Fitch Ratings agency has today warned Australia’s banks that that they need to improve their funding mix if they are to meet Basel III liquidity requirements and retain their coveted AA- credit ratings:

Fitch Ratings-Sydney/Singapore/London-09 May 2013: Australian banks need to continue to improve their funding mix to meet Basel III liquidity requirements, especially as the revised proposals from the Australian Prudential Regulation Authority (APRA) stick to the original implementation timetable and liquid asset definitions, Fitch Ratings says.

We expect banks to lengthen their wholesale funding to meet the liquidity coverage ratio (LCR) and net stable funding ratio (NSFR) requirements, because deposit costs remain high and wholesale funding spreads have fallen in recent months. As a result, the improvement in loan-to-deposit ratios over the last five years, from a peak of around 170% to below 140%, may slow down – and possibly even reverse for some banks. However, funding stability should continue to improve, with better asset/liability matching.

Adhering to the original timeframe to adopt the LCR in 2015 and NSRF in 2018, rather than a phased implementation as permitted under the revised Basel rules, should address a key negative ratings driver for Australian banks. Their reliance on wholesale funding, particularly from offshore markets, is high compared with international peers. This leaves them more exposed to a dislocation in international wholesale funding markets. We expect further improvements in funding profiles; but structural issues, such as Australia’s compulsory pension scheme, mean wholesale funding is likely to remain important.

APRA’s proposals to adopt some softer stress assumptions for the LCR under the Basel Committee’s recent revisions are unlikely to change the banks’ holdings of liquid assets to any great extent. The banks have already built substantial liquidity buffers against financial market stress. The revised rules appear to be a sensible recognition of the actual inflows and outflows experienced during times of stress.

The proposal not to exercise the discretion to allow some lower-rated corporate debt, equities and residential mortgage-backed securities to come into the definition of high-quality liquid assets is consistent with APRA’s conservative approach to bank regulation. The revised Basel rules allow for a new ‘Level 2B’ category of assets, which we expect to be typically less liquid under distressed conditions. Some compositional change in liquidity buffers may occur once APRA’s proposals are finalised.

To address a shortage of government bonds and other qualifying liquid assets, the central bank will provide a committed liquidity facility for the purposes of meeting LCR requirements. We expect there could be changes to the quantity of banks’ liquid assets once the framework for this facility and its size for each bank are set by APRA. Banks are expected to take all reasonable steps to meet their LCR requirements before relying on the facility.

APRA released its second consultation on Basel III liquidity implementation on Monday, outlining its proposed rules.

I have emphasised the key parts of Fitch’s release: the explicit warning that if the banks are to tilt their funding mix away from deposits towards wholesale (offshore) debt, then they must significantly extend the duration (length-to-maturity) of this debt in order to reduce rollover risk in the event that global capital markets seize-up, like they did in the wake of the GFC.

As noted by Houses & Holes recently, deposit growth has slowed over the past six months, growing at only 6.9% in the year to March 2013. Should credit growth pick-up from current low levels, or deposit growth continue to slow, Australia’s banks will soon be forced to seek wholesale funding from offshore, placing them in the sights of the ratings agencies.

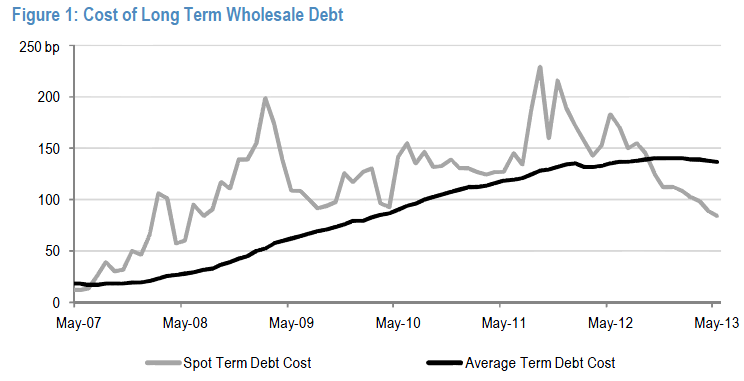

The good news is that wholesale funding costs continue to fall as the global chase for yield continues. From JPMorgan:

unconventionaleconomist@hotmail.com