Citibank produces a quarterly construction sector report that makes interesting reading. The March QTR is out

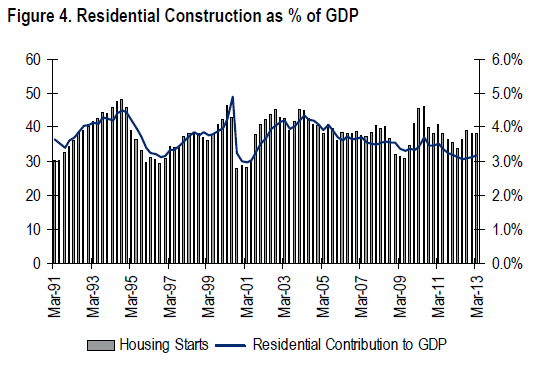

Residential Construction Remains Sideways: Cautious consumer sentiment has been restricting expenditure in the residential construction sector. The supply side is constrained due to tougher lending credit conditions which are limiting new home building and larger renovation jobs. While lower interest rates are supportive of residential construction activity, further government support (eg. reducing taxes/regulatory costs) could help. Residential construction as % of GDP grew from 3.1% in Mar-12 to 3.2% in the Mar-13 qtr due to positive growth in new dwelling construction. This outcome is fairly supported by rate cuts in late 2011 and mid 2012 along with two rate cuts in the Dec-12 qtr. However, activity in Alterations & Addition segment remains static largely due to the overhang of weak consumer sentiment.

New Home Sales Still Upbeat: 2012 was a year of lower borrowing rates combined with changes to FHB assistance, which led to slight improvement in new home sales. And importantly, recovery has continued into 2013 with new home sales up +5% y/y in Apr-13 to its highest level in last 12 months. This growth is all the more encouraging because it is driven by improvement in detached housing segment which has emerged from its recent lows and is treading upwards. An improvement in the new house segment remains critical for any sustainable improvement in new home sales and there is still a long way before new home building recovers fully.

Building Approvals Remain Positive: Building approvals were up +9% y/y to 38.9k during Mar-13 qtr with stronger momentum carried into Apr-13 (up +27% y/y). With building approvals largely in line with its long term average, we are comfortable with the rate of recovery in dwellings. But for sustainable recovery, we expect more traction from houses. The detached housing segment continued to underperform in 2012 and it remains an impediment for any possible recovery in new home building.

That’s right. Note in the chart that the contribution from residential construction is stalled. It will grow but not fast enough.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.