Cross-posted from FTAlphaville.

The reactions to Chinese macro data tend to go something like this…

Beat: Bulls are okay with this. Bears say it’s unsustainable, usually because of inflationary risks, policy tightening risks, credit risks, or the imbalances. FT AV commenters say the numbers are made up anyway.

Miss: Bears are okay with. Bulls say not to worry as it means more stimulus/loosening will happen. FT AV commenters say the numbers are made up anyway.

We’re wondering though if this will change with yesterday’s relatively wide miss with Q1 GDP growth, and much of the other data out yesterday looking soft.

Here’s Bloomberg outlining how this changes everything:

A sustained shift to a lower-growth gear would affect everything from iron-ore demand in Australia to the fortunes of companies including carmaker General Motors Co. (GM), who are counting on China to drive profits. It increases challenges for global policy makers contending with Europe’s debt turmoil and Japan’s record monetary easing, with BHP Billiton Ltd. (BHP) saying GDP gains will moderate toward 6 percent later this decade.

Nomura cut their 2013 growth forecast from 7.7 per cent to just 7.5 per cent, well below consensus (which was about 8.1 per cent prior to yesterday). Yesterday’s number kind of ruined Zhiwei Zhang and colleagues’ forecast for the trajectory of Chinese growth this year, which was also out of consensus; while others were seeing a gradual return towards 8 per cent growth, Nomura were anticipating a surge in Q1 that would be quickly reined in during the second half as inflationary pressures took hold.

We revise down our 2013 GDP growth forecast to 7.5% from 7.7% and our CPI inflation forecast to 3.1% from 3.5% (Figure 5). We no longer expect rate hikes in 2013, but maintain our view that credit growth will slow. Xinhua, the official news agency, reports that Premier Li Keqiang presided over a symposium yesterday with representatives from the industrial sector and thinktanks in attendance. He highlighted the importance of striking a balance between short- and long-term economic objectives, which suggests to us that he may be willing to tolerate slower growth now to achieve more balanced, sustainable growth in the future.

At the other end of the scale, RBS cut right back on their 8.4 per cent growth forecast (and well, even the World Bank wasn’t betting on that anymore!), reducing it to 7.8 per cent.

Okay for some, the narrative has changed little. HSBC’s Qu Hongbin has tended in the past to see disappointing data as an opportunity to look forward to stimulatory measures, and he’s done a similar thing this time. Although, we note that the balance of inflationary risks is being taken a little more to heart:

Bottom line: Today’s 1QGDP number is disappointing. As inflation is easing, this should prompt stronger policy response mainly in the format of more fiscal spending in the coming months, especially as all the dust of power hand-over is now settled. Once fiscal spending is delivered, growth should be lifted in the coming quarters. But the magnitude of the growth acceleration will depend on the dose of policy response.

But… even more interesting is Jing Ulrich of JP Morgan (emphasis ours):

A sharp decline in investment efficiency appears to be the most ready explanation for recent sub-par economic expansion, despite the remarkable credit boom. We think the questionable quality of China’s recent credit-fueled growth is reflected in the worsening incremental capital output ratio for the nation, as well as a downtrend in the return on capital for listed companies. This has been a key factor behind the underperformance of Chinese equities. Investors are also concerned about a potential negative wealth effect if the government succeeds in engineering a decline in housing prices through its stricter implementation of administrative controls. Finally, the recent discovery of a new strain of bird flu, H7N9, has provided further reason for caution – although the number of cases has been limited thus far, with no evidence of human-to-human transmission.

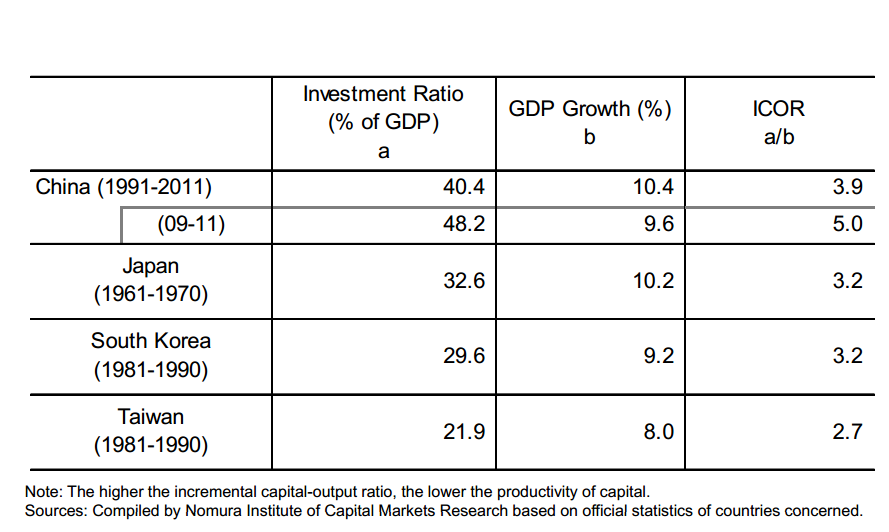

The Capital Output Ratio is a very interesting way of looking at China’s over-investment problem. Of course China’s massive investment is only a problem if it’s ‘malinvestment’. But this great chart from Nomura’s Capital Research Institute suggests that it’s already happening:

Yesterday’s GDP was a big shock to many, but time will tell whether this is a permanent change in how China’s growth is viewed. We’ll leave the last word to the FT’s Beijing bureau chief Jamil Anderlini:

Chinese officials have played down the significance of lower growth in recent weeks, saying the slowdown is partly due to efforts to rebalance the economy away from investment and exports towards domestic consumption.

Rebalancing, slower growth… it’s all sounding like both China’s leaders and the pundits that attempt to divine their true intentions might be nearing a kind of ‘Pettis Moment’, where it becomes widely accepted that China’s reducing its extremely high dependence on investment will inevitably mean the economy slows.

It’s a question Michael Pettis himself kind of asked in January (though a little more modestly than it sounds).

If this transition to a more consumption-heavy, slower growth model can happenwithout any significant disasters, well the bulls will stand corrected; just not in the high-single-digits way that some of them were hoping for.