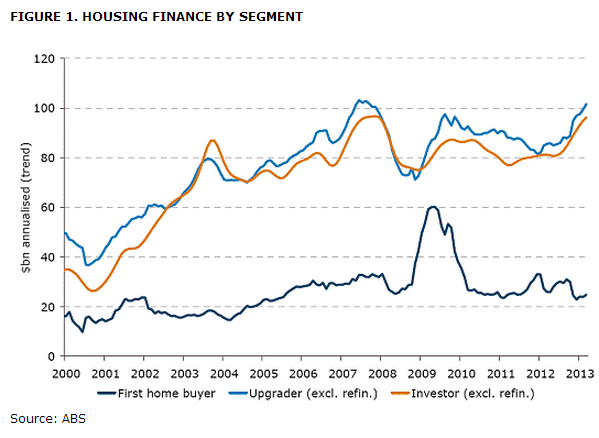

As noted yesterday by ANZ (see next chart), the ABS’ housing finance figures for March 2013 revealed ongoing weak demand from first home buyers (FHBs).

While the number of FHB mortgage commitments rose by 11% in March, they were down by -16% over the past year and were -32% below the 5-year moving average (5YMA):

And despite the modest lift in numbers, the proportion of total owner-occupied loans going to FHBs fell to -14.2%, which was the lowest reading since May-2004 (see next chart).

The overall slump in FHB mortgage demand has been driven by New South Wales and Queensland, where the number of commitments remain just above the record lows set in January, and have fallen off a cliff since FHB grants on pre-existing dwellings were removed in October 2012. Victorian FHB mortgage demand has also fallen quite sharply since mid-2012 (when FHB subsidies on newly constructed dwellings were removed), whereas Western Australia’s is in an uptrend (see next chart).

The next chart, which presents the same data on a 3-month moving average (3MMA), shows these trends more clearly:

As a percentage of total owner-occupied finance, the number of FHB commitments in New South Wales and Queensland recovered ever so slightly in March, but remained near the record low levels set in January. By contrast, FHB demand in Perth continues to boom (see next chart).

Again, the same data is shown on a 3MMA basis in order to smooth volatility:

We’ll no doubt see a false recovery in Victoria before July as the FHOG shifts from existing to new homes there as well. Then a collapse in July. Over the long term, rising home prices and falling FHB share presents potential headaches for policy makers, who may soon come under pressure to arrest the slide in FHB demand and re-institute subsidies under the false pretense of improving housing affordability.