Late Friday, ANZ issued a warning that the Chinese financial system is exhibiting signs of considerable stress:

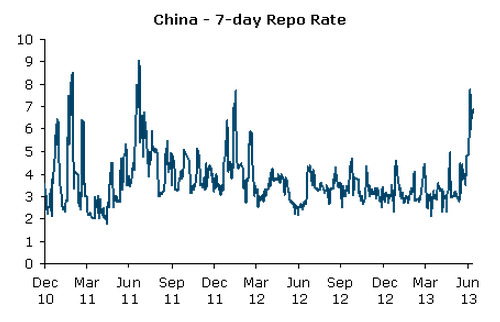

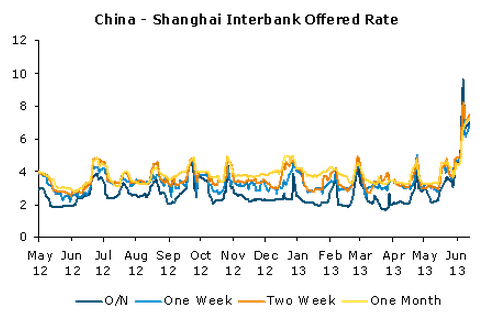

Onshore liquidity conditions have tightened in the past few weeks, despite of PBoC’s continuous liquidity injection. The 7-day repo rate, the most important indicator to reflect the market liquidity environment, picked up to around 10% before the dragon boat holidays. It has declined slightly to around 7% in the past two trading days but remains elevated compared with its average level of 3% over the past year.

SIGNALS OF HEIGHTENING FINANCIAL STRESS

Based on our previous analysis and understanding of the onshore market, we believe the jump of interest rate can be attributed to a number of possible explanations:

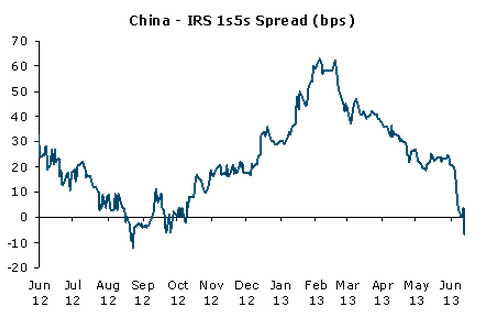

Seasonal and festival factors: For example, Chinese corporates need to submit the tax payment for last year before the end of May, and the commercial banks tend to hoard cash before the holidays. However, the market liquidity conditions didn’t ease significantly after the holidays as has normally happened. In addition, it seems that the market believes that the liquidity conditions won’t ease even after the end of Q2, as the IRS rates continue to pick up, and the Ministry of Finance failed to sell 9-month government bonds this morning. However, we do not think the seasonal and festival factors are the key drivers of the abnormal surge this year because the market should have been factored in them.

Cracking down of trade-related arbitrages: The Chinese authorities tightened regulation to limit export over-invoicing, which could have reduced capital inflows. China’s exports collapsed in May after a surge in the past two quarters, reflecting the authority’s efforts to crack down on over-invoicing and round-tripping activities that seek financial gains on large offshore and onshore interest rate differentials and RMB’s appreciation. Also commercial banks need to buy more USD positions before the end of June due to the new regulation by SAFE. (Under the new rule, banks are required to maintain a minimum net foreign exchange position based on a formula). As a result, the commercial banks need to reserve more RMB funding (to purchase USD at a proper timing) than normal, which has further tightened the market.

Extraordinary tightness of onshore liquidity this year: It has been reported that an interbank payment (of RMB6bn) between two prominent onshore banks failed to be made on time on 6 June because of tight liquidity conditions, which has increased risk aversion and hit sentiment. While both banks denied this report, including an e-mailed statement that relationships were good and that “all liquidity indicators… are good”, onshore commercial banks have remained quite cautions in the past week in order to avoid liquidity squeezing. As of today, there has not been any official explanation on the development of this apparent “default” case.

MOF fails to sell all auctioned bills: Today the Ministry of Finance failed to sell all of its 273-day bills at an auction, according to traders that participated in the sales. This is the first time the MOF has failed to sell all of its bills since July 2011. The lack of appetite for MOF bills reflects the tight liquidity conditions onshore as banks hoard cash. Reportedly, the average yield for the 273-day bills at the auction was 3.7612%, compared with yesterday’s 3.14% for bonds with similar maturity on the secondary market.

