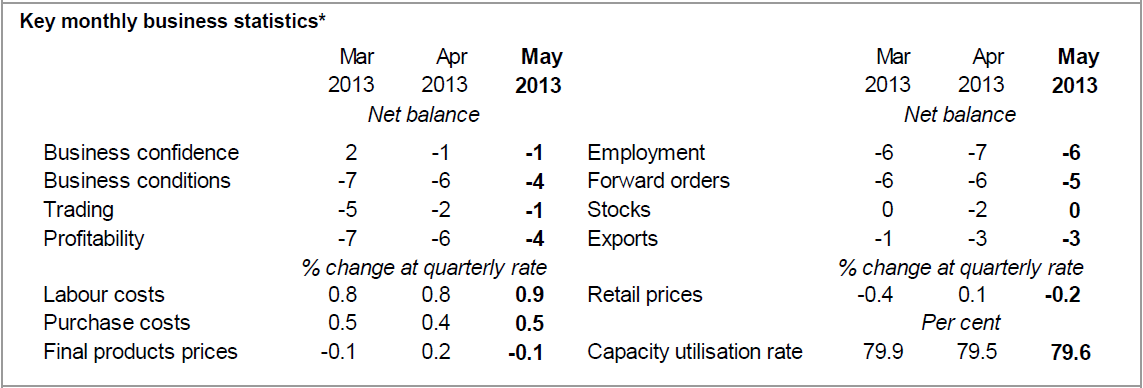

The May NAB Survey is out and shows a small improvement across its metrics:

Business conditions remain at low levels (marginally higher) with unchanged mediocre confidence levels. Conditions better in wholesale, manufacturing and construction, but mining worsens (capex at record low). Near-term demand to stay weak with forward orders, capacity utilisation and employment conditions still well below average levels. Any confidence gained from falling dollar and May rate cut have been undermined by domestic weakness. NAB activity forecasts broadly unchanged – a touch lower in out years. Currency forecasts somewhat lower.

While the business environment improved a little in May, overall business conditions remained weak with the still negative reading implying further sluggish monthly activity. Broad-based improvements in profitability, employment and trading conditions helped to lift business conditions in the month, though each of these indicators remained well below their long-run averages. Despite improvements in conditions of some weaker industries (wholesale, manufacturing and construction), mining slumped heavily in May in line with the general softness in commodity prices and the weakness in mining capital expenditure, which reached a new low in the May survey. Forward indicators suggest near-term demand will stay weak.

Business confidence remained poor in May, with mining still very pessimistic. A lower dollar and the RBA’s decision to cut the cash rate in May might have helped confidence in the month, but the weakness in the domestic economy appears to have provided some offset to this.

Overall, the survey implies underlying demand growth and GDP (6-monthly annualised) of around 2½% in the June quarter. Our wholesale leading indicator suggests a modest improvement in near-term activity, at best.

Labour costs growth edged higher in May, consistent with a slight up-tick in employment conditions. Prices (including retail) fell marginally, while modest growth in costs implies further compression of margins.

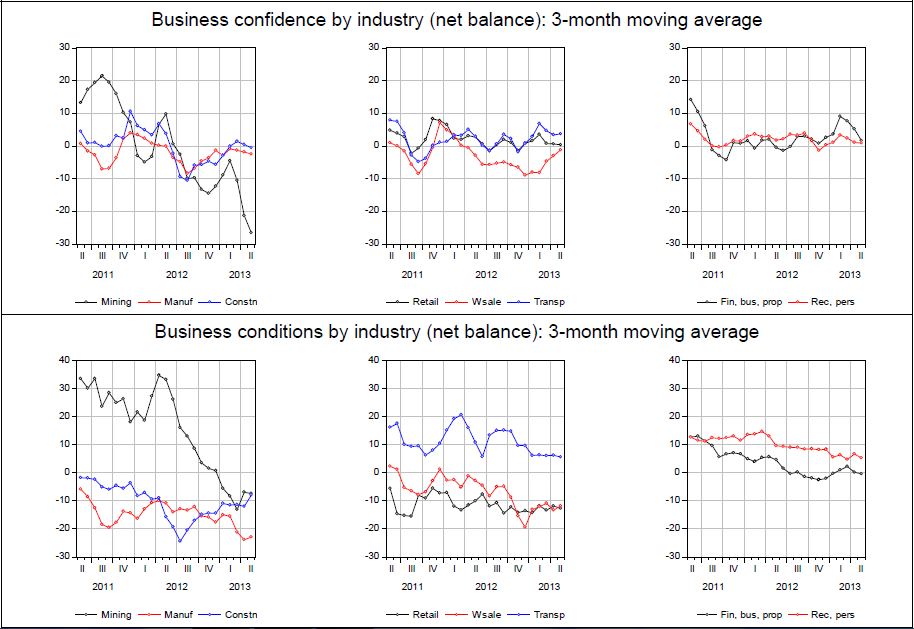

NAB has summed it upright. There is marginal improvement here, at best. That is apparent in the three month moving averages for confidence and conditions across industry:

Advertisement

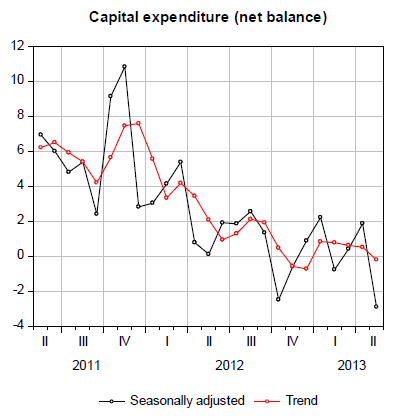

Meanwhile, capex tanked with little sign of rebalancing:

The capex index fell by a solid 5 points in May, to -3 index points. The deterioration was largely driven by an extremely large decline in mining (down 37 points to -44 points), where capex fell to its lowest level in history, as well as construction (down 13) and manufacturing (down 12). The only industries to report an improvement in capital expenditure were retail and wholesale (up 4 and 2 points respectively). In levels terms, capex was by far the lowest in mining (-44), followed by manufacturing (-14) and construction (-10), while it was highest in recreation & personal services, retail (both +5) and transport & utilities (+3).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.