Goldman has gone short gold and US 10 year treasuries:

Gold unfazed by Cyprus, recent slowdown in US recovery

Over the past month, events in Cyprus have triggered a resurgence in Euro area risk aversion while US economic data has started to disappoint. Remarkably, gold prices are unchanged over that period, despite US 10-year TIPS yields back at their lowest level since late 2012, highlighting how conviction in holding gold is quickly waning.Turn in gold prices accelerating; closing our long gold position

Given gold’s recent lackluster price action and our economists’ expectation that the acceleration in US growth later this year to above-trend pace will support US real rates, we are lowering our USD-denominated gold price forecast once again. Our new forecast is further below the forward curve with year-end targets of $1,450/toz in 2013 and $1,270/toz in 2014.Initiating a short COMEX gold position as our ECS Top Trade #8

While there are risks for modest near-term upside to gold prices should US growth continue to slow down, we see risks to current prices as skewed to the downside as we move through 2013. In fact, should our expectation for lower gold prices continue to prove correct, the fall in prices could end up being faster and larger than our forecast, as aggregate speculative net long positions across COMEX futures and gold ETFs remain near record highs.

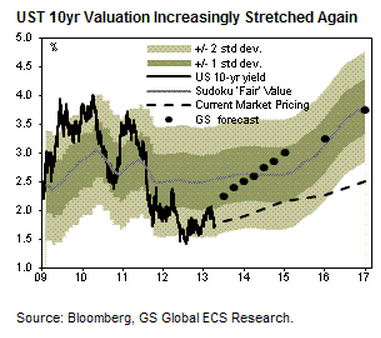

And for 10 year treasuries the rationale is as follows:

Here’s the chart for Goldamn’s forecast curve:

This strikes me a barmy. I see no way that we’re going to see this kind of normalisation in the US yield curve. Rising mortgage rates will bash housing, the rising USD will bash exports. Diminishing monetary stimulus will bash equities.

The call on gold is on a stronger footing as this mock stability endures in markets for a while.