Asia was in a bit of a funk yesterday afternoon after the Chinese trade data showed weaker exports and imports and crucially knocked notions of a broadening growth pattern in the world’s second biggest economy toward domestic consumption. This concern over the sluggishness of China gave way in European trade which was in an ebullient mood as the details of the Spanish deal spread through the market. The news that Spain would get more time to sort itself out and a release of funds saw Spanish yields rally fairly hard falling more than 25 basis points to 6.81% for the 10 year. This along with stronger data in the UK and Italy helped the EUR and European share markets push higher as well. The EUR’s strength was fleeting, however. European equities finished with the FTSE up 0.65%, DAX up 0.795 and the CAC up 0.59%.

But, as you can see in this 15 minute chart of the Dow Jones Industrials, it was a tale of two halves as the early rally which saw it up around 100 points at one stage before it not only reversed course but actually fell over 100 points before rallying into the last 15 minutes of trade.

But, as you can see in this 15 minute chart of the Dow Jones Industrials, it was a tale of two halves as the early rally which saw it up around 100 points at one stage before it not only reversed course but actually fell over 100 points before rallying into the last 15 minutes of trade. The turn around in the Dow and the S&P was driven by a combination of data and earnings plus more profit warnings indicating earnings are under pressure. The poor data was consumer confidence and a sharp drop in small business confidence. However it is the earnings warnings that are the key to the future as you don’t get warnings in the current environment en masse unless sales are off. This is crucially important in the context of how zero interest rates and quantitative easing have been holding the market up.

In effect zero interest rates increase the net present value of a series of cash flows towards infinity as the discount factor reduces. Obviously this is in abstract but you get the point. There are two sides to this net present value calculation – the discount factor and the cash flow. If the cashflow from earnings is falling then even with a ridiculously low risk free rate the value of the income stream through time will fall and thus so will equities.

This is a big risk to the market for risk assets not just equity markets and at the close of play the Dow was down 0.65% to 12,653, the S&P 500 down 0.81% to 1,341 and approaching important trendline support and the NASDAQ fell 1% to 2,902.

Equally concerning for markets and no doubt compounding the warnings on earnings and the Chinese slowdown are comments overnight from Italian Prime Minister Monti being too honest for everyone’s good. Reuters reports that he has suggested that Italy, the too big to save Club Med economy, may want to tap Eurozone aid:

“It would be hazardous to say that Italy would never use (this mechanism),” he said after a meeting of European finance ministers in Brussels. “Italy may be interested.”

While markets await the German Court decision on an injunction against the ESM and the fiscal pact this is most unhelpful.

All this combined to put downward pressure on commodities. The CRB Index reversed yesterday’s gain falling 4 points to 288.65 and in contrast to the previous night’s universal rises 14 of the 16 markets fell. Nymex crude was down 2.38% to $83.99 Bbl, Gold fell 1.34% and the agricultural commodities that have been having such a stellar run pulled back. Soybeans looks really ripe for a correction :).

In FX markets it was all about King Dollar, as we suggested in the trades section of Macro Investor this week, which no doubt is also putting downward pressure on the commodity prices discussed above. The EUR’s strength gave way quickly to fresh two year lows, Streling did better on that stronger data earlier in the day and EUR/GBP continues to look like a really good trade at present from the short side even if it is a bit extended. The Aussie had a similar reversal from early strength but for the moment is still holding in relatively well, given all the news that would normally knock it lower. Even the yen’s strength was stemmed by the stronger US dollar.

Just briefly in other news:

- The ECRI renewed their call that not only is the US headed for recession but is in recession.

- Somehow another money management firm in the futures space has gone down with client money again and is being investigated by the CFTC. The companies name is Peregrine Financial according to Dow Jones.

- You have probably seen by now that Barclays boss Jamie Diamond has forgone his £20 million bonus payment. imagine how much cash has to be stashed to do that!.

Lets have a look at some of the markets we follow.

Crude: I retain a bearish bias and think that crude is looking for a move back toward recent lows. $82.00 is the next level of support.

EUR/USD: I said yesterday that I think longer term EUR seems biased toward 1.18 but that I expected a bounce. We didn’t get it in Asia but it came in early European trade before reversing. This chart is of the weekly price action of the EUR for context of the potential selloff – it has much further to go.

AUD/USD: The trend following system is still long and will cut out if the AUD falls below 1.0122. The AUD is not going lower unless or until the trendline from the recent low below 0.96 breaks. The AUD bounced off this line on the dailies and 4 hourlies last night so clearly traders are watching it. Seems only a matter of time, though, and a move below this week’s lows around 1.0153 will see a very short term system of mine go short and the sell off likely accelerate.

