So rhetoric works sometimes it seems and my hosing recovered somewhat overnight with the big fall in the Aussie and Dr Copper going the way of my position. It was actually bad trading and the type of trading that only a big balance sheet, small positions or a big fund can really justify. But I deviated from my usual trading style because I needed to show someone that you could make money trading this way but it is not ideal.

Anyway the fall in the Aussie overnight and the huge almost 4% fall in the price of copper along with the big build in crude oil stocks in the US together with weak data and the Fed’s comment that it could increase or decrease the size and scale of its bond buying really does signal that the little global economic sweet spot of a few months back has evaporated.

Indeed I spend a lot of time looking at the Citibank economic surprise indices for various nations and as I noted recently data has been printing much weaker across the globe since about mid-March. Last night was no exception with the canary in the coal mine, as the team at Business Insider put it, was the release of the Korean export data which while positive was much weaker than expected printing just 0.4% YoY against the punditry’s 2% expectation. Clearly Korea has close ties with Japan and China and clearly Korea is a good lead on overall global trade so this data is a concern.

Add in a bit of weakness in the ADP employment survey which undershot with a 119,000 print against the 150,000 expected and the ISM manufacturing PMI which fell to 50.7 from 51.3 last month. It has been and remains our hypothesis that the Fed and others free money is goosing stocks higher but in the end the economy is where it is at. Assets like the Australian dollar which are still tied to the global growth outlook and perceptions of the miracle that is the Australian economy are vulnerable from this economic weakness.

Indeed stocks should be vulnerable too and at some point they will likely reacquaint themselves with reality. Last night saw a little bit of reality creep into traders minds with the Dow off 0.94%, the Nasdaq down 0.89% while the S&P was 15 points or 0.91% lower at the still heady heights of 1583. In Europe the FTSE was higher on the back of bank moves up 0.32% while the continent was largely closed for May Day.

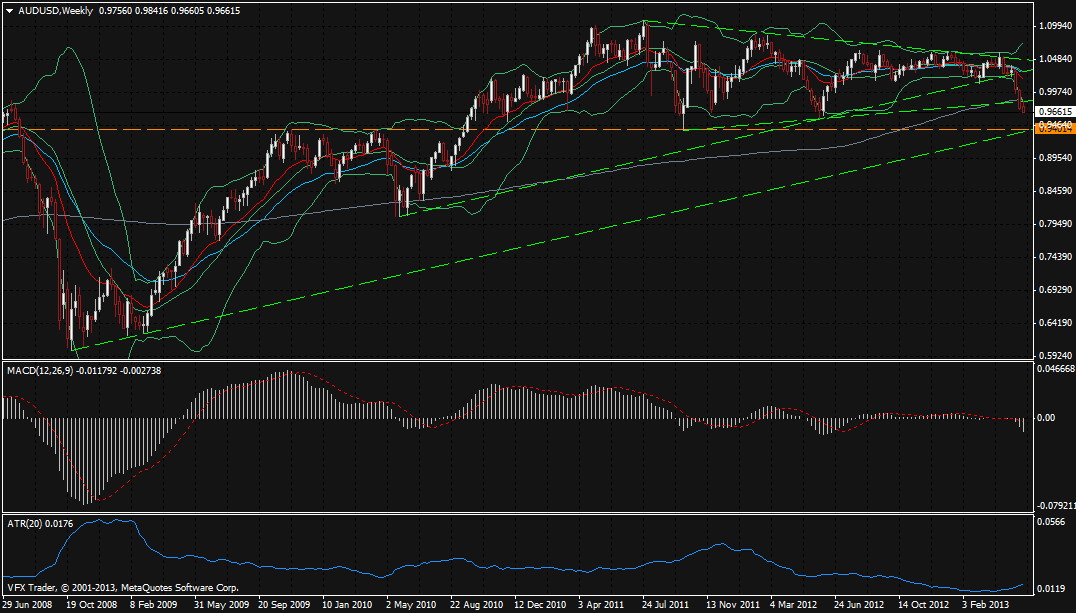

But it is the Aussie which has been my focus this week and the crash in the AUDCAD rate which we flagged yesterday and which occurred yesterday evening Sydney time as you can see in the chart below really does signal that the worm is turning for the Aussie dollar. The AUDUSD looks biased back toward the low of the past few weeks at 1.0219 and should it close the week below this level then it would certainly suggest that the big weekly uptrend we highlighted back on Monday and turn the outlook significantly lower.

My target is 1.0233 for this cross.

On the AUDUSD specifically I was sent a chart of the Citi Chinese Eco surprise index versus the Aussie dollar earlier in the week – something that I hadn’t thought to connect myself but it tells a story and the story fits with my view that the Aussie is under pressure and at risk of the legs of its positivity being kicked over. So as I note above, the AUDUSD needs to hold above the recent low and the trend line from May 2010 or the outlook turns technically.

Turning to the euro, it managed to hit 1.3242 at one stage overnight but has since sunk back to 1.3182. The candle is a warning to the bulls that momentum might have stalled and this certainly makes sense given the ECB meeting and announcement tonight where the market widely expects rates to be cut. In the face of this expected cut the euro’s strength has been baffling but then again the data from the US hasn’t been so flash the past little while which is clearly what they FX markets have been focused on:

USDJPY looks to us to be biased lower still although it is steadfastly flirting with but rejecting the break of 97 which is necessary to accelerate things to the downside.

On commodity markets as discussed the fall in copper was huge and it continues to signal a rethinking on the outlook for global growth. Gold has backed off the resistance zone of 1475 I highlighted a week or two ago falling 1.76% or about $25 to $1451. Silver was off 3.47% to $23.53 and Nymex crude was down 2.72% on the back of the huge build in stocks which rose 6.696 million Bbls against the expectation of just a 0.8 million build. In Ags, corn was 0.15% lower with bigger falls in wheat and soybeans which dropped 1.56% and 2.06% respectively.

Data

In Australia building permits, export and import prices and then tonight the ECB interest rate decision and initial jobless claims.

Twitter: Greg McKenna

Disclaimer: The content on this blog should not be taken as investment advice. All site content, including advertisements, shall not be construed as a recommendation, no matter how much it seems to make sense, to buy or sell any security or financial instrument, or to participate in any particular trading or investment strategy. Any action that you take as a result of information, analysis, or advertisement on this site is ultimately your responsibility and you should consult your investment or financial adviser before making any investments.