Citi has an interesting note out today offering another take on the Australian rebalancing from mining investment to other growth drivers.

The RBA has now provided their view. With signs that the rebalancing of growth is beginning to now occur, domestic investors and commentators are beginning to examine this subject. On Wednesday the RBA Governor provided his view on the topic in a speech titled Economic Conditions and Prospects in Brisbane. Compared to some of the far flung rhetoric on the subject, Governor Stevens provided a more balanced assessment of the current economic landscape and potential outlook.

Highlights of the speech included:

In hindsight, growth rates recorded pre GFC were to some extent driven by forces that were not sustainable. This may be a preconditioning factor in determining our own growth aspirations.

The starting point going into the downward phase of the investment boom is in several respects better than has existed at this point in previous episodes of this kind.

If the Australian economy needs a lower currency, our market based currency mechanism will likely deliver it.

Most of the time there is a question of “where will the growth come from”, the answer lies only in part from traditional areas. A fair amount of growth comes from new things, often things there is only a small awareness of at the time.

Non-mining investment and residential investment have strong fundamentals favouring their pick-up. Expansion should follow a pick-up in confidence in these areas. Confidence right now is somewhat subdued though.

Previous growth handovers have been largely successful. While there is no

guarantee that the next one will be, we shouldn’t assume that it won’t occur.

The RBA cannot fine-tune the growth handover or simply and easily improve confidence. Both monetary and fiscal policy need to be well established, understood and consistently applied. For its part, the RBA will continue to assist with the transition in sources of demand, consistent with its mandate.

Blame the terms of trade boom, not the exchange rate regime for the performance of various sectors over the past few years. In addition, Governor

Stevens provided some lucid arguments defending Australia’s flexible exchange rate in helping to avoid the terms of trade boom from overheating the economy and noting the previously unmentioned point that many sectors of the economy would probably still have struggled even if the exchange rate had not risen. To quote the Governor, “At a 70c dollar, the resources companies would have had even higher expected profits and an even greater ability to bid for labour and capital. Inflation of wages and prices would have been higher, and in the scramble to keep up many of the same companies that have struggled in recent times would still have struggled…Moreover, taking the inflationary route would have left a much bigger legacy of problems to come home to roost as the resources boom matured”.

A double sided wall of worry. The Governor also made the salient point that on the way up there were people that worried there would be no positive spillovers from the boom or that there would be adverse effects in net terms. Now people are worried that there were positive spillovers after all and that their reversal will be disastrous. In our view, as the earlier concerns were arguably magnified to a degree that the positive spillovers were not, it makes sense to treat the current concerns as a tail risk and not a central case.

To be clear, Citi’s view is that the rebalancing of the economy will not be costless. The process of adjustment between growth drivers in a dynamic economy will involve some frictions that will involve winners and losers. We take the view that these frictions will take the 2013 year average GDP growth rate below trend to 2.6% before a pick-up in 2014 to 3.1%. For our complete table of forecasts please see

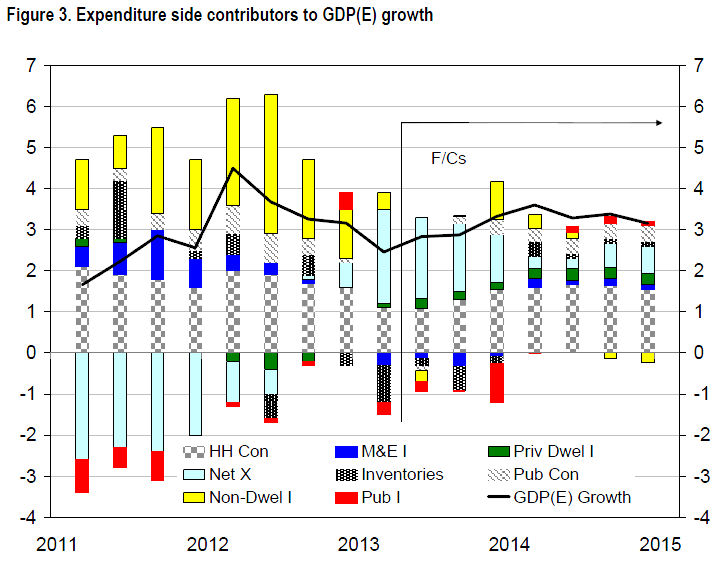

We expect growth to the end of 2014 to be moderate to good, supported by a core of private sector expenditure and net-exports. The arithmetic of our growth forecasts is shown in Figure 3, which presents the main expenditure side contributors to GDP(E), both positive and negative. This shows that the rebalancing of growth has already started. The previously large contribution from mining investment (Non-Dwel I) has abated. At the same time the large import of capital equipment that accompanied this investment has eased. In expenditure terms at least, growth in remainder of 2013 looks set to be driven more by net-exports, followed by household consumption (HH Con), with support from residential investment (Priv Dwel I) and government consumption (Pub Con). Only in 2014 does machinery and equipment investment (M&E I) and public investment (Pub I) contribute positively. These two categories we think of as essentially non-mining investment. Their return to positive growth should complete the growth jigsaw puzzle.

What about 2015 and beyond? Most of the concern about Australia’s growth outlook appears to be aimed beyond the period for which we provide detailed forecasts. But as the concerns are on the profile for mining investment, ie, worries about an investment cliff, we can add some value. Our Basic Industrials Team has updated their risk weighted engineering and construction estimates for coal, iron ore and gas projects.

Risk weighted resources investment in FY15 and FY16 will be lower, but we expect the profile to represent a manageable decline rather than an abrupt fall (Figure 4). Importantly, nominal total capital expenditure out to FY16 is expected to remain within $A10bn of the average yearly spend from FY12 to FY15. In other words, the pipeline of investment still looks solid for a number of years and provides time to increase the weight of other sectors in the economy.

Great chart! But check out the yellow bars of mining investment. It basically doesn’t fall at all. Of course we’ll be fine if no rebalancing actually needed!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.