Yesterday’s oil production chart prompted some interesting discussion on the economic outlook for a world facing physical limits to energy resource extraction, and the peak of oil production in particular It is one more important factor to add to the impact of debt dynamics and the political response to recessionary conditions when considering the global economic outlook.

I have some expertise on the interaction of energy supply and economic growth and will put forward my views on the matter in this post. First, however, I need to be clear that my expertise is not of a engineering or geological nature, so the real scope of expanding production of oil, tar sands, coal seam gas, and even renewables in the near future is the uncertain part of my analysis (and of the industry in general). Most graphs in this post are from the BP Statistical Review of World Energy 2011.

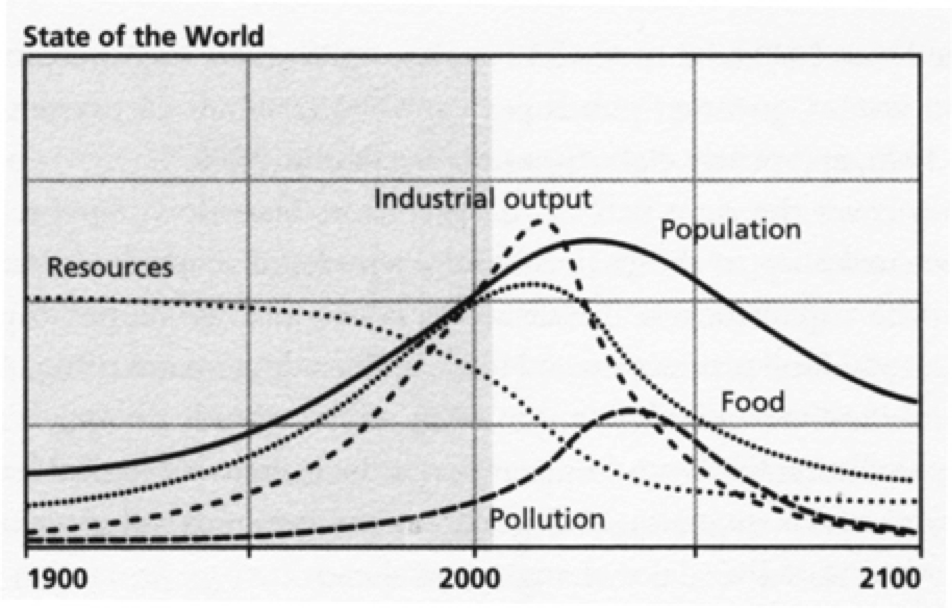

Probably a wise place to start is from the beginning of the modern Limits to Growth movement, which gained prominence with the publication of the Club of Rome’s book of the same name in 1972. This book, by Donella Meadows and colleagues, reports on the results of a computer simulation of the economy under the assumptions of finite resources. In what was cutting edge systems model simulation at the time, the World3 computer model produced scenarios showing that under various assumptions, a decline in the rate of extraction of non-renewable resources will lead to a decline in global food and industrial production, which will in turn lead to a decline in population and greatly reduced living standards for all.

The following image is one example of the results of their simulations, showing a peak of industrial output around 2010-2015.

While I don’t doubt the finitude of many natural resources, and that the human population cannot grow indefinitely, I doubt that finite limits of a handful of resource inputs to the economy necessarily means that economic growth, in terms of producing type of goods and services that provide increasing value cannot continue, even if it is necessarily at a much slower pace.

Achieving a continuation of increasing real value of production, with a declining rate of energy resource consumption, is quite a challenge. Some theories suggest that much of humanities productivity gains over the centuries have been due to a gradual process of substituting human labour for energy services, in the form of mechanisation and automation. So close is the relationship that energy use is often taken as a proxy for economic growth.

However, there are many different energy resources available on this little planet, and there will be a degree of substitution towards other energy sources and each hits their geological and technological limits to production. This substitution could enable a continued growth in useful energy sources for economic activities for some time. Coupled with gains in the efficiency of use of energy for services which consumer ultimately value, my view is that any period of economic decline, as a result of peaking production of a single energy resource, will be far less dramatic than the World3 scenario modeled in the above graph.

Substitutions will also be made to society’s capital stock over time. Our oil-dependent transport capital – the stock of vehicles, ships, and aircraft (amongst other oil-dependent industries) – will be gradually replaced to be not only more energy efficient, but potential run on different fuel sources.

