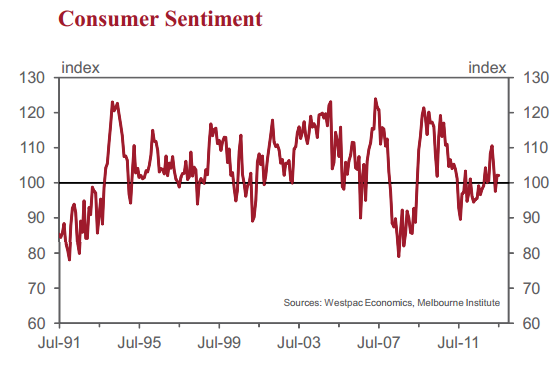

Westpac Consumer Sentiment is out this morning and is steady in July at 102.1, down just 0.1 since June:

Sentiment has held on to the gain seen last month and at just over the 100 level continues to show optimists slightly outnumbering pessimists. However, consumer confidence is still significantly weaker than at the start of the year with the Index 7.6% below its March peak.

The survey detail points to powerful ‘cross-currents’ underlying the stable headline result. Amongst the components of the Consumer Sentiment Index, those tracking views on family finances fell sharply. In particular, the sub-index tracking assessments of ‘family finances vs a year ago’ fell 5.6% to be back near recent lows. In contrast, views on the outlook for the economy improved with the sub-index tracking consumers’ expectations for economic conditions over the next five years surging 9.2% to be well above the average level recorded over the last two years.

Pinpointing the exact drivers of these shifts is difficult. The improved view on economic prospects for example may reflect shifting expectations for the US economy that have become more visible with US Fed now contemplating ‘tapering’ its QE policy stimulus. It may also reflect clearer signs of an upturn in parts of the local economy, the housing sector in particular. The sharp fall in the Australian dollar may also have played a part. The currency has gone from 104¢ US to 91.3¢ US over the last three months and although this would ordinarily be a negative for sentiment, the decline may be viewed differently given the currency’s high starting point and the difficulties this has presented for ‘tradeexposed’ parts of the economy. Other factors that may have influenced sentiment more generally in July include: the RBA’s decision to leave rates on hold at its latest meeting; mixed economic data (lacklustre retail sales but more signs of a housing pick-up); another volatile month for the sharemarket albeit with the ASX up 2% vs the previous survey; and a further rise in petrol prices (average pump price up 7¢ a litre and up 14¢ over the last two months). Political developments may well have been a factor as well with Kevin Rudd replacing Julia Gillard as Prime Minister in dramatic fashion in the week prior to the survey.

The downgrade in consumers’ assessments of their finances highlights the fragility of sentiment. It is also somewhat concerning given that these components tend to be better predictors of shifts in actual spending. Of similar concern is a downgrade in views on ‘time to buy’. The sub-index tracking views on “whether now is a good time to buy a major household item” was down only slightly in July (–1.7%) but separate indexes tracking views on ‘time to buy a dwelling’ and ‘time to buy a car’ both recorded sharp falls (–8.4% and –10.3% respectively). All ‘time to buy’ indexes are still at high levels overall but the declines again highlight the air of fragility around consumer sentiment.

The Reserve Bank Board next meets on August 6. For several months now the Bank has indicated a clear easing bias with the Governor’s statement accompanying policy decisions noting that ‘the inflation outlook, as currently assessed, may provide some scope for further easing, should that be required to support demand’. Our view is that there is a clear case for further support to demand highlighted by the lacklustre consumer response to

lower interest rates (sentiment subdued, spending and credit demand weak) and a further weakening in business conditions across both mining and non-mining sectors. Moreover we expect the Q2 CPI report due out on July 24 to show a benign read on inflation, underscoring the RBA’s ‘scope to ease’. Accordingly we expect the Bank to cut rates by 25bps at its August meeting with two further 25bp reductions coming in the December and March quarters.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.