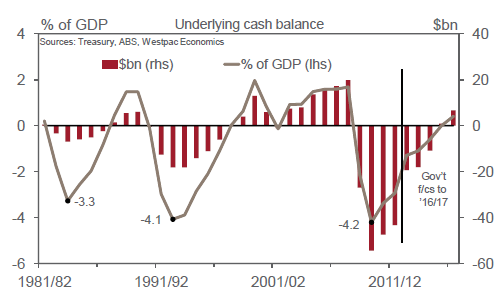

Well, the 2013-14 Federal Budget is in the bag and apparently Australia is headed back into Budget balance by 2015-16 and into surplus by 2016-17:

For this year rather than a small surplus we will see an $18 billion deficit and $19.4 billion miss from last year’s forecasts.

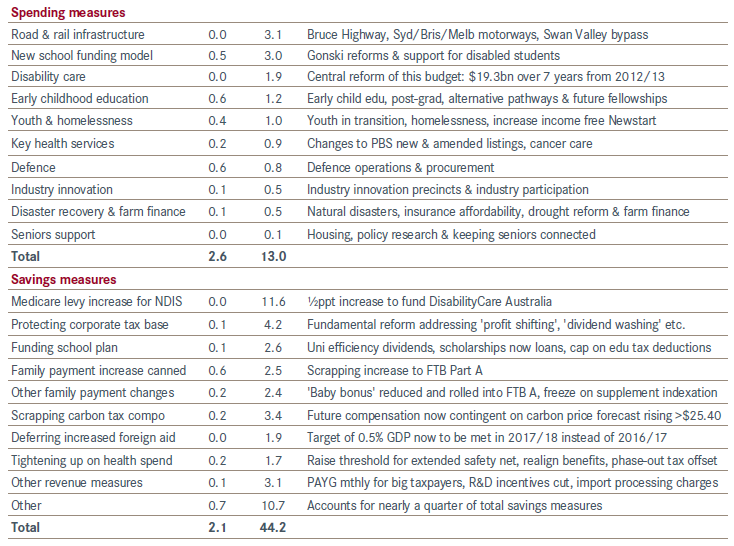

Here are the major items (both charts courtesy of Westpac, full report below):

To say that I am sceptical of the Budget forecasts is an understatement. Despite the Kouk’s bizarro reading, I see a number of potential problems with the Treasury’s forecasts, which appear to be based on unrealistic underlying assumptions and mis-reading of the stiff headwinds facing the economy.

First of all, consider the Treasury’s assumed growth in nominal GDP, which is forecast to expand from 3.25% in 2012-13 to 5.0% in both 2013-14 and 2014-15 (see below table).

For the uninitiated, nominal GDP is the dollar value of what’s produced and earned across the economy. It’s also the measure that drives taxation revenue. Nominal GDP grew by just 2.0% in the year to December, far below real GDP growth of 3.1%, which is the quantity of goods and services produced. While the fall in nominal GDP below real GDP is unusual, having happened only a handful of times since the late-1950s, it has happened twice under the current Labor Government’s watch – during the GFC and currently – on both occasions driven by sharp falls in commodity prices (reducing the dollar value of Australia’s exports) and the terms-of-trade (see next chart).

The terms of trade forecasts are very aggressive. they assume significant uplift for the March and June quarters for this year. An almost non-existent fall next year and 2% in 2014/15. These figures do not come terms with a China adjustment at all.

Indeed, the Budget recognises the unusual factors pushing down nominal GDP, noting the following in Budget Paper 1:

Nominal GDP growth has historically exceeded real GDP growth by around 2½ percentage points, but this relationship has reversed recently (Chart 3). Nominal GDP grew by only 2.0 per cent through the year to the December quarter 2012, well below the rate of real GDP growth of 3.1 per cent. This was the third consecutive quarter where nominal GDP growth was outpaced by real GDP growth, the first time this has happened in at least the past half‑century.

Chart 3: Difference between nominal and real GDP growth (through the year)

Source: ABS cat. no. 5206.0.

