Cross-posted with permission from MacroTragedy, a Greek-based macro-analyst who you can also follow on Twitter

It certainly is no secret that the west is de-industrializing fast and has been doing so for some time now. This trend has been present since the 1980s. Nonetheless, some countries, did manage to buck this trend and re-industrialized.

Now that the so called Greek growth model (if one is that charitable to call it that way) has crumbled with all the painful and disastrous consequences that we are living through, many voices have been calling for the Greek tradable sector to grow. Of course manufacturing accounts for a considerable part of the tradable sector. Hence, a good question is whether it is possible for Greece to re-industrialize?

|

| source: AMECO ,own calculations |

|

| source: AMECO ,own calculations |

As you can see from the chart, the two Euro-Area countries that re-industrialized contrary to the prevailing trend are Finland and Ireland. This trend was present from the early 90s till the early 00s since it stalled afterwards. The same, to a lesser degree though, can be claimed for Germany and Austria, although in Germany’s case the trend reached its high in the 00s.

The interesting thing is that the strategies that they followed in order to achieve that re-industrialization were quite different. Unfortunately historical data for Ireland don’t stretch back to the same time as for other countries but we’ll make do with what we have.

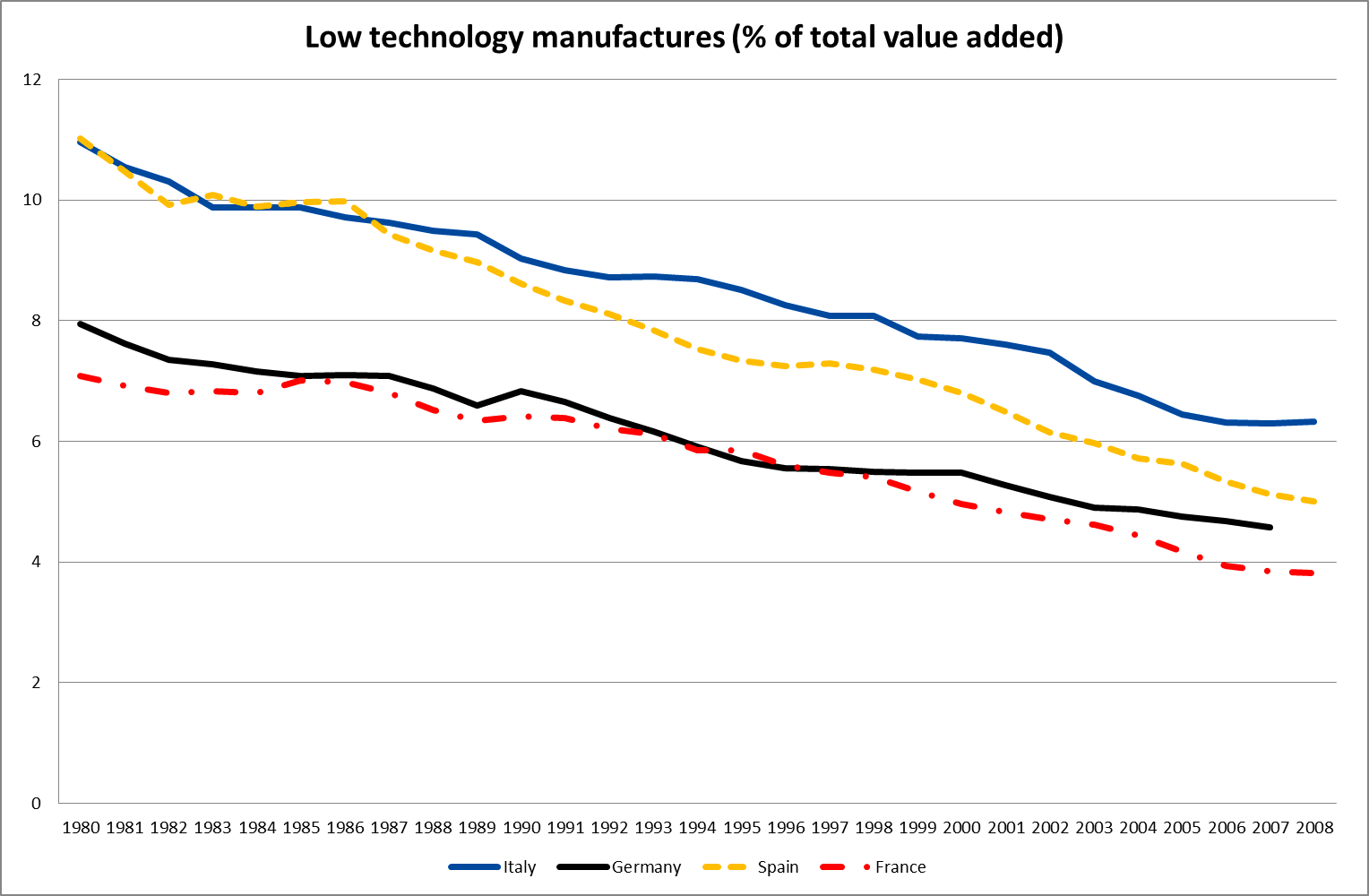

Another trend present in the manufacturing sectors of Euro-area countries is that in all cases low-technology manufacturing lead the de-industrialization process while high and medium-high technology segments proved to be more resilient. During the ’00s these segments too have started to subside in relative importance as well.

|

| source: OECD |

|

| source: OECD |

