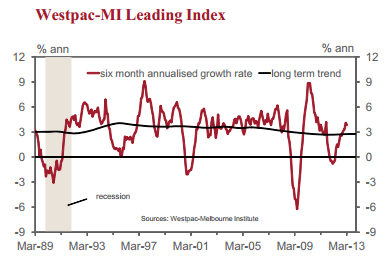

For what it’s worth, the troubled Westpac Leading Index continues to signal a boom ahead:

The annualised growth rate of the Westpac Melbourne Institute Leading Index, which indicates the likely pace of economic activity three to nine months into the future, was 3.9% in March, comfortably above its long term trend of 2.8%. The annualised growth rate of the Coincident Index, which gives a pulse of current activity, was 2.7%, slightly below its long term trend of 2.9%.

Ho hum. Even Westpac itself has given up on it:

Our chief concern is that this respectable growth momentum will not be sustained. Although only a partial picture, some Leading Index components have already shown softer readings since March – the sharemarket rally has faltered locally, US industrial production declined 0.5% in May, manufacturing materials prices were down in Q1 and overtime worked fell sharply. Updates on the remaining components due in coming weeks may offset this somewhat with the recovery in commodity prices earlier this year expected to lift corporate profits for Q1 and April expected to show a solid bounce in dwelling approvals. The April update of the Leading Index on June 19 will provide a more complete picture.

More generally, the next few months is likely to see the downturn in commodity prices and mining investment start to show a more pronounced negative impact. The ‘non-mining’ parts of the economy – housing and the consumer in particular – will provide some offsetting improvement. Our fear though is that ongoing weakness in non-mining business investment and a poor global backdrop means the overall mix will not be enough to counter the drag from the mining sector.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.