Notwithstanding some volatility in iron ore prices toward the end of 2012, non‑rural bulk commodity prices have fallen over the past twelve months. Iron ore spot prices in early May 2013 are around 30 per cent lower than their peak in 2010‑11, while thermal and metallurgical coal prices have fallen from peaks in 2008‑09 and 2010‑11 respectively. With overall export prices expected to continue to weaken over the forecast period, the terms of trade are expected to decline by 14 per cent from their peak in late 2011 to 2014‑15, placing continued downward pressure on nominal GDP growth.

So according to the Treasury, commodity prices are forecast to continue their decent from 140-year highs, dragging down nominal GDP, yet nominal GDP growth is still forecast to rebound to 3.25% in 2012-13 (from only 2% in the year to December 2012) and to 5% in both 2013-14 and 2014-15? Moreover, nominal GDP is expected to rise to levels that are well above real GDP throughout the forecast period, from -1.1% below real GDP in the year to December 2012?

In light of the ongoing slump in the terms-of-trade, the Treasury’s nominal GDP forecasts appear highly optimistic. According to the Budget papers, a 1% change in the value of goods and services generates a $2.8 billion shift in the budget bottom line in the first year and a $7 billion shift in the second. Therefore, by assuming stronger growth in nominal GDP, the Treasury has likely overestimated Budget revenues and the path back to surplus.

Admittedly, there is one potential saving grace for the Treasury’s forecasts. In the event that the Australian dollar depreciated sharply against other currencies, the Australian dollar value of exports would rise (other things equal), boosting the dollar value of goods produced and nominal GDP, offsetting the fall in commodity prices.

While the Australian dollar is likely to depreciate as the interest rate differential narrows and the mining boom unwinds (possibly removing Australia’s ‘safe haven’ status), one wonders why the Treasury doesn’t err on the side of caution and base its revenue forecasts on more moderate nominal GDP growth, rather than a quite bullish 5% growth?

Weirdly enough, Wayne Swan was out yesterday afternoon declaring that:

…the unpredictability of budget forecasts, just hours before unveiling his sixth and possibly last federal budget.

Amid opposition claims that tonight’s budget numbers won’t be reliable, the Treasurer said unexpected changes in financial conditions could wreak havoc on economic forecasts.

“The truth is that the global economy is capable of changing dramatically, quickly, and having different effects on the economy at different times,” Mr Swan said, as he reflected on the toll the global financial crisis had taken on his past budgets.

Again, given these uncertainties, why is Treasury still plugging in optimistic forecasts?

The other area of concern with the Treasury’s outlook relates to the upcoming peak and then decline of mining capital expenditures (capex). Treasury remains of the view that mining capex will unwind in an orderly manner and that overall jobs growth will improve as the non-mining economy picks-up steam:

The resources sector has responded to the unprecedented growth in demand for resources from Asia with the largest investment boom in Australian history. Total resources investment surged to over $100 billion in 2011‑12, more than 600 per cent higher than it was a decade ago. LNG projects are increasingly dominating the pipeline of investment, driven by the demand for energy in Asia, but large‑scale investment in iron ore and coal extraction and transportation is also contributing to a lift in export capacity.

Resources investment is expected to peak in 2013‑14 at record highs, and then remain elevated through to at least the middle of the decade. The pipeline of resources investment remains substantial, with over $260 billion of investment either committed to or under construction. While resources investment will begin to detract from growth after it passes its peak, the resources sector will continue to make an important contribution to growth as the record level of investment fuels exceptional growth in resources production and exports…

Employment growth is expected to strengthen as growth picks up in some non‑resources sectors of the economy and the level of employment remains high in the resources sector. Employment in Australia is expected to grow by 1¼ per cent to the June quarter 2014 and 1½ per cent to the June quarter 2015, and over 350,000 jobs are expected to be created over the forecast period. However, with the resources sector transitioning to the less labour intensive production phase, and the high Australian dollar still weighing on many sectors of the economy, the unemployment rate is expected to rise by ¼ of a percentage point to 5¾ per cent in 2013‑14, but then stabilise at that level over the remainder of the forecast period and remain amongst the lowest in the developed world…

Given that around 10% of the Australian economy are employed in mining-related activities, mostly in areas unrelated to actual extraction (e.g. construction workers, engineers, and mining services), and that mining capex will soon go into an as yet ill-defined but likely sharp decline, Treasury’s steady-as-she-goes employment projections also appear overly optimistic.

unconventionaleconomist@hotmail.com