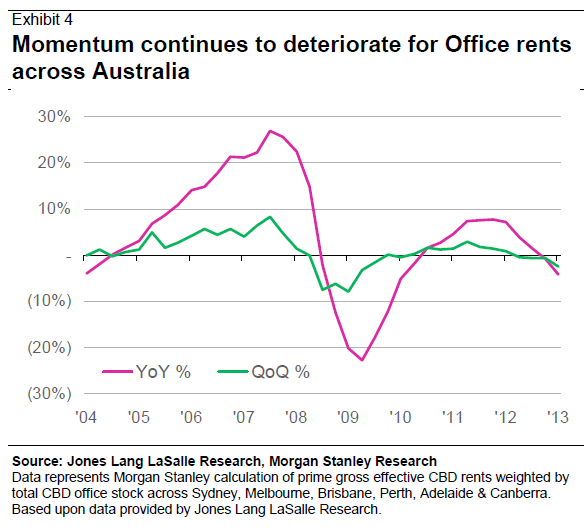

Demand fundamentals continue to deteriorate, and we see further downside risks to our office forecasts (which were last downgraded only in May). Within our report at the time (Trust Talk: Mining Capex Slowdown – The ‘Canary in the Coalmine’ for Office Demand – Download the complete report) we downgraded our rental growth forecasts for office CBDs across Australia, in particular those of the resource exposed cities of Brisbane and Perth. Examination of recent data-points from Jones Lang LaSalle Research and anecdotal feedback from industry contacts suggests conditions continue to worsen in office markets, which we believe will put further pressure on rents.

We originally highlighted that pricing power would favour tenants in 2013 in our report from early 2012. Whilst we maintained a relative preference for office through much of 2012, we highlighted within our January 2012 report (Asia Insight: Office Still Preferred Play, Despite Lower Rental Growth Outlook – Download the complete report) that the demand outlook was deteriorating and we had believed vacancy would surprise to the upside. Since that time, we have already downgraded our below consensus rental growth forecasts twice, and still see downside risks for major markets such as Sydney and Melbourne.

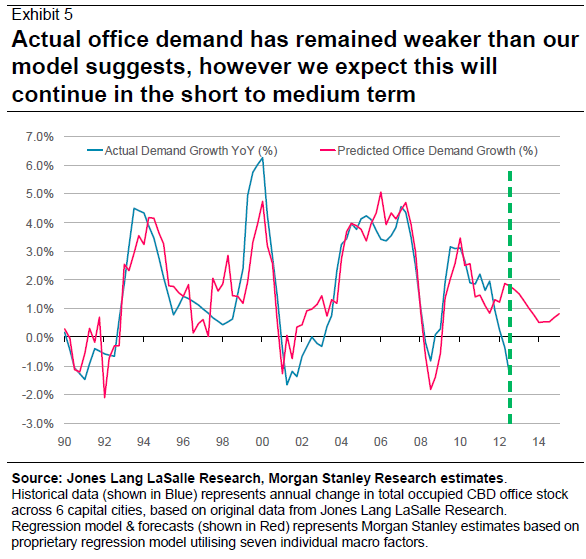

Office demand has recently diverged from our refreshed proprietary office demand model, however we see limited macro indicators that would make us positive that a rebound is on the way. This week we have refreshed and rebuilt our proprietary regression model for CBD office demand (Exhibit 5), and the first thing noticed is that actual office demand has diverged meaningfully (to the downside) vs. our model over the past 6 months. Whilst the model itself may suggest that demand should rebound in the short to medium term back in line with our model, an examination of other macro indicators in the broader market suggest momentum is likely to remain very weak in the office sector, hence we wouldn’t be surprised to see actual demand continue to remain weaker than our model suggests.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.