A couple of stories today raise questions about the possible transmission of a mining bust into bad loans for banks. At the AFR, the news is good:

The head of business banking at National Australia Bank, Joseph Healy, says a slowdown in the mining sector is yet to trigger an increase in bad debts.

Mr Healy told The Australian Financial Review that economic conditions were challenging but that troubled loan levels had remained stable.

“Conditions continue to be challenging, largely because of weak business confidence and the multi-speed nature of the economy,” Mr Healy said. “As the country’s largest business bank, our business is a mirror in many ways of what is happening in the domestic economy. I feel the ongoing weak confidence and sentiment remains a challenge.”

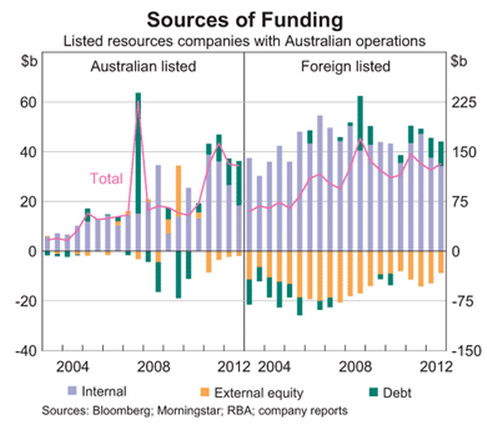

This is no surprise at all. The mining boom has been largely funded from retained earnings and cheap offshore bond debt. That’s one reason why business lending growth has been so slow yet the economy has grown OK if below trend. The following RBA chart tells the tale:

The real risk for the banks is not the mining or associated sectors but the multiplier effects of any slowing of growth that arises from a mining bust. That’s where we find State Street at The Australian:

STATE Street’s “Mr Risk” sees a clear and present danger in Australia: the housing market.

Fred Goodwin, a macro strategist at Boston-based State Street, has warned that a steep correction in house prices, while still a low probability, would hobble the ability of Australian banks to raise funds in the bond market given their heavy exposure to mortgages. Such a scenario would choke credit to the wider economy and exacerbate an economic downturn.

“The biggest worry is a significant housing crash where banks are still significantly exposed to the wholesale financing,” Goodwin said at a briefing. “That is the thing that would concern me more than anything else about Australia.”

…Goodwin says Australia may face weaker growth as China’s demand for iron ore and coal wanes.

Exactly right. The obvious trigger being rising unemployment. An additional risk will be commercial property loans, especially for development in Perth and Brisbane.

This is the major reason why I worry about an Australian economy easing towards 2% or below. Stall speed and high asset prices are a bad combination.