ANZ offers a useful guide to why Chinese trade numbers are getting whack:

China’s trade growth remained strong in April, following a surge in the past two quarters. Today’s trade data also defies the weak trade data reported in other regional economies, suggesting capital inflow imbedded in trade remains unchecked.

Meanwhile, the port throughput data remained soft for the past few months, suggesting that the real demand has not yet fundamentally recovered. The inconsistency between port throughput and the headline trade growth shows that many Chinese exporters could have over-invoiced their trade value to take advantage of the interest rate differentials between onshore and offshore markets, and the RMB’s steady appreciation since July last year.

China’s FX regulator recently posted a new regulation (effective on 1 June) to crack down on these speculative capital inflows embedded in trade, which may help China’s trade growth return to its true level.

In our view, the RMB exchange rate should see weakening bias going forward if the ‘hot money’ inflows were under control. We reiterate our view that an overly strong RMB, especially amid a weak economic recovery and a sharp yen depreciation, is not in China’s interests. If it is the strong RMB that attracts such speculative capital inflows, the PBoC will need to de-peg with the USD and return to its exchange rate policy back to referencing to a basket of currencies.

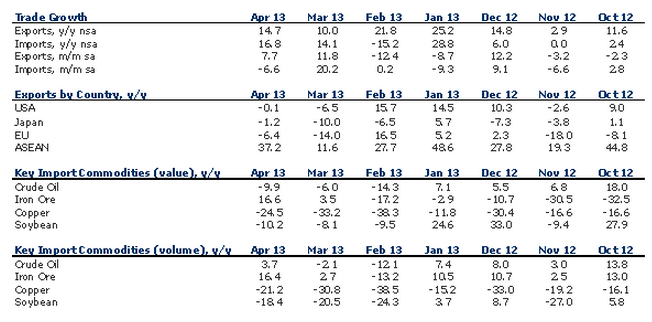

Note in the below chart the real trade numbers with major nations:

ANZ Quick Reaction – China April Trade Data by Belinda Winkelman