ANZ ASSESSMENT

Policymakers should not undermine financial sentiment:

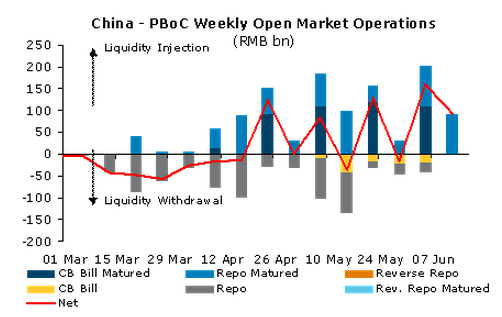

Our understanding is that the PBoC is attempting to adopt a disciplinary approach and “let the market work” without stepping in to resolve the tight liquidity condition. On 13 June, the PBoC did not conduct any open market operations. However, the net injection of RMB92bn this week has failed to ease the domestic liquidity condition. We think that the jump in interest rates is signalling a rising financial risk for

China’s financial sector. If the policymakers do not act pre-emptively and decisively, the financial risk could become a macroeconomic risk.

Interest rate cut is imminent:

As the risk of inflation diminishes near-term and activity data remain sluggish, China’s monetary policy stance should turn to be more supportive of growth. Central banks in the region have cut interest rates and used intervention to ease the pressures of currency appreciation on export competitiveness. So we believe it will be difficult for the PBoC to maintain a relatively high policy rate and continue to allow the RMB to appreciate in the short run. We believe a strong currency, together with sluggish real economic activity and limited inflationary pressures, have set the right conditions for the PBoC to cut the policy rate by 25bps. As reflected at the recent G7 meeting, an interest rate cut is regarded as a domestic policy tool as long as the country concerned is not aiming to intentionally devaluate its currency. The benefit of an interest rate cut is that it will discourage capital inflows and overheating in the property sector. Given China’s mortgage rate does not change following an interest rate cut within a calendar year, we do not think an interest rate cut will stimulate much demand for residential property.

Monetary and financial reform should be accelerated immediately:

Since the new leadership took power following the March’s NPC meeting, the monetary authority (ie the PBoC) has failed to convince the market that it is undertaking a clear strategy to push forward overall monetary and financial reform. There has been no specific action for interest rate liberalisation, exchange rate regime reform and capital account liberalisation. We think that the daily routine of open market operations cannot substitute for a faster acceleration of structural reform. Further inaction by the PBoC will lead to large risks in the financial system, fast slowdown of the economy, significant loss of Chinese competitiveness, and large unemployment pressure this year.

To cut a long story short, Chinese banks increasingly either can’t or won’t lend to one another. Western analysts have been forecasting interest rate cuts non stop for two years. It seems to me that the PBOC is determined to not do so as a part of its encouragement of structural adjustment. That is, it does not want to decrease household purchasing power and increase the ease at which bad debts around dodgy infrastructure loans can be rolled over. Having said that, the stress is looking worrying and it may have no choice.

ANZ is not alone in its concern. On Friday Fitch also issued a dire warning. From the Telegraph:

Advertisement

[Fitch] said the scale of credit was so extreme that the country would find it very hard to grow its way out of the excesses as in past episodes, implying tougher times ahead.

“The credit-driven growth model is clearly falling apart. This could feed into a massive over-capacity problem, and potentially into a Japanese-style deflation,” said Charlene Chu, the agency’s senior director in Beijing.

“There is no transparency in the shadow banking system, and systemic risk is rising. We have no idea who the borrowers are, who the lenders are, and what the quality of assets is, and this undermines signalling”…

“Typically stress starts in the periphery and moves to the core, and that is what we are already seeing with defaults in trust products,” she said.

Fitch warned that wealth products worth $2 trillion of lending are in reality a “hidden second balance sheet” for banks, allowing them to circumvent loan curbs and dodge efforts by regulators to halt the excesses.

This niche is the epicentre of risk. Half the loans must be rolled over every three months, and another 25pc in less than six months. This has echoes of Northern Rock, Lehman Brothers and others that came to grief in the West on short-term liabilities when the wholesale capital markets froze…

Overall credit has jumped from $9 trillion to $23 trillion since the Lehman crisis. “They have replicated the entire US commercial banking system in five years”…

The ratio of credit to GDP has jumped by 75 percentage points to 200pc of GDP, compared to roughly 40 points in the US over five years leading up to the subprime bubble, or in Japan before the Nikkei bubble burst in 1990. “This is beyond anything we have ever seen before in a large economy. We don’t know how this will play out. The next six months will be crucial”…

“There is no way they can grow out of their asset problems as they did in the past. We think this will be very different from the banking crisis in the late 1990s. With credit at 200pc of GDP, the numerator is growing twice as fast as the denominator. You can’t grow out of that.”

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.