A large schism is opening up in the economic forecaster space between those that see the approaching mining investment cliff as precipitous and those that view it as a gentlemanly stroll down a verdant slope.

The ANZ’s widely regarded major projects report is the most bearish, seeing the peak later this year and then tailing off at a rate of $30 billion per year for the next three years:

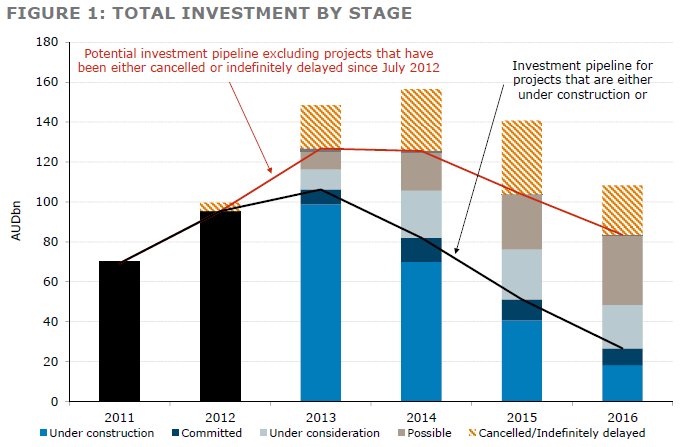

The ANZ is basically forecasting mining investment will return to its long run average of 2% of GDP by 2016. The NAB is in the same camp, seeing a similar collapse though not so bad into 2015. Unless more projects are canned, the blue line is the confirmed path that we are on:

CBA is also bearish, seeing a less clearly but equally unsettling decline (this one is not easy to follow because it is indexed to a 2007 baseline but it roughly matches NAB’s forecast. Again, the blue mountain is operative):

CBA reckons that the GDP gap can be offset by rising net exports but is concerned that falling activity will cause unemployment to rise significantly.

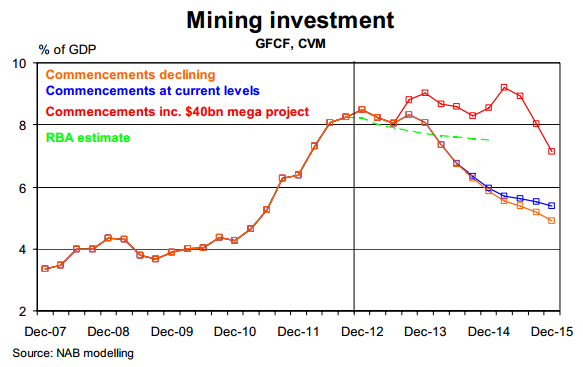

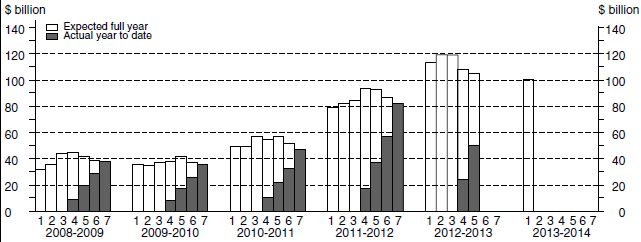

These forecasts can be compared with the genteel outcome pushed by the RBA. As you can see in the NAB chart above, the RBA (green line) sees a slow decline but has not gone more than eighteen months out. This is based in the main on the ABS expected capex expenditure survey which will have to fall sharply from its first forecast result for 2013/14 to hit the more bearish targets of the banks:

BREE has not released a major projects report since October so is behind the curve. It’s new report must due any minute.

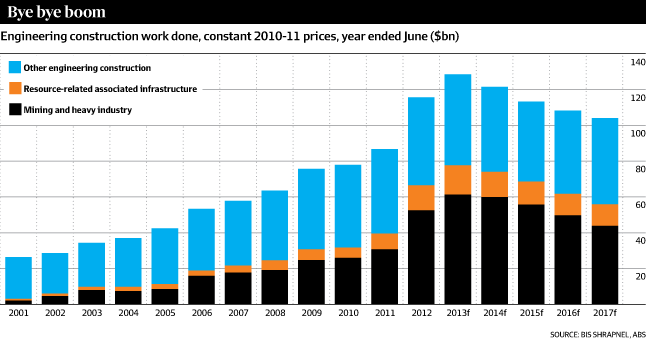

Delliote Access Economics’s major projects reports agrees largely with the RBA and so too does a new report out today by BIS Schrapnel:

BIS is using a broader definition than mining investment so its peak is higher and the tailing off is quite pleasant as you can see.

Whoever get’s this right is essentially forecasting where interest rates, the dollar and all sorts of asset classes will be next year so it’s no small question to ask, who do we believe?

My view is that the ABS capex survey is not terribly reliable, as the RBA itself has argued, so anything based upon it should be discounted on the downside to a degree. As well, I expect the terms of trade to continue to fall through the next two years so it is reasonable to expect as well that more projects will get shelved and future plans for mines will disappoint consensus wherever it is. Finally, the ANZ report is the most well researched and regarded of the major banks’ project reports.

Thus I am inclined towards a less favourable cliff.