Warning video starts automatically.

Overnight the governing council of the ECB met and decided to leave all rates on hold. The press conference video and transcript are below.

It was a standard performance from Draghi, talking up much of the weak data and talking through many major problems along with pushing his mandate by again commenting on fiscal policy of member nations. Of note he stated that more stimulus is available if necessary, inflation is under control, negative deposit rates were discussed but remain “on the shelf”, growth expectation are yet again down a little , and more needs to be done to fast-track the banking union.

I’m not sure if it is the fact that I have watched so many of these things now that I can almost tell what he is going to say, but I must admit in my mind this was one of the weakest performances I have seen him give. That may well be because his previous predictions of a recovery this year are slowly being pushed back by the data, or quite simply because his answers to a number of questions in the Q&A session appear completely disconnected from the reality of what is occurring around him in the real economies of Europe. You can judge for yourself.

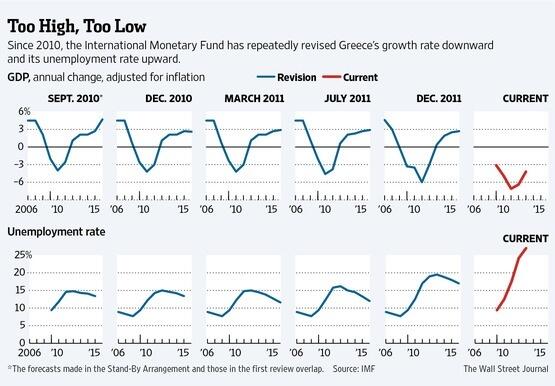

As per usual, the post-statement session was the most interesting part and quite revealing in light of the latest IMF publication documenting the Fund’s own failings on the Greek program, particularly in the area of debt sustainability and fiscal multipliers. You can see from the chart below that the Fund’s estimations were, and continue to be, woefully incorrect . If you are unaware of this particular publication then I recommend you read this assessment from Bill Mitchell which is the best analysis of the IMF report I have read over the last few days:

Mr Draghi was asked directly about the report but he basically ignored the question, although he admitted he hadn’t read the report, which is quite enlightening given his constant remarks about fiscal policy in these monetary policy addresses.

Although Mr Draghi claims to have not have read it, the European Commission most definitely has, releasing the following rebuttal overnight.

The European Commission rejected the findings of an International Monetary Fund report that said mistakes had been made in the handling of Greece’s international bailout and said it would launch its own report into the matter.

The Commission “fundamentally disagrees” with the report’s argument that it would have been better to force losses on Greece’s private creditors right from the start, said a spokesman for the Commission. “The report ignores the interconnected nature of euro area member states,” he said, arguing that, in the Commission’s view, restructuring Greece’s privately-held debt at the outset “would have risked contagion.”

“You can’t divorce the question of Greece’s remaining in the euro area and the contagion implications of a Greek exit from the euro area from Greece’s own stability and prosperity,” he said.

“A restructuring at that stage in the programme would have had devastating consequences not only for the other member states of the euro area, no small consideration, but also for Greece itself,” the Commission spokesman said.

All decisions on the handling of Greece’s debt crisis taken by Eurozone governments, the IMF and the European Central Bank, were done so unanimously at the time, the spokesman added.

The IMF report, by contrast, argued that “an upfront debt restructuring would have been better for Greece, although this was not acceptable to the euro partners.”

“A delayed debt restructuring also provided a window for private creditors to reduce exposures and shift debt into official hands,” the IMF argued.

Additionally, the Commission, also “fundamentally disagrees” that not enough was done to encourage structural reforms, he said, arguing that the Commission had always emphasised the need for structural reforms and that Brussels has played a “central role” in devising Athens’ reform agenda.

Greece, and its international aid partners, worked rapidly to devise a bailout programme in and “unprecedented emergency situation”.

The three institutions, referred to as the Troika, were in “a learning process” at the time, he stressed.

The spokesman also downplayed the significance of the IMF report, which was prepared by the Fund’s staff as an independent assessment and which is its official position. The Commission will launch its own report on the matter he said, without giving any indication of when the report would be ready.

Despite the differences highlighted by the IMF report, which also criticised the high upfront dose of austerity Greece’s lenders prescribed, the Commission and IMF had a “very good working relationship” and no change in the way they work together should be concluded, the spokesman said.

Sharon Bowles, the chair of the European Parliament’s Economic and Monetary Affairs Committee, said that it was not enough for the IMF to admit mistakes, it also has to learn from them.

“It is all well and good of the IMF to admit that mistakes have been made. But the real question is whether lessons have been learnt,” she said, pointing out that Cyprus “was not handled efficiently either”.

In the case of Cyprus, “the IMF put its own preference before the country’s economic sustainability,” she argued.

Of particular note is the line “A delayed debt restructuring also provided a window for private creditors to reduce exposures and shift debt into official hands”. Of course we all know that “offcial hands” actually means “Eurozone taxpayers” and “private creditors” means “European banks and financial institutions”. Tells you all you need to know really!

There will definitely be more to come on this episode.

Full transcript of Mario Draghi introductory speech is below.

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today’s meeting of the Governing Council, which was also attended by the President of the Eurogroup, Finance Minister Dijsselbloem.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. Incoming information has confirmed our assessment which led to the cut in interest rates in early May. The underlying price pressure in the euro area is expected to remain subdued over the medium term. In keeping with this picture, monetary and, in particular, credit dynamics remain subdued. Medium-term inflation expectations for the euro area continue to be firmly anchored in line with our aim of maintaining inflation rates below, but close to, 2%. At the same time, recent economic sentiment survey data have shown some improvement from low levels. The accommodative stance of our monetary policy, together with the significant improvements in financial markets since mid-2012, should contribute to support prospects for an economic recovery later in the year. Against this overall background, our monetary policy stance will remain accommodative for as long as necessary. In the period ahead, we will monitor very closely all incoming information on economic and monetary developments and assess any impact on the outlook for price stability.

