Cross-posted from FTAlphaville.

These sorts of charts have been bothering a lot of people lately, including us:

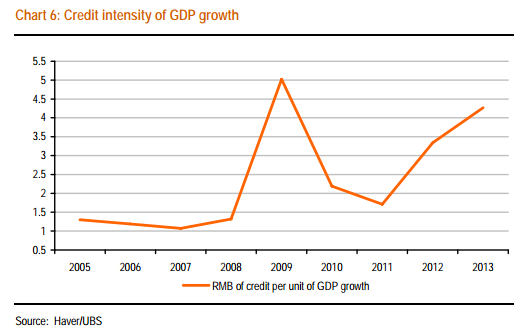

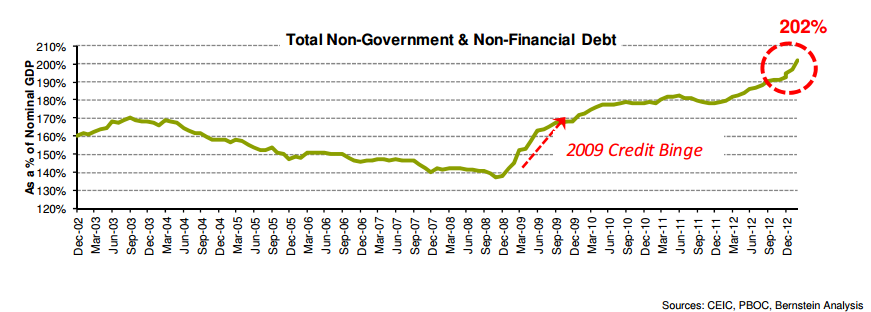

This one, via UBS’ George Magnus, shows China’s debt back near a 2009, stimulus-era ratio. Only, this time, it’s without the stimulus-era boost to the economy. We have more charts here and here illustrating this relationship, but here’s another example:

Why does this matter? The Reinhart-Rogoff debate in the past week or so relates to public debt, but you could argue, without being completely flippant, that in China, everything is public… so if we argue over whether particular sovereign debt-GDP ratios have key thresholds, why not with China?

It’s a good question, but some of it can be answered by saying that China is different – in its growth rates, its sources of growth, and its size relative to the world.

However, we’ll start with the recent confluence of faster credit growth and slower GDP growth that is worrying many China watchers. Magnus provides a good overview of these recent developments in a new note (read it in the usual place). He also touches on the big questions about what this all means:

In the face of the sharp slowdown in growth in early 2012, the government decided to play safe, especially ahead of the leadership change in October, and allowed credit to reaccelerate. But if it hoped the investment side of the economy would spring to life, the outcome has been disappointing, at least so far. Instead – and it’s hard to be specific – credit expansion is taking on a more Minsky-ish character: refinancing of maturing bad debt, borrowing to service debt because of weak cash flows and negative commercial returns, and the financing of ‘investment’positions in real estate and commodities. It is estimated, for example, that banks rolled over some RMB 3 trillion, or three quarters, of loans to local governments that matured in 2012.1 And the IMF has noted that in the broadly defined corporate sector, company profits are failing to keep up with rising interest rate expense, obliging firms to seek recourse to borrowed funds.2

As Magnus says, it IS hard to be specific about the nature of all this credit expansion, though there are certainly signs of the ‘Minsky-ish’ character — more debt being used to cover maturing bad debt and weak returns. Why is the ‘credit multiplier’ apparently slowing? One of our readers, Tom_ wrote on my post about China’s credit-fuelled non-recovery; essentially he was questioning why we assume that credit growth would have a constant multiplier. Once a country has a high rate of credit growth, that is part of your GDP growth. If the rate of credit growth slows, your GDP slows as a direct function; they are flows. Tom_ also points out that pondering the GDP-debt ratio makes the assumption that credit equals investment.

Without wanting to get into questions about accounting identities and the sectoral balance approach, we can establish two or three things about China’s growth and its credit:

1. For whatever reason, credit growth isn’t correlating to economic growth as much as it recently did.

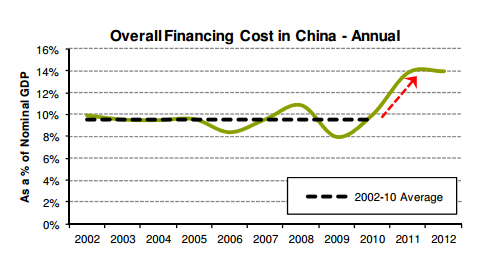

2. An increasing amount of the total GDP is being directed back into financing costs. Michael Werner of Bernstein, who made some of the interesting charts comparing credit growth and GDP growth rates, says it’s difficult to predict where exactly the growing debt levels may lead, there is a fairly simple mathematical truth (we’re paraphrasing him here) contained in this chart:

Rising financing costs, now at 14 per cent of GDP, underline Magnus’ point that credit is becoming less productive because it’s increasingly being directed towards financing itself.

That brings us to the third point about why the debt-to-GDP ratio is important — it’s a point specific to China. China’s investment has of course been largely credit-fuelled, and that investment has achieved a massive outsize role in its economy. It’s also been a significant contributor to China’s rapid growth rates post-2008.

So, credit needs to be directed to (good) investment to create growth.

Yet both credit and investment are unsustainably high...

This could end a number of ways, but it doesn’t seem that sustained high single-digit GDP growth levels is one of them.

Magnus, again:

Something is going to have to give. The credit boom could presage a pick up in near-term growth, but the point is that sooner or later, the government is going to have tighten credit policy and shadow banking regulation more than it has done so far. Sooner would risk some economic growth, later would risk financial stability. It’s a political choice, which the government must feel emboldened and confident to make: five years of 5% real growth, for example, gets you to the same place as a year of around 8%, followed by four years at 4%, but without disruptive and politically sensitive consequences.

In otherwords, China’s rising levels of credit growth, and slowing GDP growth, don’t necessarily foreshadow a crisis. But they do provide another signal that the economy’s growth level will decelerate, one way or another, and more quickly than many are expecting. This time, growth opportunities through past mechanisms of cheap labour, exports, and investment are all increasingly tapped out.