The excellent ACCI quarterly Westpac survey is out today and shows a significant manufacturing conditions in the March quarter:

-

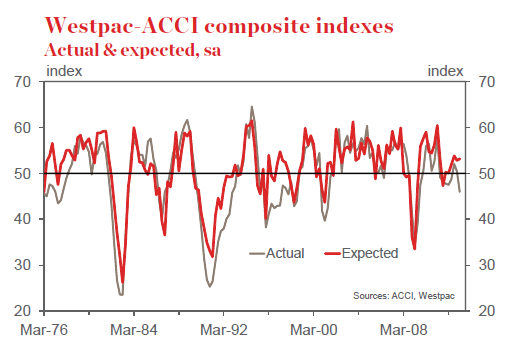

The Westpac–ACCI Actual Composite fell from 50.4 in the December quarter to 46.0 in the March quarter. A reading below 50 signals contraction in the manufacturing sector. This is the weakest outcome since June 2009’s 39.1.

-

The Expected Composite edged higher in the March quarter, from 52.8 to 53.2; respondents continue to expect conditions to improve in coming months, despite the weak Actual Composite reading.

-

Expectations of general business conditions also improved in the March quarter; a net 8% of respondents expect the business environment to improve over the next six months, up from –1% in December.

-

The Labour Market Composite fell to a level consistent with weak annualised employment growth of around 1% over the coming six months. Actual employment and overtime both deteriorated. Overtime is expected to increase next quarter, but employment is expected to fall.

-

Consistent with the fall in the Labour Market Composite was a marked improvement in the availability of labour. This followed a modest tightening over the previous three surveys. The wage expectations of manufacturers have also softened over the past three months.

-

Manufacturers continue to lose pricing power. As with previous surveys, actual selling prices have been well below expectations. Contrary to expectations, only 5% of all respondents were able to increase prices, while 79% were forced to keep them unchanged. In contrast, 27% of respondents reported increased costs, explaining the ongoing disappointing profit performance.

-

Manufacturers’ profit expectations improved in the quarter, potentially as a result of the recent moderation in wage growth expectations. That said, profit expectations remain well below average levels.

-

Investment intentions in the manufacturing sector remain weak. Plant & equipment and building intentions were both scaled back again during the past three months. The December quarter CAPEX survey concurs with this result, signalling that a marked decline in investment in the manufacturing sector is underway.

-

The Australian manufacturing sector remains under considerable pressure despite the substantial rate cuts delivered to date. Those manufacturers who are exposed to residential construction have benefited. That said, the sector remains weak. As the mining investment boom draws to a close, further monetary accommodation will likely prove necessary.

It’s a relief to know that the “marked decline in investment” observed by the survey actually means improving productivity even though that’s literally impossible.