Westpac’s June Red Book is out and as usual makes essential reading for any consumer facing business:

The Westpac–Melbourne Institute Index of Consumer Sentiment recovered some lost ground in Jun, rising 4.7% to 102.2. That follows a sharp 11.7% drop over the previous two months. The Index is back in marginally ‘optimistic’ territory but remains 7.6% below its Mar peak.

― The component detail showed a stronger rebound in sub-indexes tracking views on ‘family finances’ with more muted rises for those tracking expectations for the economy, which have been the main driver of the fall in consumer sentiment since Mar.

― Responses to additional questions on news recall also highlight the downgraded view on the economic outlook between Mar and Jun. News items on ‘domestic economic conditions’ dominated other topics in Jun and were seen as overwhelmingly negative.

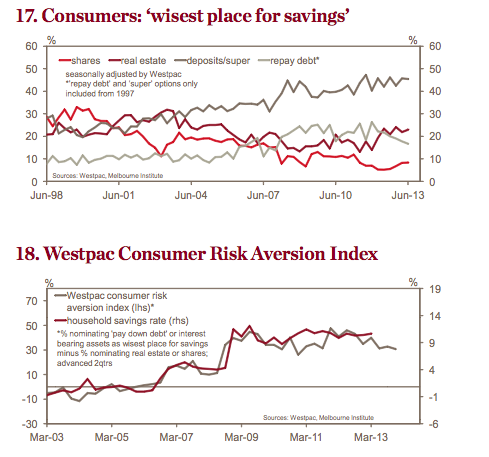

― Despite a more wary view on the economy, responses to separate questions on the ‘wisest place for savings’ suggest consumers are becoming less focused on repaying debt and more open to investing in real estate. The question, which is run every 3mths, shows interest-bearing deposits are still most favoured but a fall in the proportion nominating ‘pay down debt’ to 15.7%, the lowest reading since Dec 2007, and a rise in those nominating ‘real estate’ to 24.6%.

― The Westpac Consumer Risk Aversion Index, which draws on responses to the ‘wisest place for savings’ question to give a measure of risk aversion, declined 2pts between Mar and Jun and is now down nearly 10pts form last year’s peak. It suggests consumers may lower their savings rate over the second half of the year,

― Our CSI± measure, which includes the Westpac Risk Aversion Index and excludes ‘economic’ components of consumer sentiment, rose 4.6% in Jun and has been more stable than headline sentiment in 2013. That said, CSI± has been consistently tracking weaker levels over the last 2yrs and continues to point to weak spending growth of around 2¼%yr.

― Consumer views on ‘time to buy’ questions remain the strongest aspect of the survey. The ‘time to buy a major item’ sub-index rose 3.7% and is comfortably above its long run average. The ‘time to buy a dwelling’ and ‘time to buy a car’ indexes recorded minor changes but both remain at very strong levels (20pts and 16pts above their respective long run averages).

― The Jun survey included an additional question on consumers’ mortgage interest rate expectations. Responses show a slightly less hawkish tilt than in Feb but with no strong consensus on which way interest rates will head next. Indeed the main implication is that most consumers expect mortgage rates to stay below average for an extended period. That may in turn have encouraged some easing in the focus on paying down debt.

― Running counter to the improvement in overall sentiment and likely reflecting rising concerns about the economy, the Westpac Melbourne Institute Unemployment Expectations Index showed a further significant deterioration in Jun. The Index rose 6.3% to 158.5, above the high levels recorded in 2012 and indicating widespread expectations of rising unemployment over the next 12mths. Indeed, expectations have only been this pessimistic during recessions or downturns that have resulted in substantial rises in unemployment.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.