China bull, Stephen Green of Standard Chartered, has spooked the market this morning with a downgrade to Chinese growth to 7.7% for 2013 (from 8.3%), and to 7.5% for 2014 (from 8.2%). According to Green:

The acceleration of China‟s 2013 economic growth is taking a little longer than we expected. A disappointing March was followed by a moderately weak April; there are few signs of renewed dynamism. As a result, we are adjusting our 2013-14 China forecasts as follows:

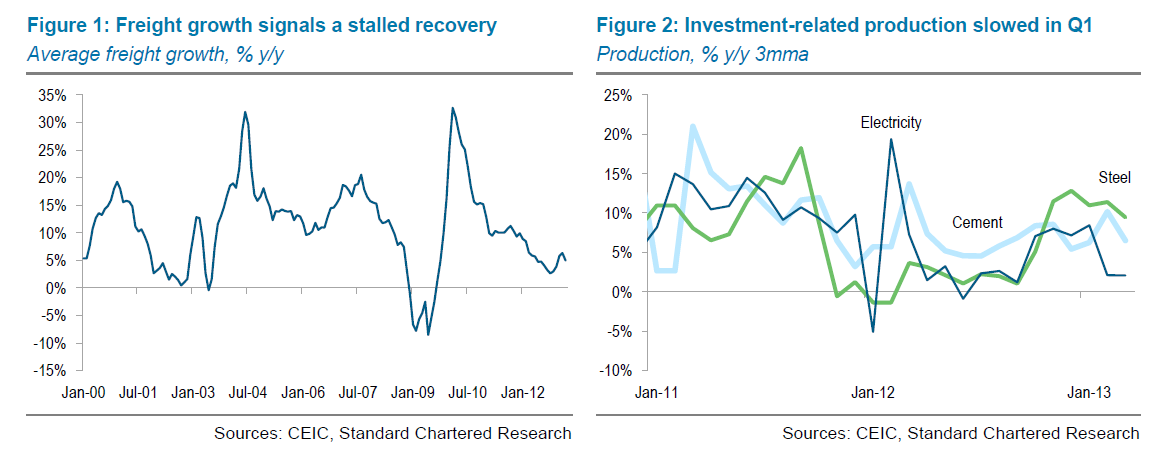

And why the cycle has stalled? Green sees five reasons:

Advertisement

The real-estate sector nationwide is still recovering slowly….Inventories in most of China‟s 40 biggest cities are falling, and we are seeing clear evidence of price rises in some cities…However, the inventory situation in many (mostly smaller) cities is not improving, so the construction recovery is slow. A national real-estate consultancy told us recently that there are no signs of a sales recovery in the 200 smaller cities it tracks (though it admits that the data is not great in Tier 3-4 cities).

The situation for public infrastructure is worse; we see limited growth momentum here. The market is still waiting for new official orders on the railway sector. Channel checks with companies making wheel-loaders and excavators suggest that their sales are still very weak, and we do not expect them to improve until activity has clearly recovered.

Local government investment vehicles (LGIVs) are likely facing serious cash-flow issues. With officially reported outstanding debt of CNY 12tn (USD 1.94tn), their interest payments this year alone will amount to some CNY 700bn. The central government has signalled that LGIVs will not be allowed to expand their bank funding this year, and trust companies have been told to stop lending to them (though it is unclear how strictly this rule is being enforced). A recent Renmin Ribao editorial instructed commercial banks not to enlarge their total LGIV exposures this year, and provincial bank regulators have been told to strictly monitor banks under their supervision.

…We believe that exports, which account for about 30% of industrial value-added (our estimate), are only really growing around 5-10%. As has been widely discussed, the recent headline export growth number of 20% was inflated by trade-financing and VAT rebate-seeking FX inflows masquerading as trade. Once recent moves by the authorities to reduce hot FX inflows and arbitrage flows take effect, a more accurate export picture will emerge (Local Markets Alert, 7 May 2013, ‘China – New SAFE rules: Less than meets the eye’).

Domestic consumption growth also faltered in Q1-2013. The causes of this are a subject of debate. The anti-banqueting and anti-corruption campaigns of the new leadership have had an immediate chilling effect on the restaurant and hotel trades, as well as luxury goods (though sales of expensive watches in Hong Kong are recovering). It is unclear how long the banquet freeze will last; those who know China‟s politics well argue that it is only a matter of time before such activity resumes, quietly and less extravagantly.

Given the shift to tighten on the property sector is already well underway and Phat Dragon expects a downdraft in construction from Q3, the year ain’t shaping up too well for China bulls.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.