In all Euro-Area the low-tech sector is in free-fall with the only discrepancy being my native Greece where the sector livened up a bit during the 00s. Unfortunately OECD data run-up to 2008 so we cannot gauge whether this is just a blip or not but I will come back to that later on.

And here are the graphs for the medium-high and high-tech segments.

|

| source: OECD |

|

| source: OECD |

As the two last charts make obvious all cases of relative re-industrialization were driven by the medium-high and high-tech segments. But then which are the differences between Ireland and Finland that I talked about earlier?

The difference lies in whether the firms that powered this re-industrialization process were indigenous or not. In Finland the firms that were the driving force behind the ICT (information communications technology) boom were indigenous, while in Ireland the re-industrialization process was based on multinational corporations setting up shop in Ireland (Foreign Direct Investment – FDI). The next chart is telling.

|

| source: UNCTAD |

In both cases the boom started in 1991-1992. Well, as you can see, inward FDI in Finland was virtually non-existent at the time while it was considerable in Ireland’s case. If you look at the chart about manufacturing value added share you may see that the de-industrialization process in Ireland gained steam again at the same time that the inward FDI stock plummeted. I guess that this could be taken as a sign that manufacturing activity in Ireland is to a large degree driven by multinational corporations.

Of course, since in both cases the booming sectors were in the medium-high and high tech segment the relative technology had either to be developed or to be “imported” somehow. Even in the case that the relevant technology was “imported” if the technology differential between the indigenous firms and the multinational firms is too high then the benefits for the host economy through backward linkages will be limited.

