The always interesting Gerard Minack of Morgan Stanley has new note out this morning which underlines the challenge facing equities going forward.

Equities are being driven by a return to normal.

This is not a case of upgrading the base case, this is about reducing tail risk. And this is not a case of following the typical QE (quantitative easing) playbook.

My only concern is that I do not think the world is returning to normal.

The 25% rally in global equities from last June seems to be driven by a growing conviction that the worst is over and tail risks are fading. This, so far, is not about pricing in a notably stronger economic or earnings outlook.

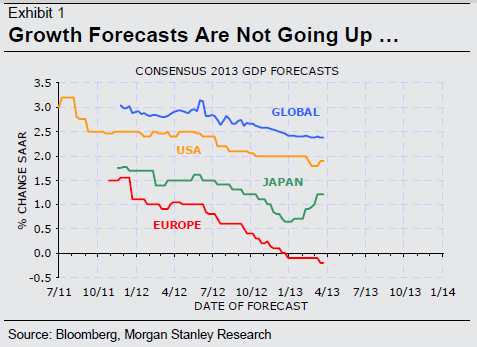

Consensus economic forecasts for growth have continued to drift lower, Japan excepted (Exhibit 1).

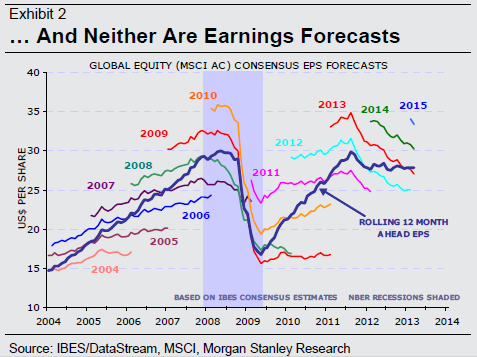

Likewise, consensus earnings expectations continue to fall. The rolling 12 month-ahead forecast for global EPS has flat-lined, and is no higher now than three years ago (Exhibit 2).

(The rolling 12 month-ahead forecast puts greater weight on the out-year calendar forecast each successive month, which is why it’s been flat even as the individual year forecasts have fallen.) With tail risks appearing to fade, expected volatility has fallen (FX markets excepted). The US VIX index last week fell to the lowest level since 2007.

Markets have not followed the template typically associated with QE episodes. I’ve argued that QE has been over-rated by investors as an influence on markets, but those who differed often argued that ‘money printing’ pushed up, for example, commodity prices and high-beta equity markets, as well as weakening the dollar. None of this has happened.

Notably, commodity prices have been mixed, at best. Industrial metal prices (LME index) are around the same levels as last May. The CRB index rallied from June to September 2012, but has fallen since. The GSCI is unchanged from last August. Mining stocks have performed poorly; relative to global equities, they are within sight of their 2008 lows. EM equity markets have under-performed. None of this fits with the presumed QE playbook.

I don’t entirely agree. Reduction of tail risks is still the direct result of central bank easing. The latest rally was fired off by Mario Draghi joining the global group of central bank avengers. And if markets have now shifted out of patterns associated with earlier episodes of QE, that’s because more folks are doing it, not less, balancing the equation as it were. Nonetheless, food for thought.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.