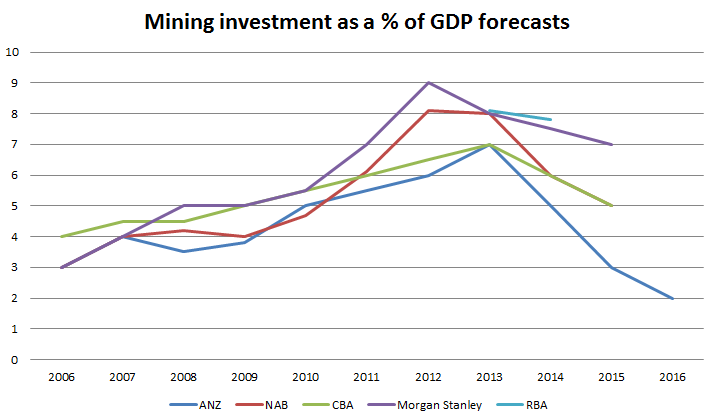

I’ve written a piece on the likelihood of recession in 2014 for Intelligent Investor this week and in the process drew up the following chart on the current forecast ranges for the mining investment cliff:

Each of the forecasts uses slightly different investment definitions hence the data range. There’s a bit of guess work in the forward GDP denominator as well so the chart should be taken as a rough guide not specific forecast. As you can see, there is still great uncertainty around the pitch of the slide, some around timing too, although all agree we’re more or less at the peak. All of the figures are based upon committed projects only and would change significantly if more come on stream. Some will, like Rio’s 360 Pilbara expansion, but in the main the pipeline of projects under consideration will keep drying up as the terms of trade trends downwards.

What matters is that each path shows mining investment not just plateauing but detracting from growth. This is a double whammy for GDP given mining investment has driven so much of it in the last few years. Not only must a replacement be found to cover the lost growth, more must be found to actually grow.

The RBA (and ABS) path is manageable for the economy if it were to persist without much further deterioration. The current modest upward trend in non-mining capex will be enough to keep the economy growing at a near trend pace though to the 2015 ramp up in LNG net exports.

The Morgan Stanley path is a challenge at approximately 1% of GDP withdrawn for the next two years but is still probably manageable at sub trend growth seeing us through to 2015. The CBA trajectory is actually similar to MS but from a lower peak.

The NAB trajectory is starting to look worrying. Facing anything like a 3% fall in mining investment as a proportion of GDP over two years would be very difficult. There is little sign at this point that non-mining investment is accelerating enough to fill such a hole. As such, growth could easily slow beneath 2%, unemployment would climb, and the economy would be operating at “stall speed”. There would be a high risk of negative business cycle dynamics overtaking growth as unemployment fed back into asset prices and bad loans.

The ANZ forecast is obviously a real worry. Before you dismiss it, remember that 2% mining investment of GDP is the long term mean. If the ANZ Major Projects report proves to be right then recession is a near certainty. Interest rates will go to undreamed of lows. The dollar will have to fall a long way and fiscal spending will have to ramp up.

That’s the final point to make. Each of these forecasts will shift if the macro settings also change. Lower rates will help consumption. Public infrastructure development will also be very important. But most important will be a lower dollar to trigger more mining and non-mining tradables investment.

The importance of getting the dollar down NOW cannot be overstated.