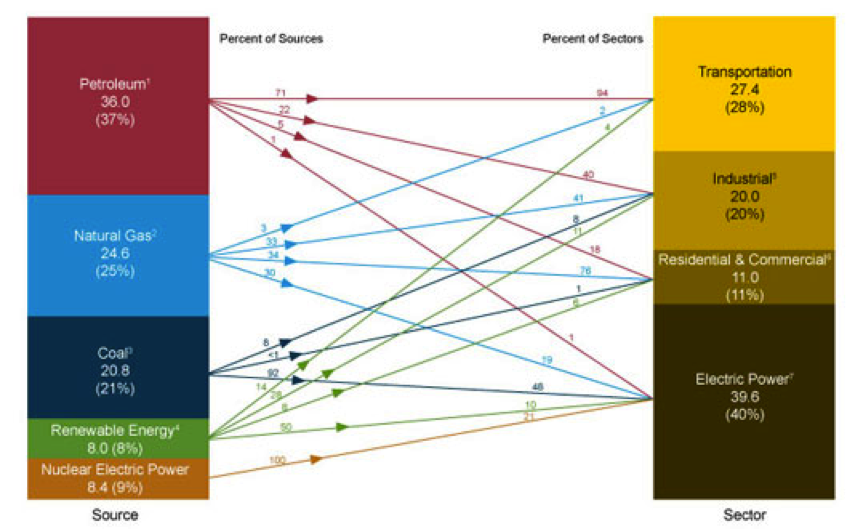

The diagram below, from the US Energy Information Administration (EIA), shows the relationships between energy source and economic activity in the US in 2010. We can see that 71% of oil consumed is in transportation, making up 94% of transport energy use. The most noticeable part of this diagram is that each economic sector currently uses multiple energy sources, and I expect the change over time to show that energy sources for each sector are becoming more diverse. A peak in oil production will continue this trend.

On the production side, we can see that non-oil energy sources have been developed rapidly over the past decade or so as a response to a combination of new technology and price signals.

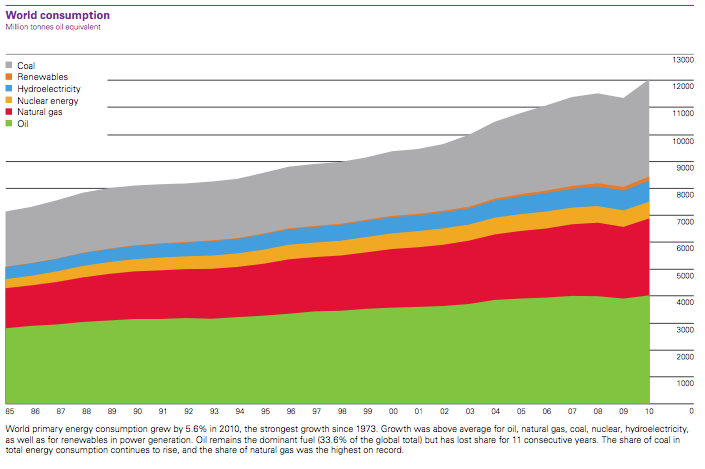

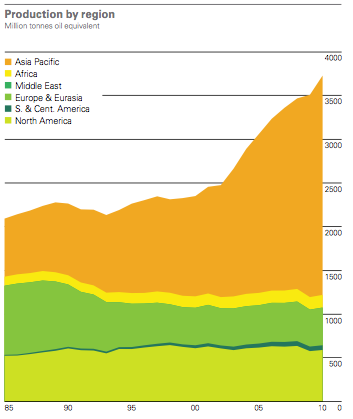

We can take a look at the big picture first, with the composition of global energy production (aka consumption). The graph below shows that the fossil fuels of coal, oil and gas have been the mainstays. Hydro-electricity, nuclear and renewables have seen more growth than oil over the past 25 years.

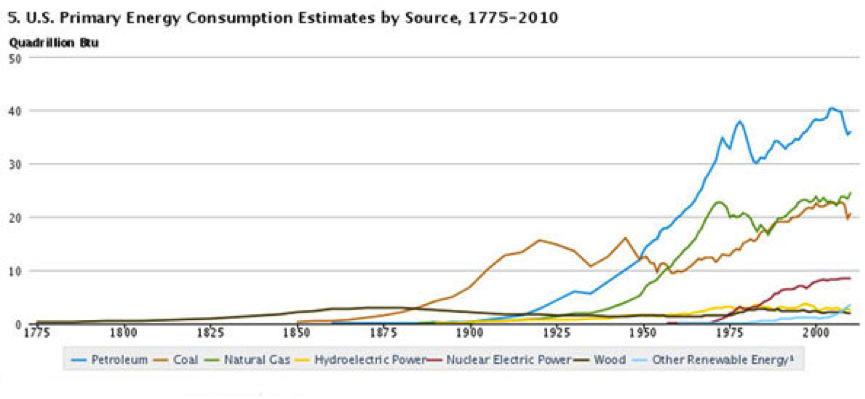

In the US over the very long term we can see the gradual changes in energy source composition more clearly, with coal seeing a long period of stagnation while oil, gas, and later nuclear, were rapidly growing (below).

