From the AFR this morning comes the news that:

Federal Treasury has downgraded its economic growth forecast for this year and next by a quarter of a percentage point, predicting a slowdown that would dent tax revenue and make it even harder to deliver a budget surplus.

As it finalises the budget’s economic forecasts, Treasury has been working on the assumption of 2.75 per cent growth for 2012-13 and 2013-14. In the October Mid-Year Economic and Fiscal Outlook, it forecast real GDP growth of 3 per cent in both years.

…A quarter point cut to growth in gross domestic product this year would reduce government revenue by $1.75 billion in the following year because of weaker corporate profits and jobs.

…A 2.75 per cent growth rate would be below the economy’s long-term average rate of just over 3 per cent and is at the lower end of the Reserve Bank’s February 3 per cent GDP forecasts for both years.

Treasury, which has been criticised in recent months for overly optimistic forecasting, is taking a conservative approach to economic forecasts in the May 14 budget.

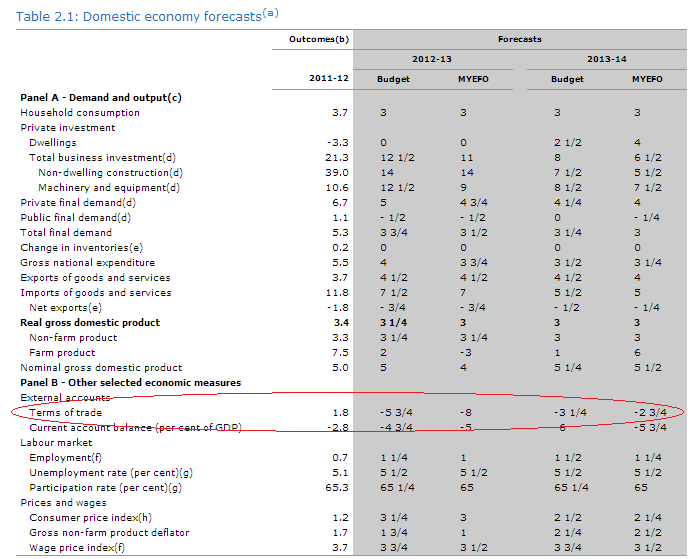

Conservative, eh? How much do you want to be they miss again, and by miles? We’ll have to wait and see on budget night, but the critical number in the budget will not be assumptions about growth. It will be the assumptions made about the terms of trade. In the MYEFO they were as follows:

The December national accounts has the terms of trade down 18.8%. The rebound since then has probably taken the fall back to 15% from the peak in 2011. As you can see, the Treasury badly underestimated the falls in the past two years and will dos o again if it continues with the methodology explained in the last MYEFO:

Considered from a medium‑term perspective, commodity prices are still expected to be elevated by historical standards, and will still provide an incentive to continue the expansion of low cost supplies in Australia and around the world. In Australia, around $65 billion of coal and iron ore projects are committed or have already commenced construction… The medium‑term projections for the terms of trade are based on a gradual decline in commodity prices as the supply of iron ore and coal steadily comes on line. This medium‑term methodology has been retained from the 2012‑13 Budget.

Since when did markets operate this way?Since when did the set up of current supply expansions versus declining demand expectations make this likely? Never and not.

I don’t know where this assumption of taking the lift up in commodity prices and escalator down came from but it is the opposite of traditional wisdom. Commodity prices take the escalator up and the lift down. Until that is the budget forecasts they are anything but conservative.