I don’t trust last night’s rally in US stock markets.

Sure everyone in equity land was happy that Shanghai scrapped its way back from nearly 6% down to close to square on the back of PBOC hopes but if markets last week sold off on the basis that the taper is coming and that central banks want to take air out of the bubble then there is more downside to come.

Just look at the data. It fairly screamed taper and the stock market reaction fairly screamed “cognitive dissonance”.

On the face of it none of the data were spectacularly important but taken together they give a good feel for what is happening in the economy right now. Durable Goods jumped 3.6% against 3% expected. Richmond fed Manufacturing followed its recent Dallas counterpart by jumping sharply to +8 from -2 last month. Case Shiller said house prices are up 12.1% year on year against expectations of 10.6% while New Home Sales were 2.1% and Consumer Confidence jumped from 75.1 in May to 81.4. this month,which is the best print since January 2008 before this whole mess really kicked off.

So you can see in this that Bernanke and the team will be smiling to themselves that they are doing the right thing and the market rally last night might prove ephemeral in the days and weeks ahead as thoughts and talk of the taper grows. And for goodness sake there are 5, yes 5, Fed Governors talking in public in some way, shape or form tonight.

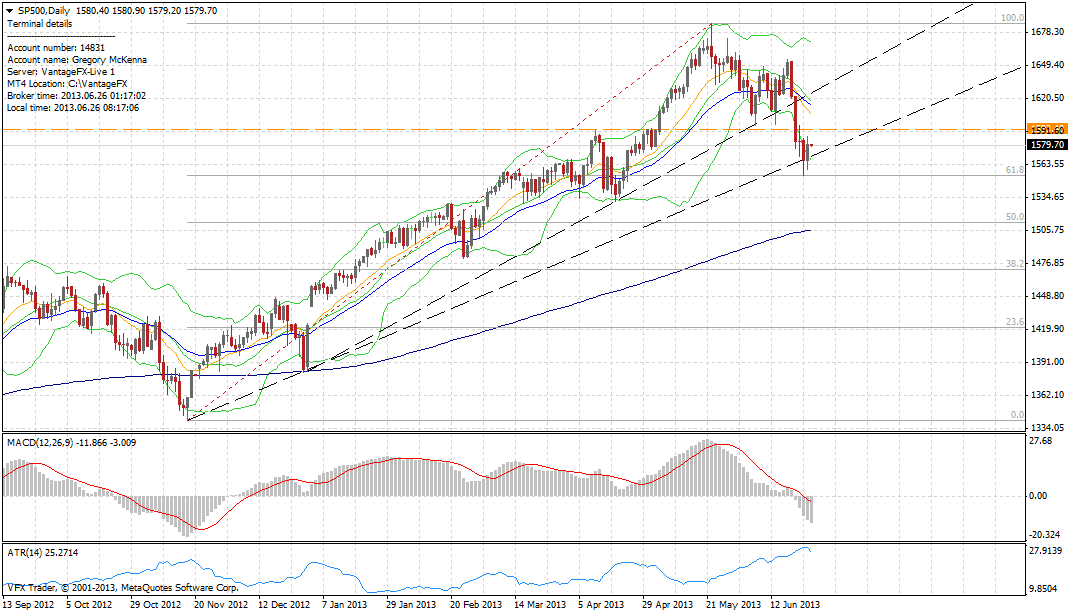

In the end though the Dow was up 100 points to 14760, the Nasdaq rose 0.82% to 3348 and the S&P 500 rose to 1588 up 0.95%. In Europe stocks were also higher with the FTSE up 1.21%, the DAX up 1.54%, the CAC up 1.51%, stocks in Madrid up 0.73% while in Milan the bourse was 0.37% lower.

So while US equities goosed themselves higher, 10 year Treasuries rose again to 2.61% this time and it is increasingly looking like these are going to need to travel to somewhere closer to 3% before any meaningful support can be found.

So I don’t trust last night’s rally and although I’m not silly enough to say the market is wrong and I am right, my JimmyR indicator says it is now a bear market so this looks to me to be a reaction off a very important long term Fibonacci level and that’s about all.

In FX land it was a bit weird with the euro, yen and pound under a bit of USD pressure but it wasn’t exactly super strong and the Aussie had another wild ride.

The euro looks really weak to me and I continue to see it trading substantially lower in the days and weeks ahead. Over the past 24 hours the range has been 1.3150 down to 1.3063 and it sits at 1.3092 at the moment. Euro lost ground across the board slightly as well due to this weakness in the euro outright. It is sitting just on the 200 day moving average at the moment and a break, and hold, will likely turn the trend back to negative.

USDJPY was a little higher trading up to 98.05 and GBP sits at 1.5425. The data in the US last night combined with 5 Fed speakers, in some form or the other tonight, should aid the US dollar across the board in the next 24 hours if the Bernanke, Kocherlakota, Fisher lead in over the past few days is any guide.

The Aussie has looked both very weak and very strong in equal measure at times over the past 24 hours. Opening around the 0.9250 region Aussie traded down to 0.9195 and all the way back to 0.9296 and sits up just 0.10% at 0.9256. At least Nicholas Darvas would be pleased because we know we are in a 0.9190-0.9300 box for the moment with an extension up 0.9325 and down to the low the other day of 0.9145. A break will likely kick one way or the other.

Clearly after all the downside recently and given the set up a break to the topside is likely more decisive.

Now one thing I should do, because I have begun a conversation about my trading in this space is highlight the lessons learned yesterday – or should I say relearned. So memo to self – DO NOT TRADE WHEN YOU ARE SICK. I have spent a lot of time over the past couple of weeks collecting pips and building up a substantial return amongst all of the volatility. But in one fell swoop yesterday I managed to screw it up because I wasn’t paying attention and didn’t stick to my process – largely because I’m crook and should have turned the machine off.

So it wasn’t a banner day, the volatility that I love bit me on the backside and I got to relearn two lessons, don’t trade unless you are fit to trade and don’t deviate from your process. Stuff happens and we move on but gee whiz!

Crude was largely unchanged up 0.15%, with gold and silver a similar amount either side of square for the past 24 hours.

Data

Gfk Consumer Confidence in Germany, GDP in France, UK Financial Stability report but we know the banks need to be recapitalised from this week so should have limited impact I guess and then the third read I think of US GDP.

AND 5, yes 5, Fed officials speaking in various contexts.

Twitter: Greg McKenna