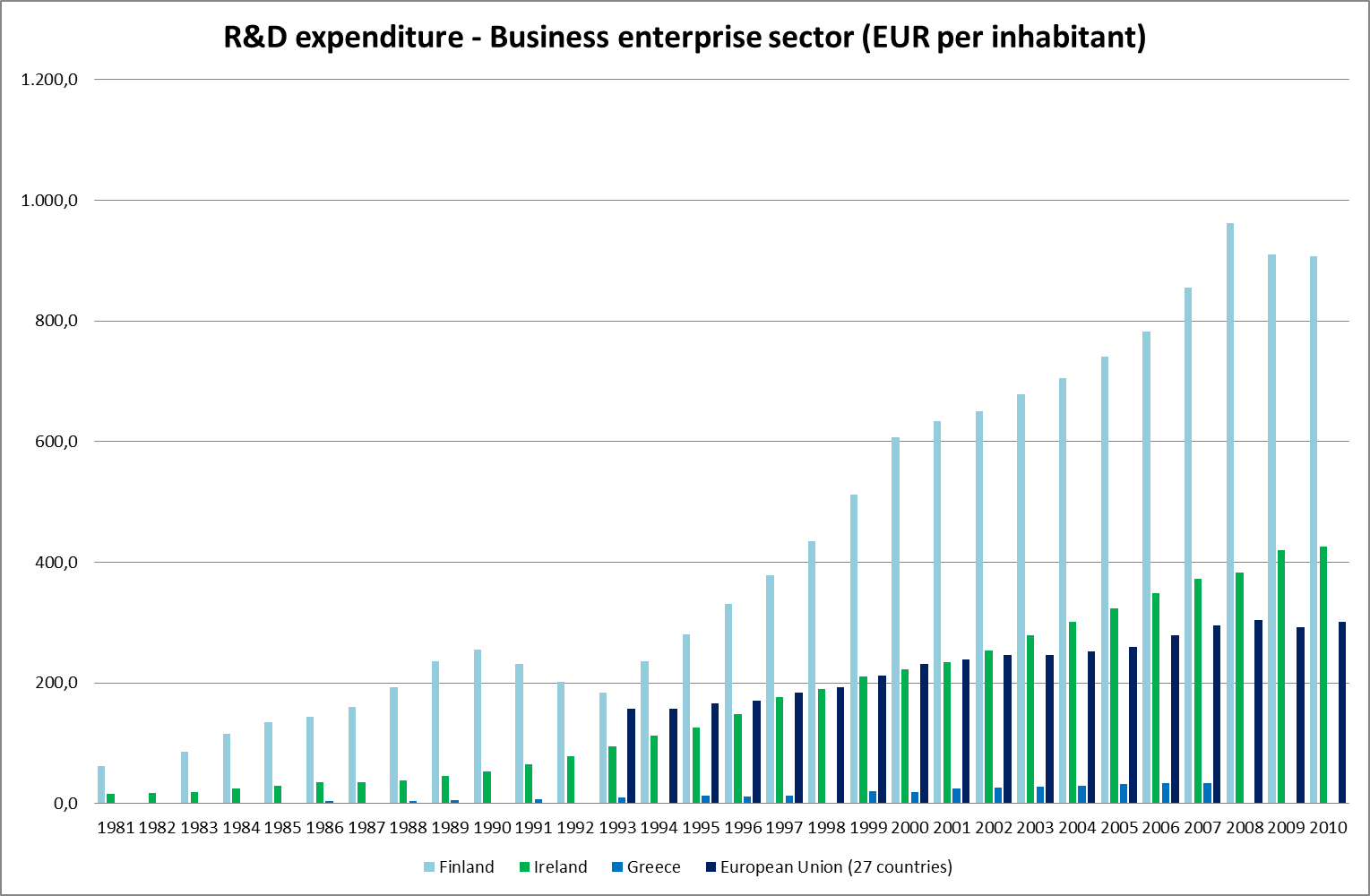

Since in the Finnish case the boom was based on indigenous firms, to some extent the technology was developed inside the country. Much credit has to be given to all actors in the Finnish business stage for their foresight. For years prior to the boom Finland invested heavily in R&D and what’s more the government sector, the universities and business sector co-operated closely. That gave them the ability to seize the opportunity when the ICT boom occurred.

|

| source: Eurostat |

Overall R&D expenditure for Finland is more than double the EU27 average.

|

| source: Eurostat |

Moreover, when it comes to R&D by the business sector the level for Finland is maybe 3 times higher than the EU27 level.

|

| source: Eurostat |

If we look at all 3 charts it becomes apparent that R&D expenditures in Finland is rather high for all performing sectors and this along with the fact that they collaborate closely gives the country and its firms an edge. On the other hand, in the Irish case, R&D is mostly funded by the business sector and it surpassed EU27 average since the ‘00s.

What I think would be interesting to find out is whether Finland and Ireland possessed a comparative advantage in these sectors before the boom. First, let’s take a look at the sectors that were the driving forces behind the boom.

|

| source: OECD |

The sector that powered ahead in Finland was Electrical and Optical Equipment. Before the boom its importance was definitely smaller but it was by no means inexistent.

