For all you MSM optimists out there, I suggest a strong dose of David Bassanese at the AFR today. After a flirtation with bullish housing forecasts earlier this year, Bassanese is now leading the MSM interest rate debate by following MB. He notes today the key change in this week’s RBA minutes:

…In the July minutes, for example, the board noted that while “mining investment was likely to remain high for some quarters given the considerable volume of firmly committed work. . . at some time beyond that, however, [it] was expected to decline more rapidly, partly reflecting a significant decline in the planning and development work that is a precondition for new projects”.

One month earlier, the RBA’s minutes had merely indicated “mining investment. . .was expected to remain at a high level for the next year or so, although the exact profile was difficult to predict”.

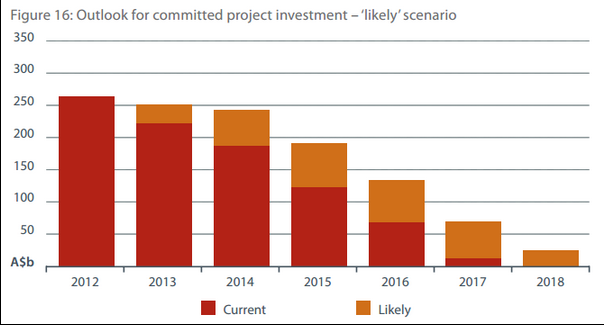

To my mind, this is a key evolution in RBA thinking, which has been largely missed across the market…Beyond 2013-14, we need to look to industry guidance and other official data. One hard number is provided by the Bureau of Resources and Energy Economics, which estimates that the value of committed mining projects will fall from around 16.5 per cent of GDP this calendar year to 4 per cent of GDP by 2017 – or the level last evident in back in 2007. Based on broad historic relationships, that suggests a decline in mining investment to around 3 per cent of GDP over the next four years, or around 1 percentage point decline per year.

Actually, Bassanese has this wrong. He is referring to BREE’s “likely scenario” not “committed projects” scenario:

The committed projects scenario is much worse and that’s the one I think we’ll end up closer to. Would it really surprise anyone if the greatest mining capacity building event in history was followed by a bit of a drought in investment? LNG and coal will rationalise not expand. Iron ore is propped up short term by the game theory being played out between big and small producers. Perhaps Gina Rinehart’s Roy Hill is still possible, though it will cause carnage if it goes ahead, and in the medium term it points the way to but one outcome: falling price and investment.

Bassanese makes more sense when he turns to rebalancing:

That said, the pre-GFC consumer leveraging boom is over and post-GFC spending caution remains. This caution was handy to have when mining was booming, but it’s leaving a major headwind as the mining boom starts to deflate. Given the political restraints on fiscal policy, that will place more of the adjustment burden on interest rates and the dollar.

Correct. Both will fall much further.