Cross posted from FTAlpahaville

The Reserve Bank of Australia cut its cash rate on Tuesday to 3 per cent — making a total of 175bps worth of cuts since November 2011, and bringing the rate to its lowest level since the depths of the financial crisis.

The RBA’s governor’s statement alluded to the bank’s discomfort over the stubbornly high Australian dollar, which is not doing what it tended to do in the past and falling to provide a fillip to the economy:

There are signs of easier conditions starting to have some of the expected effects, though the exchange rate remains higher than might have been expected, given the observed decline in export prices and the weaker global outlook.

The strong and newly-resilient AUD is partly due to reserve diversification by foreign central banks and SWFs, along with Australian government bonds (ACGBs) remaining one of the few sovereign bonds still rated AAA.

However the foreign appetite for ACGBs is waning, just a little, as JP Morgan’s Australia economist Sally Auld points out (emphasis ours):

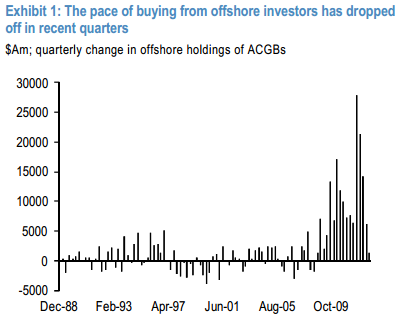

The current account data for the September quarter show that offshore investors were still net buyers of ACGBs in the three months to June. Offshore investors added $1.3bn of ACGBs to their portfolios.

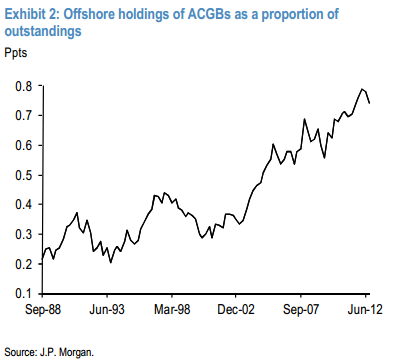

This was the lowest amount (in absolute terms) of offshore buying in net terms since the June quarter of 2008 (Exhibit 1) and continues the theme of less-intense inflows from offshore investors into the ACGB market. Offshore holdings of ACGBs as a percent of total outstanding is now at 74.4% (Exhibit 2). Nonetheless, foreigners still hold a significant proportion of ACGBs outstanding by historical standards.

Auld writes that while foreigners absorbed 88 per cent of net ACGB issuance in 2010 – 2011, they only absorbed 9 per cent of issuance in the September quarter.

She adds:

Perhaps the more interesting story for the ACGB market is the prospect of waning enthusiasm for ACGBs by foreign investors in an environment where domestic fiscal fundamentals appear to be deteriorating.

Perhaps, indeed! Go on…

While recent rhetoric from the Federal Government has still emphasized the Government’s commitment to achieving a surplus in the 2012/13 fiscal year (and beyond), J.P. Morgan economists are forecasting a deficit of $15.0bn in the current fiscal year. This is probably a conservative estimate given downside risks to the growth outlook and lower commodity prices.

Well yes. The Australian Treasury’s rather optimistic forecasts for commodity prices in its revenue forecasts were the basis for the somewhat muddled solution to taxing the mining industry that was arrived at, following a Prime Ministerial coup in 2010. However we’re not convinced that investors — particularly the buy-and-hold types that have been so keen on ACGBs of late — would see much difference between a small deficit and a tiny surplus.

The bigger risk is that the commodity-intensive and China-exposed nature of the Australian economy begins to make those foreign investors wonder whether the country’s sovereign debt is such a good thing after all.

Whether any of this happens — or happens in time to weaken the dollar and aid Australia’s economy as the peak of the mining investment boom draws near — is anyone’s guess.