By Greg McKenna

Markets are at an incredibly critical juncture at the moment with the notions that a Fed taper is coming as soon as next week top of my mind with the resultant impact on stocks front and centre too. I‘ll talk about that a little later but first lets focus on the massive 4.9% rally in the Nikkei yesterday after the yen weakened again and as we await the BoJ’s announcement later today.

On the face of it the BoJ should just sit back, relax and enjoy the ride on the wave that the economy has picked up after the yen’s 25% slide against the dollar, won and yuan which was in evidence with yesterdays Q1 2013 GDP. I would struggle to see how the BoJ might be more accommodative given they seem to be gaining traction with a 1% growth rate QoQ and 4.1% annualized both better than expected. But something to note is that the GDP deflator fell 1.1% much worse than the -0.8% expected. So Japan and the BoJ still has a deflation problem not the 2% inflation they are aiming at.

So I guess the BoJ might pull a rabbit out of the hat today. Hold onto your hats traders it could be more volatility.

Which brings me to the other source of volatility recently – the Fed and its taper. Non-farm payrolls on Friday night of 175,000 was a pretty goldilocksy number when you add in the rise to 7.6% for unemployment but “Fed Mouthpiece” Jon Hilsenrath seems to me to have doubled down on his warning that the Fed IS going to signal a taper and soon and that the word “taper” understates exactly what the Fed is going to do.

In the Wall Street Journal after the jobs data last night Hilsenrtath said:

A good-but-not-great jobs report Friday ensured officials wouldn’t want to act right away and would instead want to see more data before taking a delicate step toward winding down the program. But they could point at their next meeting to improvement they’re seeing in the economy, a prerequisite to reducing the so-called quantitative-easing program.

And then followed up in a separate article with:

The hangup for Fed officials is the word “tapering” suggests a slow, steady and predictable reduction from the current level of $85 billion a month at a succession of Fed meetings, say to $65 billion per month, then to $45 billion and so on. And that’s not necessarily what Fed officials envision.

Ouch – watch out we may be in for a bit of a shock as soon as the next week’s FOMC meeting.

Certainly the message might have got through to US bond traders as both the 30 year and 10 year were higher with the former at its highest since April 2012 and the 10 year closing at 2.21%.

This and the Fed is becoming a threat to the stock market rally.