Let me now explain our assessment in greater detail, starting with the economic analysis. Real GDP contracted by 0.2% in the first quarter of 2013, following a decline of 0.6% in the fourth quarter of 2012. Output has thus declined for six consecutive quarters, with labour market conditions remaining weak. Recent developments in economic sentiment survey data have shown some improvement from low levels. Looking ahead to later in the year and to 2014, euro area export growth should benefit from a recovery in global demand, while domestic demand should be supported by the accommodative stance of our monetary policy and by the recent real income gains due to lower oil prices and generally lower inflation. Furthermore, the significant improvements in financial markets seen since last summer should work their way through to the real economy, as should the progress made in fiscal consolidation. At the same time, the remaining necessary balance sheet adjustments in the public and private sectors will continue to weigh on economic activity. Overall, euro area economic activity should stabilise and recover in the course of the year, albeit at a subdued pace.

This assessment is also reflected in the June 2013 Eurosystem staff macroeconomic projections for the euro area, which foresee annual real GDP declining by 0.6% in 2013 and increasing by 1.1% in 2014. Compared with the March 2013 ECB staff macroeconomic projections, the projection for 2013 has been revised marginally downwards, largely reflecting the incorporation of the latest GDP data releases. For 2014 there has been a marginal upward revision.

The Governing Council continues to see downside risks surrounding the economic outlook for the euro area. They include the possibility of weaker than expected domestic and global demand and slow or insufficient implementation of structural reforms in euro area countries.

According to Eurostat’s flash estimate, euro area annual HICP inflation was 1.4% in May 2013, up from 1.2% in April. This increase was, in particular, accounted for by a rebound in services prices related to the unwinding of the Easter effect and an increase in food prices. More generally, as stated last month, annual inflation rates are expected to be subject to some volatility throughout the year due particularly to base effects relating to energy and food price developments twelve months earlier. Looking through this volatility, the underlying price pressure over the medium term is expected to remain subdued, reflecting low capacity utilisation and a modest pace of economic recovery. Over the medium term, inflation expectations remain firmly anchored in line with price stability.

This assessment is also reflected in the June 2013 Eurosystem staff macroeconomic projections for the euro area, which foresee annual HICP inflation at 1.4 % and 1.3 % in 2013 and 2014, respectively. In comparison with the March 2013 ECB staff macroeconomic projections, the projection for inflation for 2013 has been revised downwards, mainly reflecting the fall in oil prices, while the projection for 2014 remains unchanged.

In the Governing Council’s assessment, risks to the outlook for price developments are broadly balanced over the medium term, with upside risks relating to stronger than expected increases in administered prices and indirect taxes, as well as higher commodity prices, and downside risks stemming from weaker economic activity.

Turning to the monetary analysis, recent data confirm that the underlying pace of monetary and, in particular, credit expansion continues to be subdued. Annual growth in broad money, M3, increased in April to 3.2%, from 2.6% in March, mainly due to a base effect and special factors. The same factors have impacted on the annual growth rate of the narrow monetary aggregate, M1, which increased from 7.1% in March to 8.7% in April.

The growth of loans to the private sector continued to be weak. The annual growth rates of loans to households (adjusted for loan sales and securitisation) remained at 0.3% in April, broadly unchanged since the turn of the year. The annual negative growth of loans to non-financial corporations (adjusted for loan sales and securitisation) increased from -1.3% in March to -1.9% in April. This development stemmed, in particular, from net redemptions in short-term loans, which could reflect reduced demand for working capital against the background of weak order books in early spring. More generally, weak loan dynamics continue to reflect primarily the current stage of the business cycle, heightened credit risk and the ongoing adjustment of financial and non-financial sector balance sheets.

In order to ensure adequate transmission of monetary policy to the financing conditions in euro area countries, it is essential that the fragmentation of euro area credit markets continues to decline further and that the resilience of banks is strengthened where needed. Progress has been made since last summer in improving the funding situation of banks, in strengthening the domestic deposit base in stressed countries and in reducing reliance on the Eurosystem as reflected in repayments of the three-year LTROs. Further decisive steps for establishing a banking union will help to accomplish this objective. In particular, the Governing Council emphasises that the future Single Supervisory Mechanism and a Single Resolution Mechanism are crucial elements for moving towards re-integrating the banking system and therefore require swift implementation.

To sum up, the economic analysis indicates that price developments should remain in line with price stability over the medium term. A cross-check with the signals from the monetary analysis confirms this picture.

With regard to fiscal consolidation and structural reforms, the Governing Council welcomes the progress made and encourages governments to continue with determined efforts. It is essential that euro area countries do not unravel their efforts to reduce government budget deficits. The new European governance framework for fiscal and economic policies should be applied in a steadfast manner. In this respect, the Governing Council considers it very important that decisions by the European Council to extend the time frame for the correction of excessive fiscal deficits should remain reserved for exceptional circumstances. At the same time, it is necessary to continue, where needed, to take legislative action or otherwise promptly implement structural reforms. Structural reforms should, in particular, target competitiveness and adjustment capacities in labour and product markets, thereby helping to generate employment opportunities in an environment of unacceptably high unemployment levels, especially among young workers, prevailing in several countries. Combined action on the fiscal and structural front should mutually reinforce fiscal sustainability and economic growth potential and thereby foster sustainable job creation.