Next, we can break down each energy source and examine the production and price changes over time to give a better indication of how energy substitution is currently playing out. You will have to excuse the fact that I am ignoring the geopolitical gaming that often accompanies large-scale resource development, and especially the role of State-sponsored energy companies in Brazil, China and elsewhere. The political side of resources is also an important determinant of market conditions.

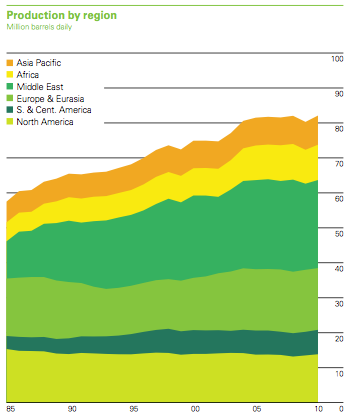

First cab off the rank is oil. We can see clearly in the graph below that global oil production has plateaued since around 2003, and that North America has seen a gradual decline in oil production, while the Middle East is the source of most growth of the past few decades.

The simple economic argument is that if prices increase, and the only barrier to supply is increasing marginal costs, then production volumes should increase. For the wonks out there, resources are one of the few markets that closely behave as predicted by the basic medium term supply and demand framework, as they typically face increasing marginal cost for expansion of production due to geologically more difficult locations of each new deposit discovery.

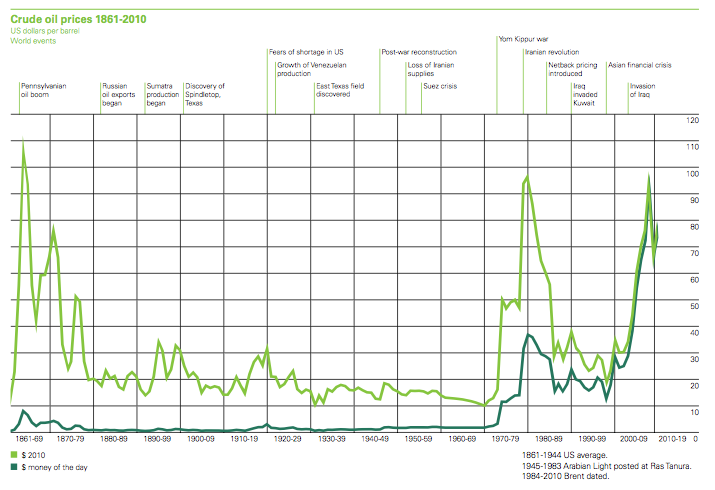

Since 2005, crude oil prices have stayed stubbornly high (below), even in light of the slump in global economic activity as a result of the financial crisis. At the same time, oil production volumes globally have plateaued, with no more oil being produced in 2011 as 2005. This is unlike many other energy resources, and does signal that supply is restricted. That is not to say that there are not many oil companies looking to take advantage of the price, and that with substantial investment, more oil could be produced from marginal reserves in the future. Without a new technological advancement in oil extraction, the chances of a renewed growth in production are slim, and the expectation is for the plateau to continue for the immediate future.

Moving on to coal, which has seen similar price gains over the previous decade, in the order of 200% in some cases. Production volumes have also grown dramatically, with global production around 60% higher than a decade ago (see below). This is typically the type of supply response economists expect from price increases in resource markets, indicating perhaps even moderate rates of production growth are achievable at prices below the current level. Whether or not any kind of global agreement in climate change heavily impacts this market in the near future is yet another political game I will have to ignore for now (but previously considered).

