Friday’s solid US jobs numbers have not altered my skepticism that a US QE taper is imminent. Here is a useful cross-post from Calculated Risk on why:

At the June FOMC press conference, Fed Chairman Ben Bernanke said:

“If the incoming data are broadly consistent with this forecast, the Committee currently anticipates that it would be appropriate to moderate the monthly pace of purchases later this year. And if the subsequent data remain broadly aligned with our current expectations for the economy, we would continue to reduce the pace of purchases in measured steps through the first half of next year, ending purchases around midyear. In this scenario, when asset purchases ultimately come to an end, the unemployment rate would likely be in the vicinity of 7%, with solid economic growth supporting further job gains, a substantial improvement from the 8.1% unemployment rate that prevailed when the committee announced this program.”

The first graph is for GDP.The current forecast is for GDP to increase between 2.3% and 2.6% from Q4 2012 to Q4 2013.The first quarter was below the FOMC projections (red), and it appears the second quarter will also be below the FOMC forecast – if so, then GDP will have to pickup in the 2nd half of 2013 for the Fed to start tapering QE3 purchases in December.

The second graph is for the unemployment rate.The current forecast is for the unemployment rate to decline to 7.2% to 7.3% in Q4 2013.We now have data through Q2, and so far the unemployment rate is tracking at the high end of the forecast. If the participation rate ends the year at 63.6% (level for the year), then job growth will have to pickup up a little in the 2nd half to meet the FOMC projections. See the Atlanta Fed’s Jobs Calculator tool to estimate how many jobs per month will be needed to reach a certain unemployment level.

The third graph is for PCE prices.The current forecast is for prices to increase 0.8% to 1.2% from Q4 2012 to Q4 2013.We only have data through May, but so far PCE prices are below this projection – and this projection is significantly below the FOMC target of 2%. Clearly the FOMC expects inflation to pickup, and a key is if the recent decline in inflation is “transitory”.

The fourth graph is for core PCE prices.The current forecast is for core prices to increase 1.2% to 1.3% from Q4 2012 to Q4 2013.Once again we only have data through May, but so far core PCE prices are below this projection – and, once again, this projection is significantly below the FOMC target of 2%. Clearly the FOMC expects core inflation to pickup too.It has only been just over two weeks since the FOMC press conference, and all of the data has been worse than the FOMC forecasts (GDP revised down, unemployment rate at high end, prices below forecast). It would be a stretch to say the incoming data has been “broadly inconsistent” with the June FOMC projections, but clearly the economy will have to pickup before the FOMC would meet their “broadly consistent” goal and start to taper QE3 purchases in December. (September tapering seems less likely now since the key data has been worse than forecast, but still not impossible).

Add to this the fact that the US bond market implosion continues unabated, hiking rates at an alarming rate. The US 10 year is close to a doubling of yields in under twelve months and the 30 year is approaching a rise of 50% (that’s not 50 basis points, its 50%):

Advertisement

Unsurprisingly, again last week the US refinancing and mortgage applications indexes both plunged again and appear headed straight back to pre-QE3 levels:

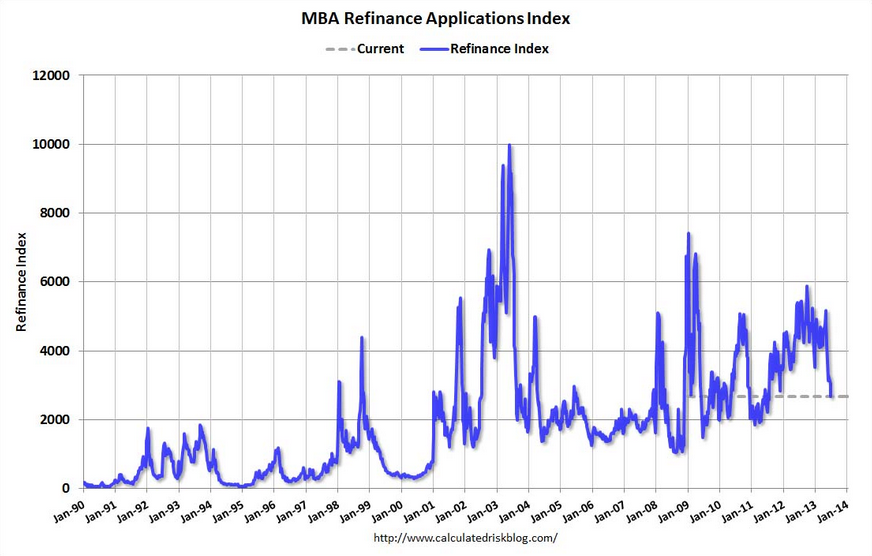

Mortgage applications decreased 11.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 28, 2013.

The Market Composite Index, a measure of mortgage loan application volume, decreased 11.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 12 percent compared with the previous week. The Refinance Index decreased 16 percent from the previous week and is at its lowest level since July 2011. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 4 percent compared with the previous week and was 12 percent higher than the same week one year ago.

Advertisement

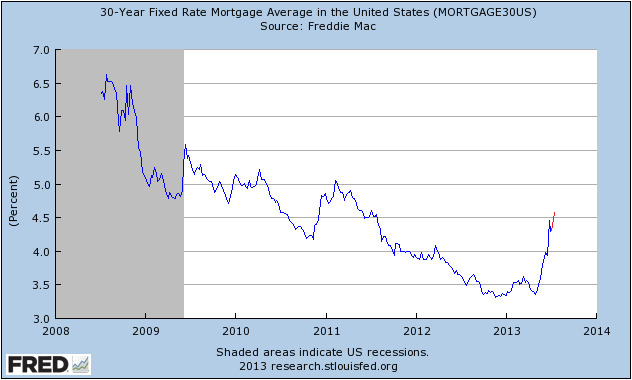

And you can expect it to continue because, as said, yields for the benchmark 30 year bond leaped after the jobs report to a new high, which will drive mortgage rates up this week above 4.5%:

It does not take Albert Einstein to conclude that this will slow the US housing market and its economic recovery.

Advertisement

Don’t get me wrong. I think the Fed is doing the right thing in using its jawbone to in some measure pop the bond bubble. It was increasingly out-of-control both in terms of the effect on house rices and the search for yield that has been blowing bubbles all over the world. But it is probable as well that the Fed is going to slow the US recovery (or prevent any acceleration), suggesting to me that markets are well ahead of the actual timing of tapering.

In the end, though, the shift in Fed rhetoric is real and unlikely to dim now. As such, it looks like the easy ride is over for the stock market and risk assets in general, even if actual tapering remains distant. In short, this is not the yield you’re looking for…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

in December.