Cross-posted from FTAlphaville.

When the International Energy Agency’s big annual report came out last week there was a big top line story picked up nearly everywhere: that US oil production will overtake Saudi Arabia by about 2020.

This is due to projected rises in oil being wrung from the sort of shale formations that have been the source of vast new supplies of natural gas in the past few years.

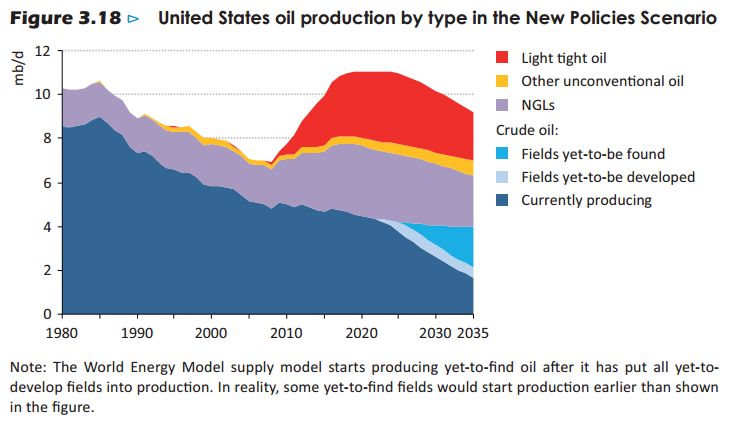

Here are the IEA’s actual US oil production forecasts, in a “New Policies” scenario (click to enlarge):

The ‘New Policies’ scenario includes no new greenhouse gas emission policies beyond what was committed to by mid-2012; average 3.5 per cent world GDP growth to 2035; and average crude oil prices approaching $125/barrel, in 2012 dollars, by 2035.

However, Neil Beveridge and colleagues at Bernstein Research have been sceptical about the predicted shale oil boom for some time, as highlighted in their note about the Bakken shale formation in Montana which we wrote about in August.

They remain unmoved by the IEA’s forecasts, foreseeing an earlier peak and a quicker decline of US oil output:

The renaissance in US liquids production has been remarkable, growing by over 1mmbls/d to reach 8.5mmbls/d this year over the past three years. By 2015 we expect that the US will produce close to 10.5mmbls/d given further growth in shale liquids. This will be comparable to Saudi production but only for a brief period and by 2020 we forecast that US production will have declined back to 9mmbls/d. In contrast, the IEA expect US liquids production to keep growing to 11.1mmbls/d by 2020 following which the US production will plateau and by 2025 start to decline (Exhibit 2).

Beveridge explains:

As we have noted, shale liquids plays are far rarer than their related shale gas plays and already we are seeing decline in some of the core areas of the Bakken oil field highlighting the early onset of maturity in some of these plays (see our report Bernstein Commodities & Power: Something is Rotten in the State of Montana).

And as for the rest of the non-Opec producing world:

Outside of the US, Canada and Brazil will be the largest contributors to non-OPEC supply growth. Again however there are risks. Delays to drilling rigs and FPSOs in Brazil as a result of local content regulations, infrastructure bottlenecks and scaling back of oil sands investments in Canada mean that production growth may not be as rapid as some expect. Excluding biofuels, we project non-OPEC supply will show no aggregate growth over the next 10 years and remain at 48.7mmbls/d compared with the IEA which projects a 2mmbbls/d increase to 50.2mmbls/d in 2020.

Long-term forecasting for energy supply and demand is notoriously difficult, like most other types of long-term forecasting. Unforeseen developments — like technology and prices rendering it economic to extract shale oil — can really throw a curve ball at those who make these forecasts for a living. US shale gas is a very good example. However, reading through the WEO section on oil supply and the somewhat breathless box on ‘light, tight oil’, it’s hard not to wonder if the IEA authors have overshot a little in relating this to shale oil (emphasis ours):

The US Energy Information Administration estimates that unproven recoverable resources of light tight oil at end-2009 stood at 33 billion barrels; adding about 2 billion barrels of proven reserves yields a figure for total remaining resources of 35 billion barrels. Some industry sources claim that recoverable resources will end up being much larger, capable of sustaining a higher level of production for longer than we project here.

Well, it would be weird if no industry sources were claiming that.

Meanwhile, The Oil Drum points out that just last week, Chesapeake’s chief executive Aubrey McClendon was expressing pessimism about the oil potential of the Utica shale formation in Ohio.