So is the correction over? Capital Economics thinks so:

After collapsing as low as $1,180 per ounce on 28th June, the price of gold has been gradually picking up again and has already touched our revised year-end target of $1,320 set on that day. (See our Commodities Focus, “What next for gold?“, 28th June.) Indeed, gold appears to be recovering for the reasons we had anticipated – notably the prospect of a long period of ultra-low interest rates in the advanced economies, including in the US, and a rebound in demand from key emerging markets. We had been assuming that, after reaching $1,320 by end-2013, the price of gold would then climb by around 6% per year, roughly in line with the projected growth in global nominal incomes. Given that gold has hit this target sooner, we are now raising our gold price forecasts for end-2013 to $1,360, for end-2014 to $1,440 (previously $1,400) and for end-2015 to $1,530 (previously $1,480).

CE goes on to argue that gold will outperform silver:

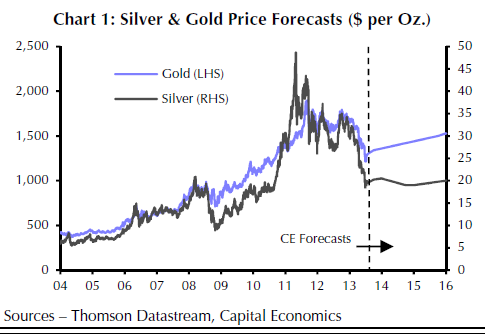

We expect silver’s underperformance to continue for three reasons. First, silver prices are more volatile (see Chart 1), in part because the market is smaller and less liquid, and partly because silver is often mined as a by- or co-product of other activities, making supply less sensitive to price movements

Second, industrial uses account for almost half of silver demand, compared to just 10% for gold. This means that silver will be more vulnerable to the weakness of the global economic recovery, particularly in China and Europe…What’s more, silver faces the headwind of an outright fall in demand from the photovoltaic sector, which had previously been growing strongly, as subsidies for solar panels are scaled back and advances in technology reduce the amount of silver used in each panel.

Third, gold is likely to benefit more from strong demand from households and central banks in key emerging markets.

Advertisement

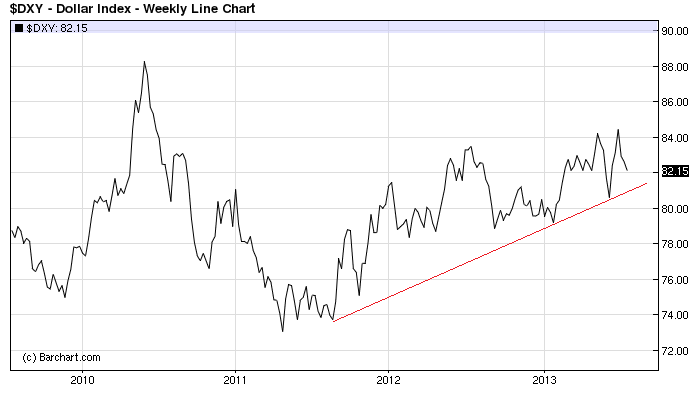

So is gold a good bet again? Virtually the only question that matters for gold is what is going to happen to the US dollar. And as DFM has been arguing, the US dollar is in an uptrend that looks suspiciously like a bull market:

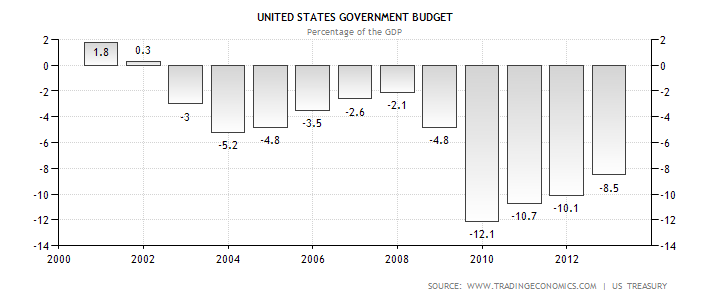

Crucially, however, this strengthening shift will rely of the stabilisation of America’s two macroeconomic levers, monetary and fiscal policy. On the latter there is steady improvement in the US deficit that is likely to continue on measured austerity and the ongoing recovery:

Advertisement

But monetary policy is the big one. If Ben Bernanke’s much discussed “tapering” of quantitative easing goes ahead then the US dollar will certainly rise further, pushing down gold. I’ve been arguing for some months that the “tapering” is doubtful. Given the bond bubble and the difficulty in deflating it slowly, the rises in long bond yields and knock-on effect on the US housing market demands tapering caution. At the same time, I think you can expect Bernanke to continue to argue its coming, to prevent irrational exuberance.

The other scenarios that would see a rise in gold are greater global instability emanating from either Europe or China but these are still tail risks.

Advertisement

There is comfort in the fact that gold has already fallen much further than the Australian currency. The local dollar is likely to outpace any further falls in the yellow metal.

However, I am still cautious. I think US housing will slow and more QE will come. The chances that the gold price has bottomed are increasing given that QE will likely be removed more slowly than markets currently expect. But with Bernanke determined to prevent an asset price blowoff, either with tapering of talk of it, this is still not an ideal environment for gold appreciation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.