From ANZ comes a note this morning offering a guide to the ABS capex report due on May 30 that I discussed last week. First for total capex:

The Private New Capital Expenditure and Expected Expenditure (CAPEX) release on 30th May includes firms’ sixth estimate for 2012-13 investment intentions and their second estimate for intended capital spending for 2013-14. There is always uncertainty around these estimates and realised investment and for this reason, firms’ ‘raw’ investment intentions must be adjusted for historical biases (using so called ‘realisation ratios’). This is a highly subjective process and the figures below need to be interpreted in broad terms.

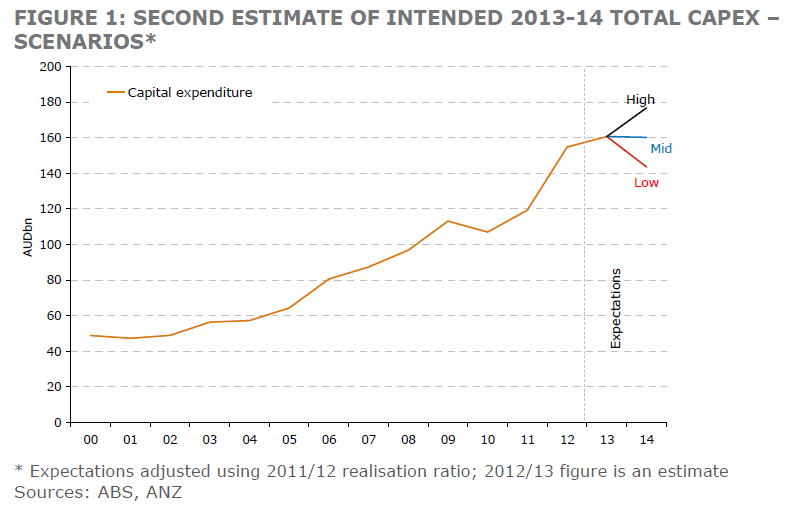

Broadly speaking, a raw aggregate nominal investment intention for 2013-14 of around AUD145bn would imply actual investment of around AUD160bn, after accounting for historical realisation bias. This would represent no growth relative to expected investment for 2012-13 (Figure 1). (This uses 2011-12 realisation ratios.) Such an outcome would be broadly in line with our current forecasts and would support the view that monetary policy could still afford to be eased a little more.

A raw aggregate investment intention of around AUD130bn for 2013-14 would imply a decline in actual nominal investment of around 10% y/y. This would be a sharper fall than currently expected by the RBA.

In contrast, a raw aggregate investment intention of around AUD160bn for 2013-14 would imply growth of around 10% y/y compared with 2012-13. This would be a stronger result than both we and the RBA currently forecast and would support the view that there is less scope for further RBA policy easing. Given the weaker profile for mining investment, however, the likelihood of this scenario eventuating appears unlikely.

My own view is that the “realisation ratios” this year are unlikely to be historically consistent. Given the range of developing challenges for the economy amid a falling terms of trade, I reckon investment is more likely to undershoot than in other years. Still, that is something that will become apparent only in retrospect.

Advertisement

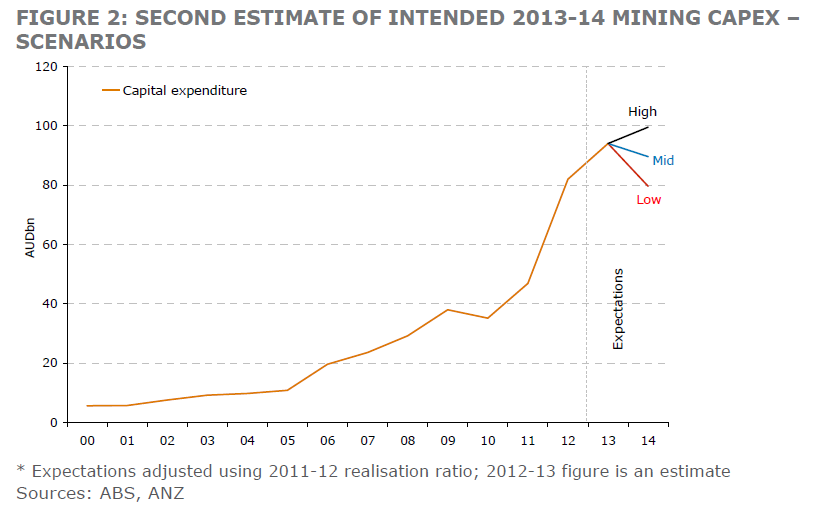

For mining in particular, ANZ reckons:

A raw mining CAPEX intention of around AUD100bn or above for 2013-14 would be higher than we expect and would imply growth of around 5% y/y on 2012-13 expected capital expenditure (Figure 2). An estimate of around AUD90bn would be broadly in line with our expectations, suggesting a decline in mining investment of around 5% y/y in 2013-14. A raw estimate of AUD80bn or below would imply that mining investment would fall at least 15% y/y in 2013-14, suggesting that investment in this sector would be a much bigger drag on growth over 2013-14 than we are currently forecasting. We remain of the view that resources and related investment will decline more sharply in the second half of 2014 and over 2015 as investment in the LNG sector wanes.

This is the big one for me and, in my view, markets. Even if there is evidence of rebalancing with capex rising in non-mining sectors, if mining capex undershoots then it will show the mining investment cliff is real and imminent. That’ll immediately pressure the dollar.

Conversely, if it comes in strong, it’ll be short covering time.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.