|

| source: OECD |

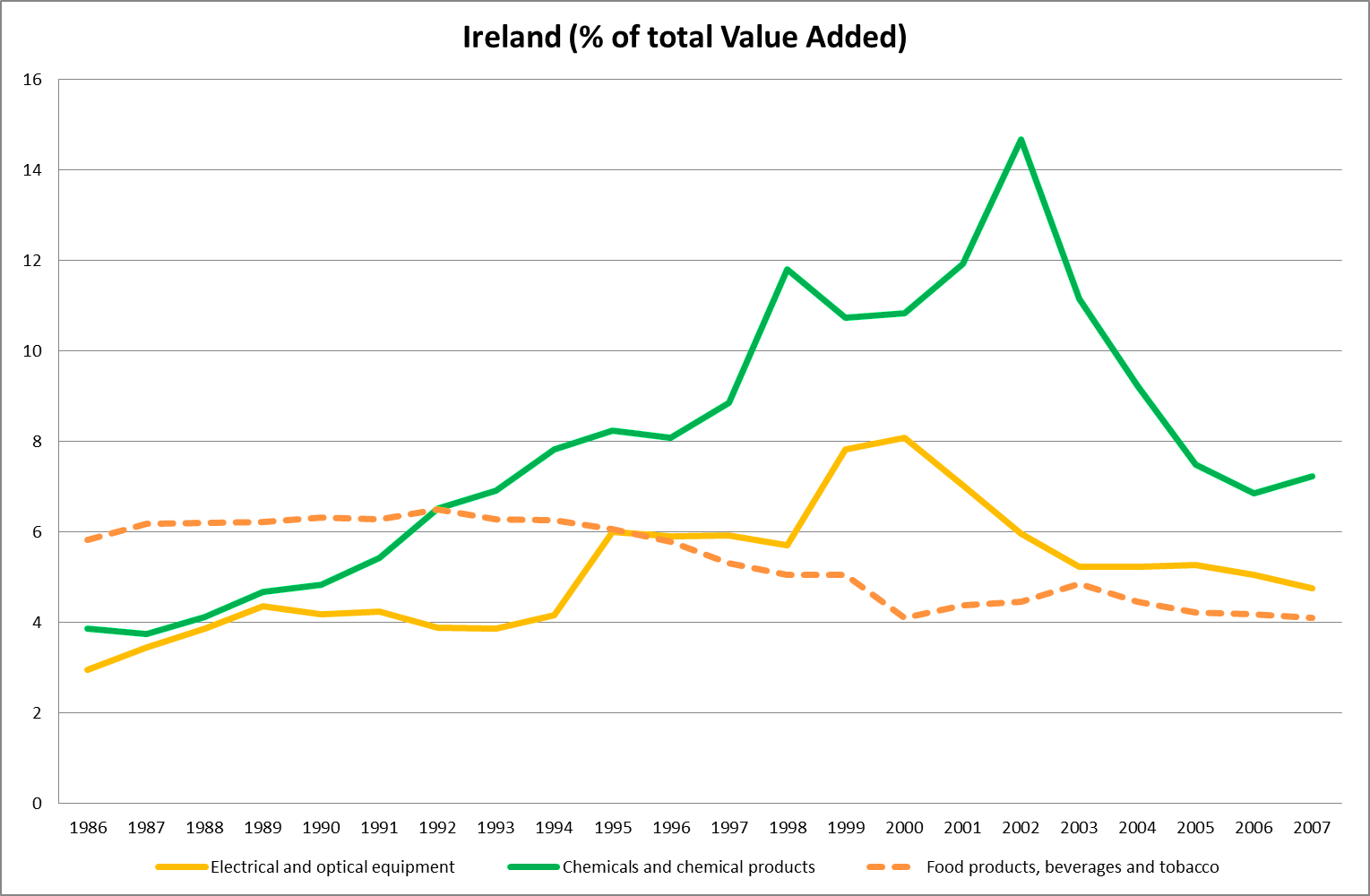

In Ireland, two sectors did the heavy-lifting, Electrical & Optical Equipment and Chemicals. The story here is the same, both sectors were not that important before the boom but no one can claim that they were negligible, especially Chemicals.