S&P 500: Closing in on support – this is a bellwether for global markets and needs to hold.

DATA: NAB Business survey wasn’t terrible yesterday and we await the Westpac Consumer confidence today along with house finance data.

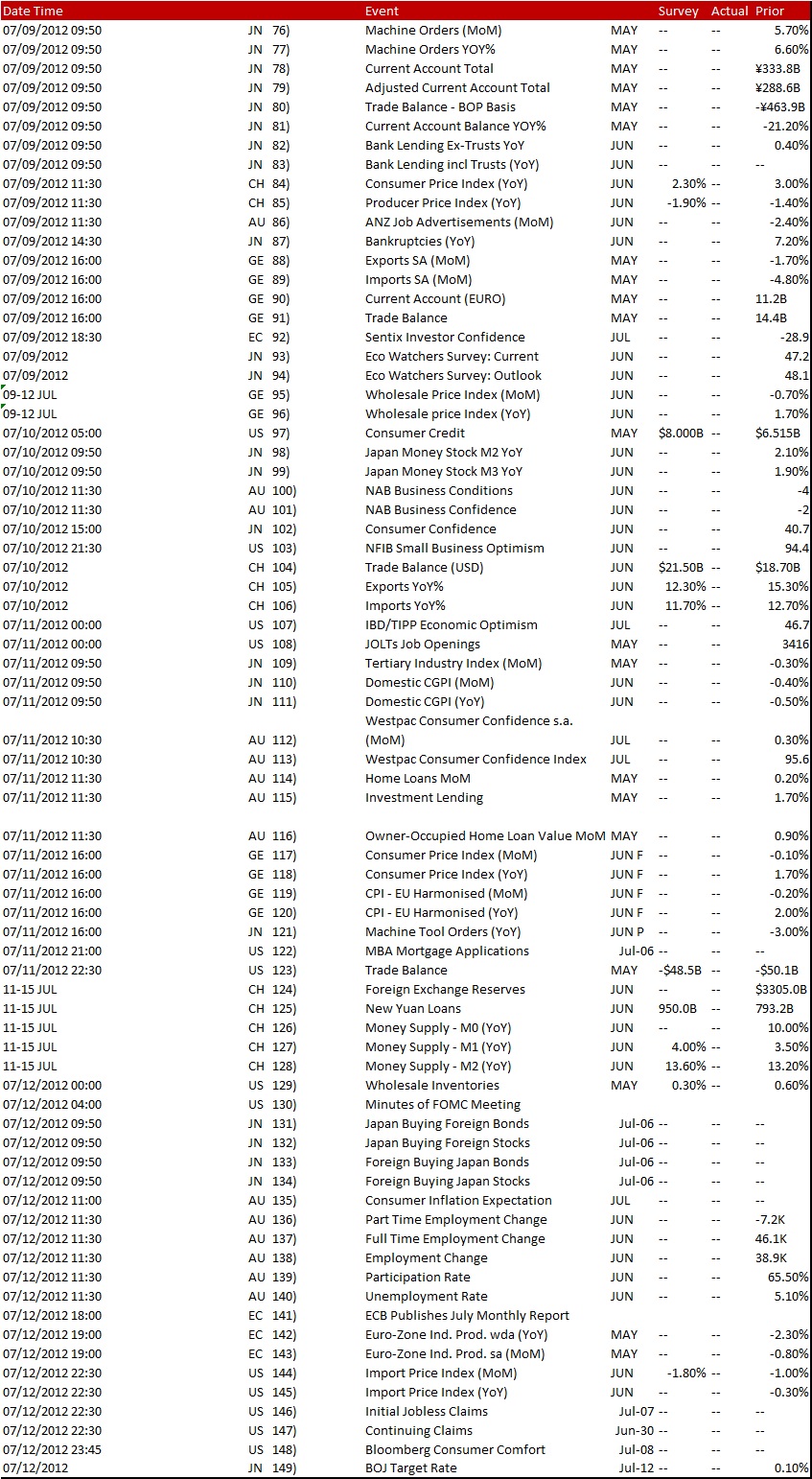

Here is today’s data and you can click here for the full week’s calendar.

{kind=link}

And here is how the markets closed at 6.00 am Saturday Morning courtesy of AVAFX

Twitter: Greg McKenna. He is the Chief Investment Officer of Macro Investor, Australia’s independent investment newsletter covering trades, stocks, property and yield. Click for a free 21 day trial.