Stocks were lower and the Euro strengthened overnight in what was essentially lacklustre trade over the past 24 hours. How or why these moves occurred is really not worth worrying about as the past 24 hours has been about light volume range trading with little or no conviction.

But we did see yet more data points which are pointing to the weak reality and outlook for the global economy at the moment. Data from Japan yesterday showed that Q2 GDp expanded just 0.3% which was half the expected rate and the year on year number is now close to 1% not more than 2% as expected. Equally worrying was the news I picked up on Reuters which showed that China’s output of refined copper dropped 6.8% from the month before – but that was a record high so we have to add that context as its not all bad.

So Europe was a bit flat after the Japanese data and decided that with a lack of topside catalyst the bulls would make way for the bears – at the margin anyway. The FTSE was off 0.3%, the DAX fell 0.50% and the CAC was off 0.27. In Madrid the market actually managed to post a small gain of 0.27%. Italy sold some short term debt and they have a bond auction tonight as well as some Greek debt and of course the GDP data for Europe. It could be very interesting for Europe tonight so watch the data.

In the US stocks were similarly lower for the Dow dropping 0.29% while the S&P fell 0.14% to 1,404 while the NASDAQ managed a rise of 0.05%. Most of the focus in the US overnight seems to have been on Mitt Romney’s running mate Paul Ryan for the upcoming Presidential election.

On commodity markets news that the G20 is thinking of an emergency meeting about the price of grains reinforces to me that we might have seen the highs last week in this complex, given regulators and government track records of moving behind the curve. At the close of play corn was down 2.15%, wheat dropped 3.33% and Soybeans fell 2.69%. Copper was off more than 1% while crude was essentially flat. The wash up was that the CRB dropped a little less than 1% to 299.

In FX land the Euro rallied but it is only small bickies and ranges at the moment but the Aussie does look like it is slipping back from the highs of last week and under a little pressure. Even then though it is only a cent or so lower than the highs – as the lack of catalysts but more likely action keeps things subdued. NAB Biz survey might give us something today though. The pound was under a little pressure against the Euro and of course yesterday’s weak GDP data in Japan put the Yen under pressure. Well actually it didn’t – markets are very thin and lacklustre at the moment.

Lets have a look at some of the markets we follow using our AVATrade trading platform charts.

EUR/USD: Euro is gradually drifting lower but is realistically simply range bound and boring. 1.2250 is key short term support and then 1.2150/1.2110. Resistance at 1.2450/72, 1.2572 and 1.2740/50.

AUD/USD: The AUD is drifting and sits just above 1.05 this morning. 1.0450 is solid support from a week or so ago and then below this you can see the importance of the 1.0350 level of the chart below. Overall it remains strongly in an 8 week uptrend but likely to probe lower to find where real support is once again.

DATA: NAB Monthly Business survey and New Motor Vehicle sales are the keys for me in Australia today and then a raft of European CPI and GDP data data before advance retail sales in the US tonight. It might be a more volatile 24 hours than we think.

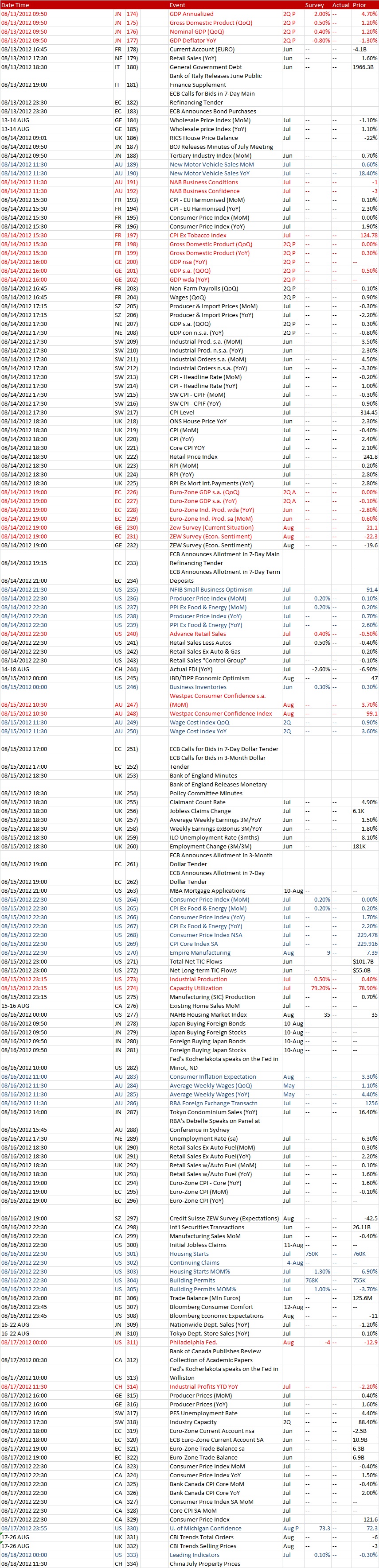

Here is today’s data and you can click here for the full week’s calendar. Please note that data coloured blue is important to me and that which is coloured red is important to everyone.

{kind=link}

And here is how the markets closed at 6.00 am Saturday Morning courtesy of AVATrade

Twitter: Greg McKenna. He is the Chief Investment Officer of Macro Investor, Australia’s independent investment newsletter covering trades, stocks, property and yield. Click for a free 21 day trial.

Disclaimer: The content on this blog should not be taken as investment advice. All site content, including advertisements, shall not be construed as a recommendation, no matter how much it seems to make sense, to buy or sell any security or financial instrument, or to participate in any particular trading or investment strategy. Any action that you take as a result of information, analysis, or advertisement on this site is ultimately your responsibility and you should consult your investment or financial adviser before making any investment decisions.