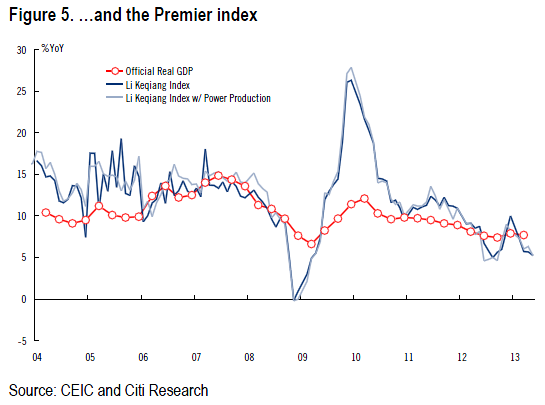

Citibank is the latest major investment firm to downgrade Chinese growth:

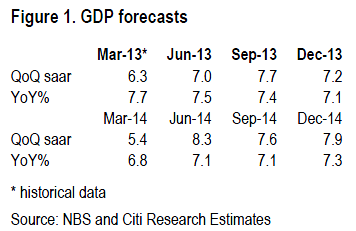

We downgrade 2013 and 2014 growth forecasts to 7.4% and 7.1% – The growth rebound in late 2012 proved short-lived, with cyclical upturn restrained by structural gravity. High-frequency data indicate growth likely decelerated to 7.5%YoY in 2Q/13 from 7.7% in 1Q. The chance of a government stimulus is remote. Credit growth slowed in May, and the recent liquidity crunch in the interbank market suggests monetary and credit conditions would become less accommodative in 2H. In addition, government emphasis on reforms may bring short-term pain before reaping long-term gain. Growth in 3Q may stay at around 7.4%YoY, benefiting from the lagged effect of relatively loose monetary policy early this year and a low base last year. Tighter credit going forward may significantly affect investment (especially infrastructure investment), bringing growth down to 7.1%YoY in 4Q and 6.8% in 1Q/14, by our estimates.

Credit conditions may become less accommodative in 2H – Benign inflation amid renewed slowdown would preclude a drastic monetary tightening. However, the willingness of PBOC to allow a liquidity crunch in Jun suggests the authorities are increasingly concerned about accumulating financial risks with credit growing at a rapid pace but the efficiency of credit in supporting growth is declining. We now see limited room for further RMB appreciation and expect USDCNY spot to be around 6.10 at end- 2013, with sporadic depreciation likely in time of capital outflows. M2 growth may fall toward 14%, and the chance of an RRR cut would increase if capital account outflows exceed current account surplus. PBOC may cut benchmark the interest rate by 25bps, increase the upward floating range for deposit rates from 10% to 20%, and eliminate the floor for lending rates. The combination of measures would have a limited impact on the overall interest rate level. We continue to expect new RMB lending to reach around Rmb9tn this year, but the recent liquidity crunch may contain off-balance-sheet credit by smaller banks, and we cut our annual forecast for total social financing to Rmb18tn. A slower credit expansion would hit infrastructure investment particularly hard, underpinning the growth downtrend into 2014.

What may trigger stimulus in 2H – Stable employment is the bottom-line for the government. While there is no reliable jobless data, PMI employment index provides an early warning. We believe the chance of stimulus would increase substantially if the index falls to 2 standard deviations below the mean. Based on our discussion with government think tanks, quarterly growth of below 7%YoY is still not acceptable. A stimulus, if any, may still rely on credit-fueled investment, and the dosage will likely be limited to stabilizing growth at just above 7%. Rate cut, RRR cut and temporary depreciation are possible responses. Investment in this case will likely be related to urbanization (such as subways, water treatment, social housing) and areas that may foster consumption over time (such as medical facilities, tourism, culture and entertainment industries).

That’s a nasty looking Q1-14, followed by more stimulus!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.