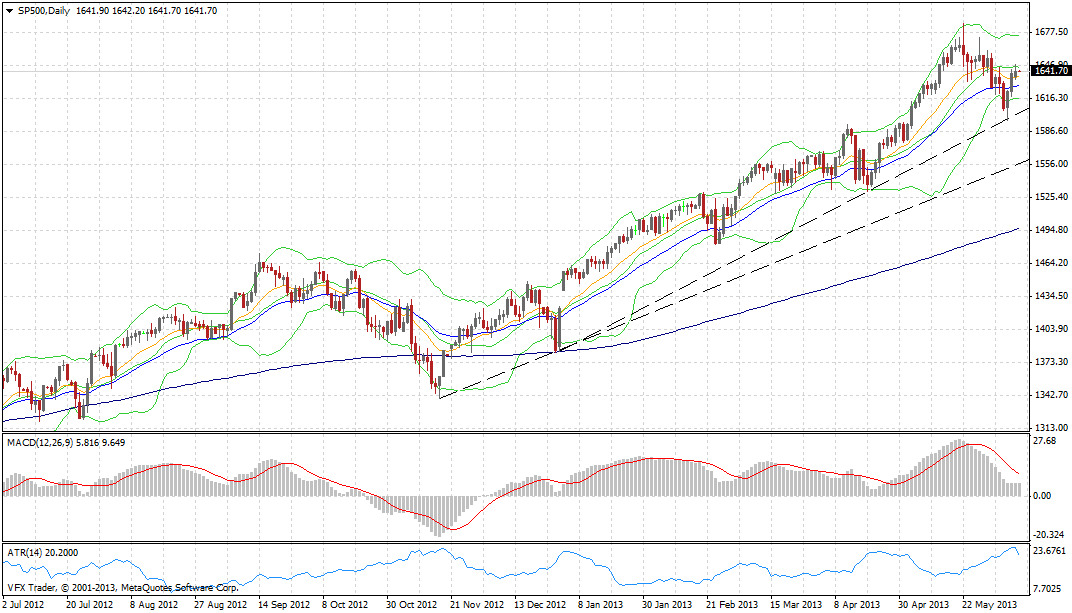

Last week the S&P 500 bounced perfectly off the big uptrend line. It remains the level to watch and while this means the up trend is still intact I am wary. Puts in the back pocket and all that :).

At the close then US stocks ignored the big 4.94% bounce in the Nikkei yesterday in Asia closing either side of flat. The Dow was down 0.06%, the S&P 500 down 0.02% and the Nasdaq up 0.14%.

In Europe Germany continues to be a law unto itself with the DAX rising 0.65% but the rest of the market was under pressure. The FTSE was down 0.19%, the CAC down 0.22%, Milan fell 0.81% and Spanish stocks fell 0.48%. But the real action was in Greece with the Athenian stock market fell 5.8% after the news that one of the cornerstone revenue raises for the Greek Rescue package, the sale of DEPA the Greek natural gas firm – failed to attract a bid. This makes it harder for Greece to hit its targets agreed with the Troika but it is worth noting that globally almost everyone except the Germans are acting more conciliatory for countries in strife at the moment.

Looking to the FX markets and the yen and the Aussie are the big ones I’m looking at presently and by definition the AUDJPY cross as this could be a lot of fun over the next few days.

The Australian dollar is struggling hard and I’m not sure whether the signals suggest that I should be very bullish or very bearish. Yesterday it got knocked under 94 cents on the back of the weaker than expected Chinese trade data that looked to me like authorities had cracked down on the “invoicing” racket with Hong Kong which is really just a way to get money off the mainland. But the Aussie did find support and rallied with the EUR and GBP overnight to a high of 0.9480 off a 0.9390 low.

The bullish signal is the fact that the CFTC COT report released Saturday morning showed a net short position in the Aussie dollar of m0re than 58,000 which looks like an all-time net high for shorts. The bearish signal is that the Aussie continues to make 52 week lows as it did again yesterday and with Friday night’s close.

My sense is that I need to see 0.9377 trade as a clear signal that the support zone has broken otherwise I am going to treat it as intact and indeed I bought yesterday in the mid teens after the low and sold last night at 0.9477 last night just below the high of 0.9480. BoJ today is going to be important as is the home loan data and NAB Business Survey. The most important economic stat in Australia each month.

Looking at the chart above you can see the important juncture that the USDJPY is at presently. Having broken the 99.90 level and the 6 month+ uptrend USDJPY fell out of bed with a huge move last week into the 94’s before rallying hard for a retest yesterday of the up trend line. It would be my proposition that while below the 99.90/100 level USDJPY has more downside ahead of it.

The euro had a big week last week too but even with a strong rally yesterday it has to break the 1.3300/20 region to kick on. Sterling looks exactly like euro over the past few days and needs to take out 1.5680/1.57 which is last week’s high and the 200 week moving average.

Commodities

It’s all a bit boring on commodity markets, or at least the ones we watch, at the moment. Nymex crude was down 0.31% to $98.73, gold rose 0.23% to $1386 and silver was 0.85% higher at $21.78. Dr Copper fell 0.83% and corn, wheat and soybeans were under intense pressure falling 2.14%, 1.04% and 0.93% respectively.

Data

Big day today with the BoJ interest rate decision and the Australian NAB business survey and home loan data.

In Europe tonight we have industrial production and the German Constitutional court ruling on the OTM bond buying program.

The US is quiet.

Twitter: Greg McKenna