Strong currencies are the bane of every triple-A rated, QE-less economy in currency war-torn 2013, it seems. It’s become an increasingly irksome point in Australia, where the initial exuberance over cheap foreign holidays has been slowly replaced by worries that it’s squeezing the non-mining sectors.

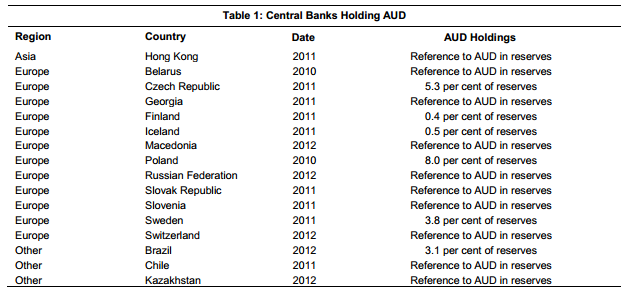

An FOI request by Bloomberg yielded a bunch of documents from the Reserve Bank of Australia about the currency’s overvaluation problem. Specifically, how bad it is and who’s to blame. Well, who among other central banks*, at least. Here’s list of the definitely-implicated:

Advertisement

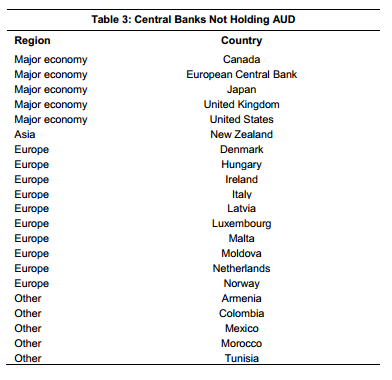

And a list of possible other culprits, courtesy of the RBA’s own sleuthing (and media cuttings):

Advertisement

The Fed, BoJ, ECB, BoE and Bank of Canada are among those definitely not holding AUD in their foreign currency mix.

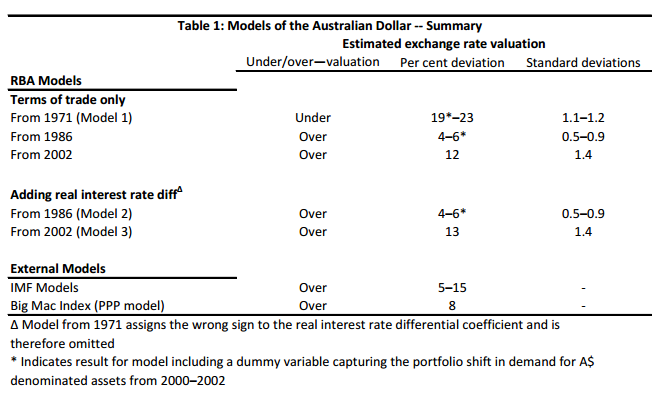

The RBA documents also include various internal emails and briefings about the AUD overvaluation. For example, a nice summary of various methods of estimating just how high the AUD is:

Advertisement

There’s a definite theme of reluctance to overplay the scale of the overvaluation. For example, from an internal briefing prepared for the September board meeting (our emphasis):

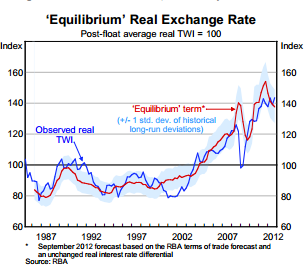

The staff’s preferred model is based on the long-run relationship between the real exchange rate and the terms of trade and the real policy rate differential with the G3 (US, euro area and Japan) over the post-float period. It suggests the exchange rate is around 5 per cent overvalued. However, given the uncertainty of the estimates, the model also suggests that the exchange rate could be reasonably assessed (at roughly a 70 per cent probability) as being anywhere between 4 per cent undervalued and 12 per cent overvalued (shown by the shaded band on the graph).

Advertisement

Well, central bankers are supposed to be level-headed after all; and it’s not like RBA officials haven’t been clearly stating in recent months that they don’t like the AUD valuations. While the bank has signalled that the dollar has been a factor in deciding recent rate cuts, and there’s been a bit of ‘passive intervention‘ with a chunk of foreign currency, so far it does not seem to have done much.

We have to wonder how much of the central bank’s low-key response to the AUD’s overvaluation is because officials genuinely think the Australian economy can cope, and how much of it is because doing anything about it is too damn difficult. The RBA is already in a cutting cycle but slashing rates very low would risk inflation. Going Swiss is not an attractive option for small economies that have inflationary pressures; as the New Zealand central bank governor outlined last week.

An RBA assistant governor further elaborated this week, by explaining that the scale of Switzerland’s balance sheet, if applied proportionately to Australia, would total $1tn. Not a portfolio to be embarked upon lightly.

Advertisement

Of course, the RBA’s reluctance to really wade in is likely a trade-off between the size of the problem and the difficulties of doing anything: the costs don’t seem to warrant the risks of taking dramatic action. So far. With Australia’s economy likely to hit a very significant point this year as mining investment peaks, the harm that could be wielded by a persistently strong AUD — one that’s largely disconnected from commodity prices — might become much clearer.

In that scenario, how long might it take before even a ‘moderately’ overvalued currency takes its toll? We also can’t help noting that the central bank of New Zealand, a much smaller economy in a very similar predicament, has decided that despite the risks it is time to go a little harder by explicitly threatening intervention and unspecified ‘macroprudential’ tactics to relieve the upward pressure on its currency. There’s some room for creativity, after all.

But perhaps we’re being too doomy. RBA governor Glenn Stevens says that if things get really bad, a strong Australian dollar probably would cease being a problem. From a regular parliamentary testimony last week:

Advertisement

On what the tools would be if you think it is a major overvaluation, I think, in all honesty, the evidence of history is that, if it is overvalued by a long way, it is going to come down sooner or later and the market will bring it down. I should add that, if that is the case and that starts to happen, my expectation would be that public debate will very quickly swing from fretting about the higher dollar to fretting about a falling one. The other tool that may be available is, of course, intervention. I think the truth is that, with the power of the forces at work here, you would need to be pretty confident that it is seriously overvalued or that the market is behaving in some quite irrational way before you would launch on large-scale intervention, and we have not done that in this episode.

It seems markets would need to be behaving *really* irrationally to warrant intervention:

I would have to say that, as uncomfortable as it is at the moment, in the broad sweep of history, markets are irrational much of the time, but somehow, over the broad sweep of history, I think they have done a better job setting that price than we would have done if we had been trying to set it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.