It seems a little bit of reality goes along way in Australia with the May consumer sentiment number crashing in the wake of the Federal Budget, down 7%. The full release is worth a read:

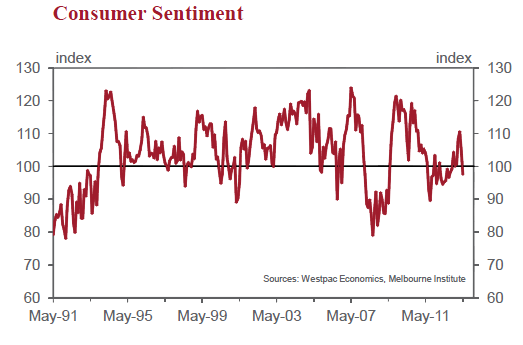

This print pushes the Index back into a range where pessimists outnumber optimists for the first time since October 2012. It is the lowest read since August 2012. Over the last 2 months the Index has fallen by 11.7% to fully reverse the promising 9.0% increase we saw in February and March.

Of course, the remarkable aspect of this result is that it is the first read of the Index since the Reserve Bank cut the cash rate by 0.25% on May 7. Absent any other major influences, we would have expected a solid boost to the Index following that rate cut.

However, since the rate cut we have seen the announcement of the Federal Budget.

In this survey we added an additional question around respondents’ assessments of the Budget and the results confirm our reasonable assumption that this weakness in confidence is being driven by a sharply negative response to the Budget.

In this survey we added an additional question around respondents’ assessments of the Budget and the results confirm our reasonable assumption that this weakness in confidence is being driven by a sharply negative response to the Budget.

We expect that the dissatisfaction is not only due to concerns around some of the savings measures in the Budget but also the sharp deterioration in the fiscal position, indicating renewed fears about the overall state of the economy. These concerns are also likely to have been fuelled by the surprise fall in the Australian dollar before and during the survey period. We will have further evidence around this issue with tomorrow’s release of the Westpac Melbourne Institute Index of Unemployment Expectations.

One of the main reasons why we assessed that the Reserve Bank was likely to hold rates steady in May choosing to move in June was to get some “clear air” between the rate cut and the Budget.

There was a genuine risk at the time that the negativity around the Budget would overwhelm any expected positive response to a rate cut. The Bank, however, has argued that it has further scope to ease. This result points to the need to use that scope.

The survey was conducted over the period 13 – 18 May. That means that 2 days (May 13 and 14) were effectively prior to all Budget details being known and 4 days (May 15–18) covered the post Budget period.

The Index was actually 1.8% higher in the post Budget period than in the pre Budget period. That result indicates that the damage from the Budget occurred even before all details were known as respondents reacted to pre Budget media coverage of the fiscal deterioration and some of the likely savings measures. There is some modest comfort for the government that the actual Budget details saw Sentiment slightly more positive than before its release but, nevertheless, still significantly negative.

Our own special question around the Budget in the survey indicated that 44% of respondents assessed that the Budget would make them worse off with only 5.4% seeing it as improving 22 May 2013 their position (The balance of the respondents were neutral). We have been conducting this separate Budget question since 2010 and this response is by far the most negative.

While other issues such as the employment report; the share market and house prices may have influenced the result at the

margin we expect that the Budget and the associated fiscal deterioration have been the dominant drivers of this sharp drop in confidence.

The key issue for the economic outlook is whether this response represents a short term reaction to a Budget that will be forgotten in a couple of months or whether the Budget Blues will linger for some time. The take out for us from this surprisingly sharp response is to emphasise the fragility of the confidence of the household sector , particularly at a time of near record low mortgage rates. Furthermore, because we expect that the negative response was fuelled not only by dissatisfaction with some savings measures in the Budget but also the deterioration in the fiscal position and the direct implication for the state of the economy this weakness is likely to persist for some time.

A clear illustration of the damage which the Budget has caused to hopes for a boost from the rate cut is demonstrated by the 9.7% fall in the confidence of those respondents with a mortgage despite receiving a 25 bp cut in the variable mortgage rate.

All components of the Index fell in May. The sub indexes tracking views on “Family finances compared to a year ago” fell by 8% and “Family finances over the next 12 months” fell by 7%.The economic outlook also deteriorated – down by 13.4% over the next 12 months and 6.9% over the next 5 years. “Whether now is a good time to buy a major household item” was down by 1.3%.

In comparing the pre and post Budget prints on these components we note that there was a modest improvement in how families perceived their finances while they were even more concerned around the economic outlook following the release of the Budget. The larger than expected deterioration in the fiscal position which was revealed on Budget night might explain why respondents were even more negative on the economy having seen the full details.

So, despite 200bps of rate cuts and ceaseless prattle about it being all good from all quarters, the fiscal instability canary has reminded the kids once again that Australia is not not what it used to be.

In fact, sentiment has crashed out of its uptrend and is now well below where it was when the rate cuts began:

Advertisement

And versus the average of previous cycles, is very sick indeed:

Advertisement

Something is wrong and everybody who is not paid to say otherwise knows it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.