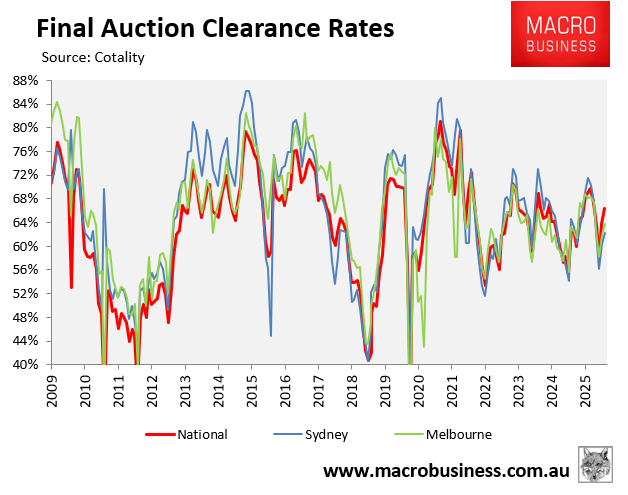

Despite the strong prospects of an interest rate hike, the nation’s final auction clearance rate bounced last weekend.

Source: Cotality

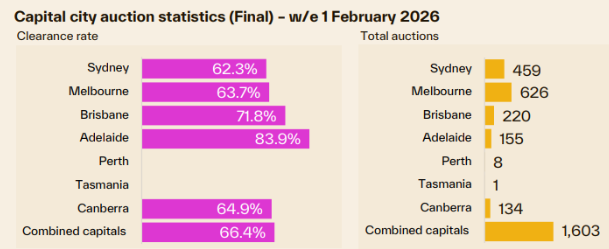

Cotality recorded a final clearance rate of 66.4% last weekend, up from 57.1% in mid-December and 59.4% at the same time last year.

Melbourne’s final clearance rate was 63.7% last week, up from 58.4% and 58.6% at the same time last year.

Sydney’s final clearance rate was 62.3%, up from 52.6% in mid-December and 59.6% this time last year.

Both Sydney and Melbourne recorded their highest final clearance rates since the week ending 9th November 2025.

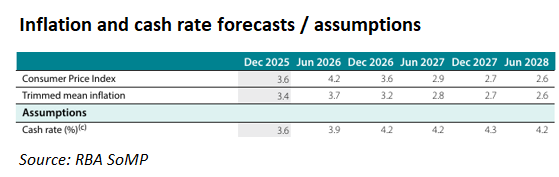

This weekend’s auctions will provide a major test for the housing market. The Reserve Bank of Australia (RBA) lifted the official cash rate by 0.25% on Tuesday and flagged higher inflation and further rate hikes ahead.

The RBA’s February Statement of Monetary Policy (SoMP) assumed that the official cash rate would rise two more times by late 2027, with trimmed mean (underlying) inflation to increase in the near term and not decline to the midpoint of the RBA’s target range until after June 2028.

Financial markets are also now tipping two more rate hikes from the RBA:

Latest interest rate futures official cash rate pricing.

Three interest rate hikes of 25 basis points imply a variable mortgage rate above 6% and a $330 increase in monthly repayments on the average $700,000 new mortgage. Three rate hikes would also lower borrowing capacity by around 12%.

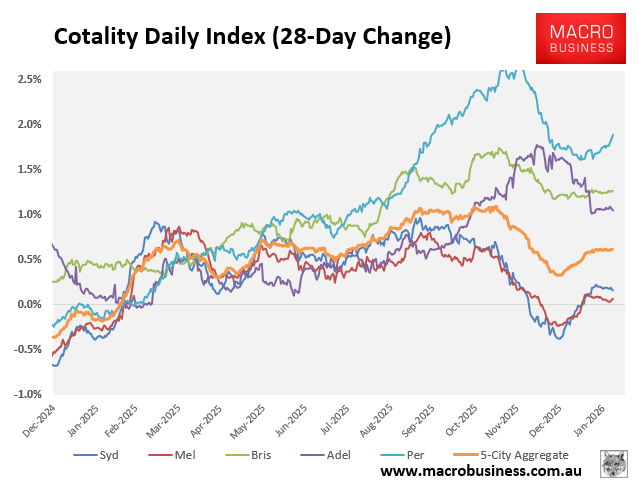

Cotality’s daily dwelling values index shows that home prices continue to rise at a solid pace, driven by the smaller major capitals of Brisbane, Perth, and Adelaide.

However, the prospect of a 75 bps tightening and a 12% reduction in borrowing capacity is expected to put the market under stress.

The first major test arrives this weekend with the first auctions after the RBA’s rate decision.

It will be fascinating to observe whether buyers retreat to their caves, spooked by the prospect of higher mortgage payments and potentially future price falls.

Will the ‘fear of missing out’ (FOMO) turn into a ‘fear of overpaying’ (FOOP)?