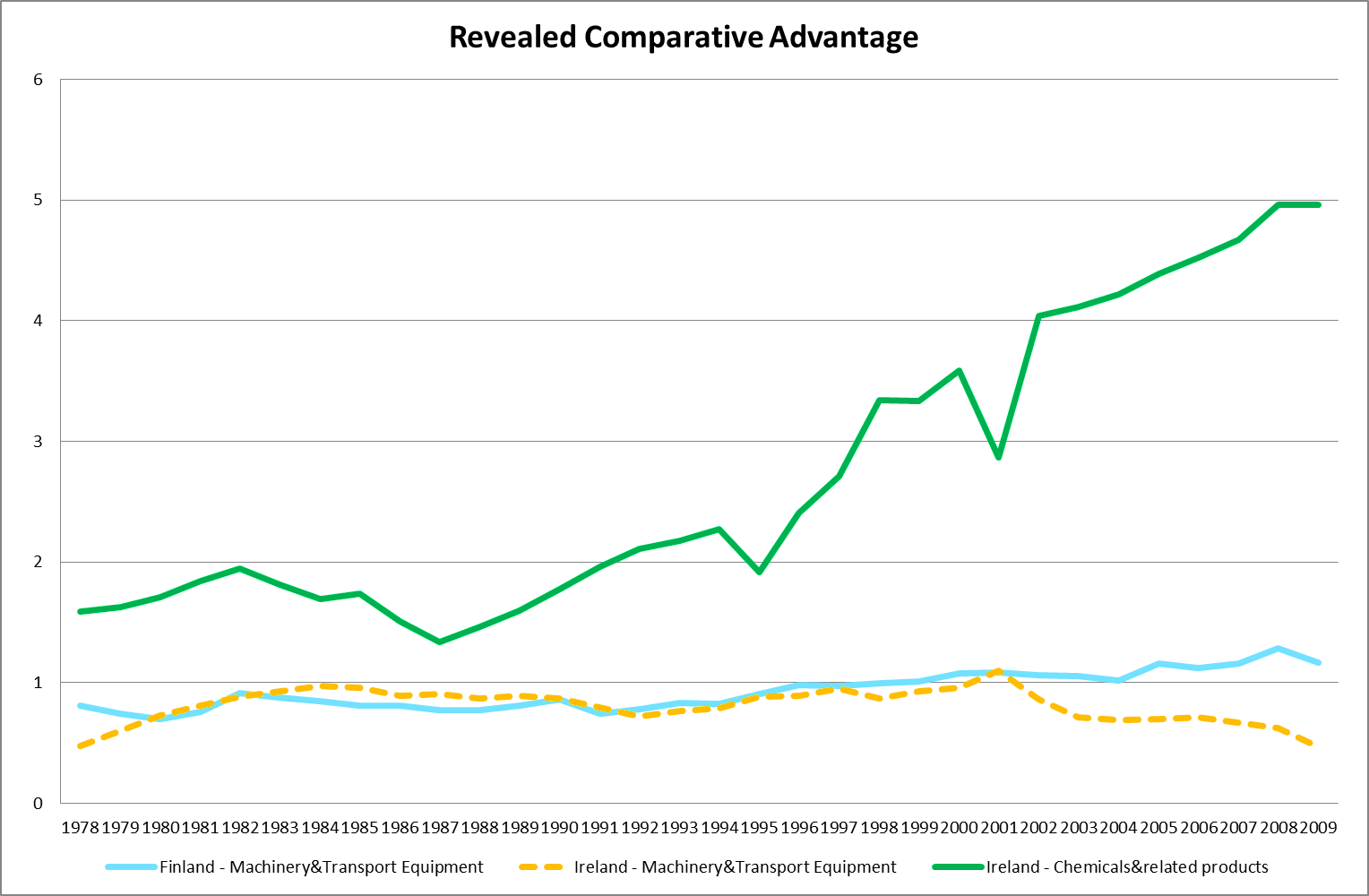

The OECD calculates the Revealed Comparative Advantage indicator. A value greater than 1 implies that products from this sector comprise a greater share of this country’s exports than the world average.

|

| source: OECD |

So before the re-industrialization process begun, Finland was borderline not-specialized to machinery, as was Ireland, while Ireland was specialized in exporting chemicals. This serves as evidence that nothing happens out of the blue and some foundations are required before a sector takes off.

Finally I want us to have a look at what the business and regulatory environment in the two countries is like. The next two charts are interesting.

|

| source: World Bank – World Governance Indicators |

|

| source: World Bank – World Governance Indicators |

Finland ranks at the top percentile for almost at every world governance indicator. Ireland is not as good as Finland but still ranks especially high in all indicators.

All in all, I think that we can safely deduce that for Ireland and Finland to re-industrialize they did get an awful lot of things right.

First of all, they built a favorable business environment, either for the local firms to grow and compete or for the MNCs (MultiNational Corporations) to choose to invest in Ireland. They invested heavily in R&D and they were flexible enough to grab the chance that the technological advances in the ICT sector offered. At the same time they were a bit lucky too but with all the effort they put into this and their strategic vision I think that we can safely say that luck takes the back seat this time.

Of course, getting it right then doesn’t mean that they are invincible and true to that, this re-industrialization process that was initiated in the early 90s has reversed or stalled at best. The effects of world trade, offshoring, outsourcing and a million other factors make the world (for good or for bad) a very dynamic and ever-changing place nowadays. Furthermore, for them to initiate this process, a technological “revolution” was required, it didn’t come out of the blue and certainly such opportunities do not arise every day.

The outlook for free trade, something essential for smaller countries that wish to do what Ireland and Finland did, is somehow clouded and uncertain due to the economic plight that the world finds itself in. Of course the nature of production processes is a lot different than what it was at the time of previous breakouts of protectionism, but then who said that history repeats itself, it only rhymes. I wouldn’t be surprised if we right now are just in the first bends of a rather curvy road with especially low visibility.