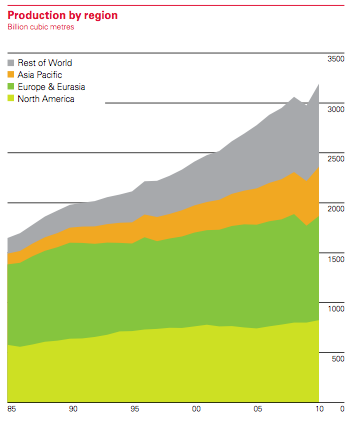

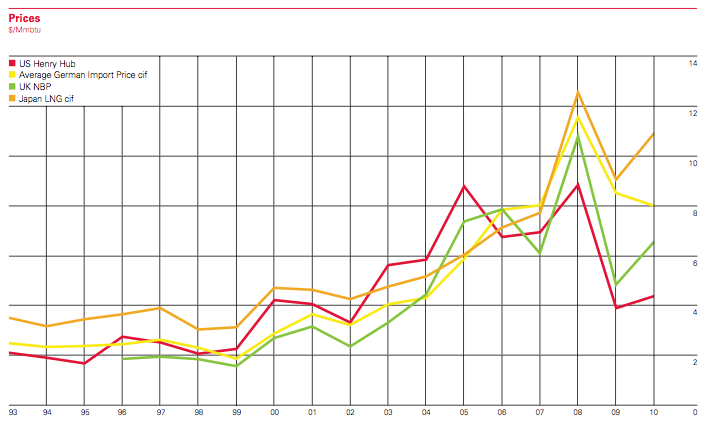

Natural gas shows the same expected market response to prices increases we saw with coal. Prices have risen significantly since around 2003, along with production across most regions.

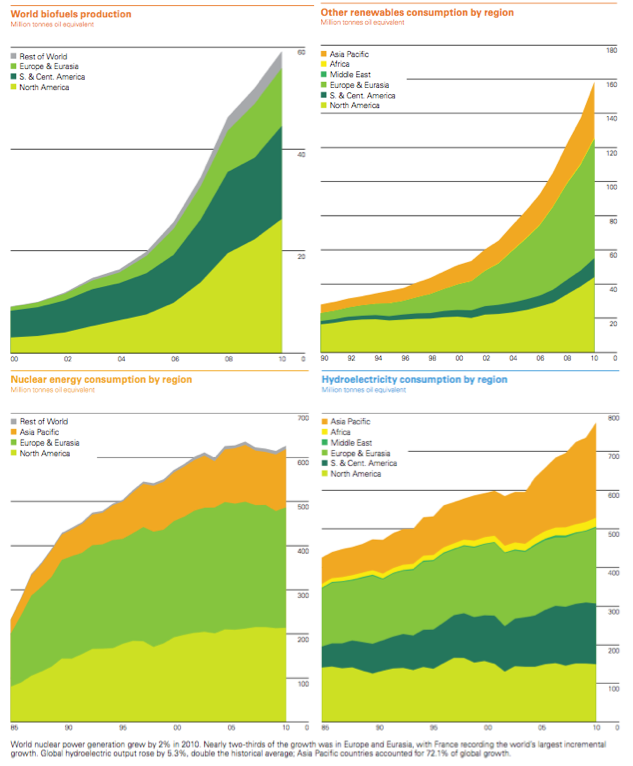

Finally, the remaining 15% or so of world energy production – nuclear, hydro, biofuels and renewables – show extremely high growth rates in terms of energy production. There are some exceptions in this bunch. The nuclear industry is expected to continue its decline, while limits to suitable locations for large-scale hydro may temper the growth of this industry, even if opportunities for small-scale hydro are widely embraced.

The future of bio-fuels is particularly uncertain and prone to political influence, due to the relationship between food cropping and biofuels production. Complementary food production with bio-fuel by-products is one area that will continue to grow.

Development of all these renewable energy sources will be supported by technological innovation, which, relative to fossil fuels, is in its infancy.

Where does all this leave us?

First, we need to acknowledge that cheap energy has been a key ingredient in the rapid economic growth seen over the past century. But, the above discussion shows that substitution of energy sources is a slow ongoing process that the peak of oil production may simply accelerate, but may come at a cost to the rate of growth.

And there are many other factors at play.

The rate of population growth will greatly determine the per capita wellbeing in a time of limited growth due to an energy transition. If the trend of declining population growth continues (global population growth now around 1.1% compared to 2.1% in the 1960s), this will contribute to maintaining per capita wellbeing.

Further, developed societies may adjust to taking productivity gains as leisure time instead of more work time, dampening growth in demand for energy resources.

Often forgotten is that fixed resource inputs, even critical ones, don’t always stop growth. There are always 24 hours in a day, but that doesn’t stop us producing more each day. If a shortage of hours was encountered, would a sudden change to 23hrs (a 4% decline) have a dramatic impact? Or would society easily adjust to this new environment with minimal impact on quality of life?

While a smooth transition to prosperity under much greater limits on energy resource inputs to the economy is theoretically possible, I don’t expect this to be our future reality. Self interested governments, businesses and the general public will react to short term shocks in unexpected ways, potentially promoting conflict, and taking the bumpy road. But the peak of oil production itself will not stop progress altogether.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin