Courtesy of Sober Look.

In spite of the fear mongering taking place in the media and in the blogosphere with regard to the US housing “shadow inventory”, considerable progress is being made in shrinking the oversupply of distressed properties around the country.

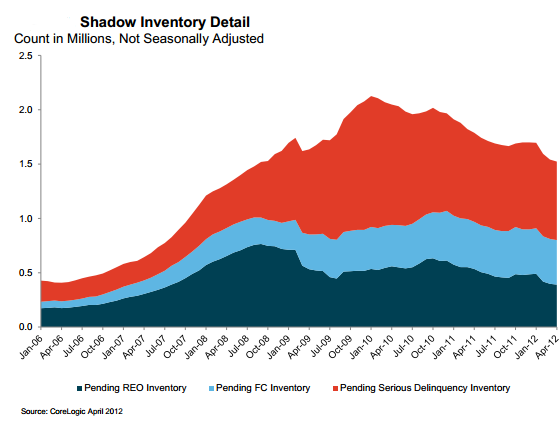

CoreLogic: –

- As of April 2012, shadow inventory fell to 1.5 million units, or four-month’ supply and represented just over half of the 2.8 million properties currently seriously delinquent, in foreclosure or REO.

- The four-month’ supply of shadow inventory is at its lowest level in nearly three years. It parallels the unsold months’ supply of non-distressed active listings that hit a more than five-year low in April, falling to a 6.5-months’ from a 9.1-months’ supply just a year ago.

- Of the 1.5 million properties currently in the shadow inventory, 720,000 units are seriously delinquent (two months’ supply), 410,000 are in some stage of foreclosure (1.1-months’ supply) and 390,000 are already in REO (1.1-months’ supply).

- The dollar volume of shadow inventory was $246 billion as of April 2012, down from $270 billion a year ago and a three-year low.

- Serious delinquencies, which are the main driver of the shadow inventory, declined the most in Arizona (-37.0 percent), California (-28.0 percent), Nevada (-27.4 percent), Michigan (-23.7 percent) and Minnesota (-18.1 percent).

|

| Source: CoreLogic |

It is important to note that the CoreLogic numbers exclude homes that are already listed in the market – it only shows the “shadow” (unlisted) inventory. That means that the overall inventory of distressed homes is far greater than the chart above shows (maybe 2 to 2.5 times that number).

Two key components are impacting the decline in shadow inventory:

1. A smaller portion of loan delinquencies now results in a sale due to the various loan restructuring programs and

2. the inventory has been hitting the market much faster than people anticipated.

The pie chart below is the projection from JPMorgan of how delinquent mortgages in the US will be resolved this year.

1. Not all of the “shadow inventory” is expected to hit the market.

JPMorgan: – … increased modification efforts and other foreclosure alternatives should remove a sizable amount of inventory … In addition to the ongoing HAMP and proprietary mod programs, which were pacing at around 500,000 loans annually at the end of 2011, increased incentives to HAMP forgiveness, relaxing DTI [debt-to-income] requirements, and requirements to forgive principal in the AG [Attorney General] settlement should boost modifications by hundreds of thousands more loans. In all, we expect over 1mn loans to be modified in 2012.

2. Short sales are becoming a larger part of liquidations, putting the inventory on the market much faster.

JPMorgan: – … servicers have been aggressively pursuing short sales as a lower severity alternative to foreclosure; short sales are nearly half of liquidations now.

3. REO bulk sale and rental programs will reduce the inventory further.

Overall some 2.5 million loans will be resolved this year. Note that a good percentage of these 2.5 million homes is already listed in the market and therefore is no longer included in the shadow inventory number. Nevertheless this year’s mortgage resolutions are expected to materially reduce the supply.

JPMorgan: – … All in, we think over 2.5mn loans could be resolved this year, putting a major dent in inventory. Of course, given the large supply and volume of continuing delinquencies, we expect it will take years to work through all the defaults, but significant progress is being made, which gives us reason to be more bullish on housing than we have been for years