At least that’s the verdict of Credit Suisse with the half year result today:

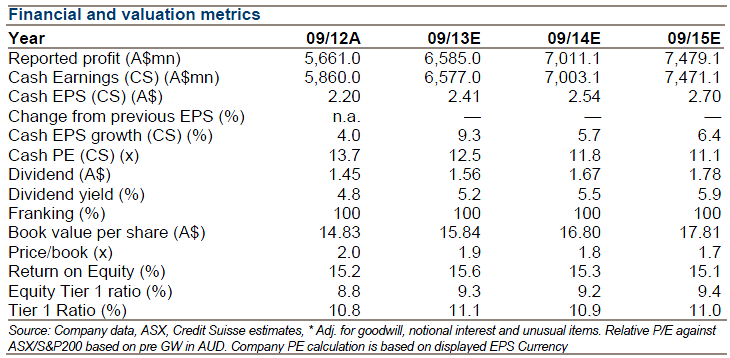

Event: ANZ reported (company defined) cash earnings of $3,182mn (up 10% on $2,896mn 1H12) 2% short of our top of market $3,253mn estimate but 1% better than the $3,135mn consensus average. Interim DPS of $0.73 (up 11% on the $0.66 pcp) was $0.01 better than our top of market estimate and much better than the $0.69 consensus, on a revised dividend policy. Refer detailed financials attached. Compositionally revenues were marginally weaker than expected; the consensus beat reflects favourable outcomes in bad debts especially (27bp) and costs.

Investment Case: Result should be well received, with an upwardly revised dividend policy, a strong cost outcome, net interest margins remaining intact (the key consensus fear going into the result) and the share rating quite discounted compared to peers. What we liked about the result: Revised dividend policy (65-70% cash payout, with a bias towards the upper end in the near term) from c65% previously; Costs down 8% sequentially (broadly based across divisions) with FTEs -2%; Creditable margin outcome (flat sequentially ex-Markets) with Australia division (+3bp) offsetting International & Institutional (-14bp) and NZ (-10bp) – although the headline margin was -4bp; Improving asset quality. What we didn’t like: Flat sequential revenues (weak funds management & insurance); On-going decline in collective provision coverage.

Valuation: ANZ currently trades on 12.0x 12-month prospective earnings (9% discount to the major bank peer group vs. a 4% four-year average discount) and a corresponding book multiple of 2.0x.

Fair enough. I’m currently giving some thought to whether an when one should short the major banks. As we go over the mining investment cliff, the terms of trade falls further and greater fiscal cuts loom, the time is approaching.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.