Gerard Minack is out with a sobering note on the mining investment cliff this morning that, if anything, too bullish! Enjoy:

A precipitous fall in mining-related capex is the most plausible domestic trigger for an Australian recession. This risk seems greatest 12-18 months ahead. However, new survey work by our research team suggests that mining-related spending could begin to decline this year. Increasing signs that investment spending will be a drag on growth this year, as well as recent weak domestic data, support the RBA resuming its easing cycle. Rate cuts, weakening domestic activity, and concerns about mining investment, may also trigger a material A$ decline.

Australia is now in the second leg of the mining boom. The first leg was the rise in the terms of trade (the ratio of export prices to import prices), which drove real national income growth 18% faster than GDP growth over the past decade. With commodity prices now, in our view, past their peak, the terms of trade have swung from being a structural tailwind, to a structural headwind. Real national income has fallen through the past five quarters, even as real GDP has risen by 3.8%.

Investment spending has taken over as an engine of domestic growth. Mining investment spending is an unprecedented share of GDP. Investment spending contributed significantly to growth over the past few years, even after allowing for the import component of investment spending.

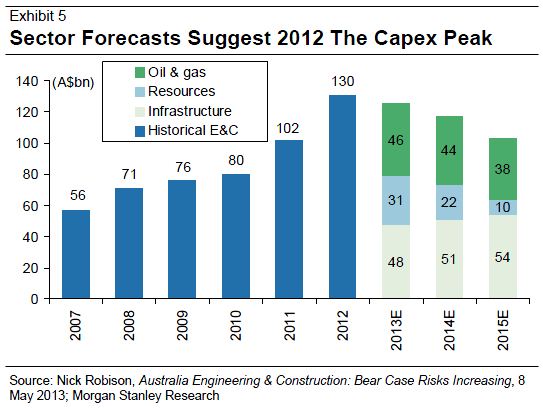

The key forward-looking question is how long the investment boom persists, and how quickly it deflates. Our colleagues, led by Nick Robison, have undertaken a survey of mining companies which suggests rising risk of a sharp decline. This survey, along with other macro indicators, suggest that the RBA will have to continue easing policy, and the A$ may weaken.

Perspicacious readers will note that this investment peak is higher and the decline slower than others we have seen from ANZ, NAB and CBA. Presumably we can put this down to different definitions of investment categories. I maintain that the more bearish outcomes are the most likely because, as Stanley Drukenmiller said last night, falling commodity prices are not a correction, they are a trend as China rebalances. So we’re likely to see increasing pressure to cut projects (as is the case with Rio today) not decreasing.

Anyway, the Morgan Stanley cliff is still enough to have Minack contemplating recession:

Advertisement

All this suggests that mining-investment may become a drag on growth this year. While it is unlikely to be a severe headwind in 2013, an earlier peak to mining investment also raises the risk that the decline in 2014 could be significantly more damaging than we have in our current forecasts.

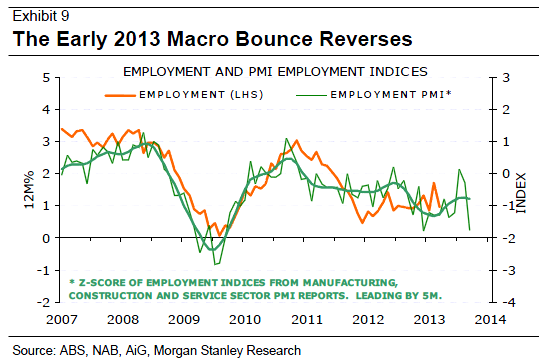

…It is, in our view, too early to forecast recession in Australia next year. However, it seems that the risks to the investment outlook are slanted to the downside. Moreover, recent domestic data have weakened, reversing much of the

improvement apparent in early 2013 statistics. Employment is a key indicator, and hiring intentions in the monthly business surveys fell sharply in April.

This weakness, along with benign recent inflation data, prompted the RBA to resume its easing cycle at the May board meeting. We now think that the Bank will likely keep easing if – as our survey suggests – the outlook for investment deteriorates in coming quarters. At the start of the year we had expected that the cash rate target would be lowered to 2½%, a forecast we regret changing on the back of the solid January-February macro news. It now seems possible for the cash rate to fall to 2-2½% later this year.

The A$, however, remains a wild card. The currency has unexpectedly held up over the past 18 months as commodity prices have softened, and Australia’s rate differential with trading partners has narrowed. The prospect of further rate cuts, driven by domestic weakness, increases the chance of the A$ moving back in line with its usual fundamentals. That would imply a decline to around US$0.90 in our view. If the A$ falls sooner, rather than later, it would commensurately reduce

the need for the RBA to cut rates aggressively from current levels.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.