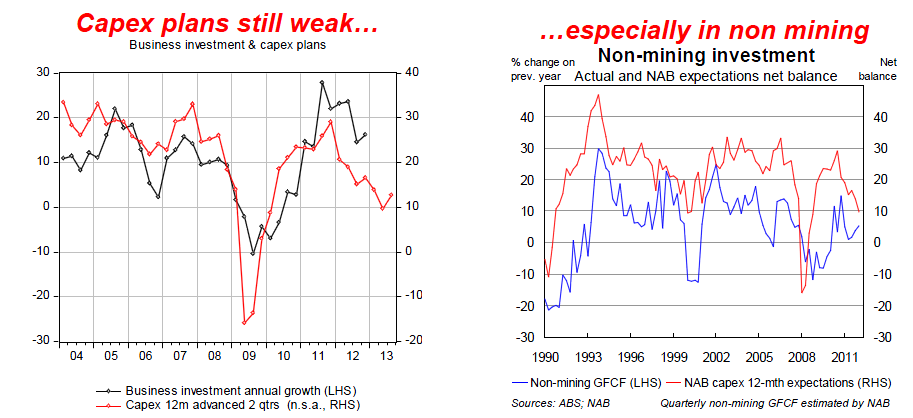

The quarterly version of the NAB Business Survey out today is most useful for one fact: it contains a capex intentions component not available in the monthly version. In the March quarter it showed the following:

The NAB survey measure of business capital expenditure continues to point to a further deterioration in business investment growth in the next six to 12 months, with the March quarter outcome implying little to no expected business investment. Nonetheless, expectations in the March quarter improved a touch from expectations in the previous quarter. The expected softening in investment growth is consistent with declines in commodity prices, which have brought into question the viability of a number of prospective mining projects (with mining investment making up the lion’s share of total business investment in Australia over recent years). A number of mining firms have confirmed their intentions to either scale back capacity or defer projects in the current soft price environment. While the approaching of the peak in mining investment is expected to see total business investment activity soften over the next year, the value of mining investment is expected to remain at historically elevated levels. There are, however, no signs of accelerating-non mining investment which would be needed to offset the falls in mining investment that lay ahead.

The rest of it is pretty academic. Either non-mining capex accelerates, or the public sector does the same, or we start losing jobs. There has been a turn in non-mining capex expectations but not enough to offset declines in mining.

Advertisement

The full assessment of the results was pretty dour:

Business confidence improved significantly in the March quarter – the first quarterly rise in sentiment since December 2011. That said confidence still remains below long-run average levels. Much of the improvement in confidence reflects the unwinding of concern surrounding a number of external risks, including the US fiscal cliff, a hard landing in China and the reduced risk of a further European crisis. While equity price rises and lower borrowing rates are also likely to have helped, it appears the still high AUD remains concerning for the trade dependent industries.

Business conditions strengthened modestly in the March quarter, after weakening to their lowest level since June quarter 2009 in the previous survey. That said, business conditions are still clearly signaling below trend growth. Indeed, the NAB quarterly business survey points to domestic demand growth in March quarter 2013 of around 2¼%. More worrying forward indicators of demand remain subdued – notably forward orders, stocks and capital expenditure – suggesting activity will soften into the June quarter. There are indeed signs of that happening in the March Monthly Business Survey.

The improvement in business conditions is almost entirely attributable to two industries; finance/ business/ property, which probably gained from rising equity prices and easier financial conditions, while lower borrowing rates appear to have helped to strengthen construction activity. Consumer and trade dependent sector conditions remained weak, implying that either lower interest rates need more time, or more stimulus (eg. RBA rate cuts) are needed to strengthen consumer demand. Conditions were little changed across mainland states in Q1, with the exception of Queensland, where they lifted considerably.

Business investment intentions (next 12 months) lifted a touch in Q1 but remained low relative to outcomes a year or two ago. Indeed, they imply flat investment growth over the next 12 months. This is consistent with NAB’s expectation for non-mining investment to take time to fill the approaching ‘gap’ from a slowing in mining investment. Near and longer term employment expectations ticked up but point to more labour market weakness. Lack of demand is expected to be the most significant factor impacting profitability over the next 12 months and concerns about tax & government policy remain important.

Product price inflation remained subdued, recording annualised growth of just 0.2%. Retail price inflation was also soft and implies a soft March quarter underlying inflation outcome. Labour and purchase costs growth remained modestly below-average levels.

There are some green shoots in the survey with confidence, property and finance on the rise but whether this translates into enough activity later in the year remains the question.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.