It’s was a humbling afternoon for Australian economics yesterday with just 8 of 29 surveyed economists getting the rate cut right. I’ll claim this one, as I said last week:

March quarter GDP is now irrelevant. The current round of easing has always been forward looking to the extent that it is anticipating the mining slowdown. Forecasts for the mining investment cliff have clearly worsened in the month and the offsetting growth areas have stalled as well. I agree with Bill Evans that the Board would prefer to wait a month but frankly the data is saying cut.

In my experience the Board follows the data. Either way, it’s coming.

There are many others whose heads exploded at 2.30 yesterday afternoon. Chris Joye was one:

There are two essential reasons why the RBA cut rates to 2.75 per cent when the internal staff were likely ambivalent about any urgent need to do so. The first is because with core inflation around the bottom of the RBA’s target band, the central bank felt it could offer more monetary stimulus without, it alleges, risking destabilising equities, bonds or housing bubbles.

The second explanation is because it was the demonstrably easier decision for the RBA’s board to make. The tougher call would have been to hold its nerve. And this RBA has a track-record of taking the easy route.

Chris, who is the AFR’s best commentator these days by some distance, and who tells a good story about global central bank experimentation in the same piece, somehow managed to write 1300 words without once mentioning the exchange rate. Splat!

Paul Bloxham at HSBC faced a double whammy of having called the rates cycle bottom over the past six months and that the RBA would not cut this week However, he got the rationale for his miss spot on:

They also made a very clear reference to the unusually high AUD. As they suggested, the AUD has been little changed at a historically high level, ‘which is unusual given the decline in export prices and interest rates’. The high AUD has long been a concern of the Reserve Bank, and the recent low inflation print left them room to move to try to do something about it. It appears that this was a key motivation for today’s cut. In assessing where rates will go from here, many of our concerns remain. Low rates are lifting the housing market and housing prices. Today’s cash rate cut will support that even more.

But a glutton for punishment, he’s also redoubled his bet, delivering another ruptured melon.

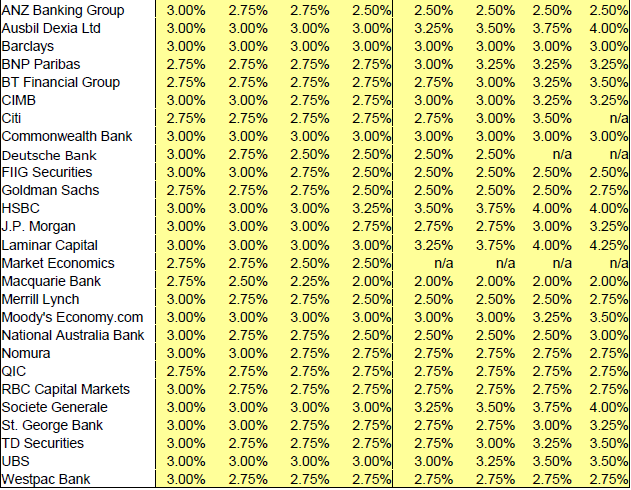

The list of others suffering from cognitive detonation is so long it’s easier to simply provide the chart courtesy of Bloomie:

Those with lumps of brain on the lapel include Ausbil Dexia, Laminar Capital and Soc Gen. Everyone else has had a mild embolism but remains at the desk. Those with intact heads include BNP, BT, Citi, GS, Kouk, Mac Bank and QIC.

Thinning ranks indeed.

Finally, our old mate Bill Evans of Westpac claimed a partial win:

The Reserve Bank Board decided to lower the cash rate by 25bps to 2.75% at its May meeting. Westpac had expected that the Board would wait another month before making this move to assess further evidence particularly around business investment, the labour market and the global economy. However we did argue that the case had already been made for a cut and the debate was now purely around tactics rather than the need for lower rates. The overnight cash rate has now reached 2.75% which was the target we nominated in May last year when the consensus view was that rates would bottom out at 3.25-3.5%.

…Our long held target of 2.75% for the cash rate has now been reached. We have consistently argued that 2.75% would be the low point but that risks are to the downside for the cash rate. We are currently assessing that outlook.

In short, stand by for Westpac is issue more rate cuts calls. They’ll need them.