In today’s Bonds Spotlight we take a look at the recently-released Origin floating rate notes. The $900million in debt was raised primarily to fund Origins contribution to the Australia Pacific LNG project.

The Key Details

| Security type | Floating rate note |

| Coupon rate: | 90 day BBSW + 4.0% |

| Face value: | $100 |

| Payment schedule: | Quarterly, in arrears |

| First payment: | 22 March 2012 |

| Maturity Date: | December 22, 2071 |

| Convertibility: | None |

| Funds raised: | $900 million |

| ASX code: | ORGHA |

Origin notes are dated, unsecured, subordinated and cumulative. This means:

- They have a redemption date (albeit 60 years in the future)

- They are not backed by a mortgage or security over an asset

- They are subordinate to all other security classes (except equally ranking debt and ordinary shares) in the event of a default or company windup

- Any deferred interest payments on the notes accumulate – that is, they cannot be forfeited and must eventually be paid (except in the case of default). Missed payments also compound at the prevailing interest rate

Payments will be mandatorily deferred if Origin violates their interest cover or leverage ratios (see below for more details).

The margin (currently set at 4% and added to the 90day) will increase to 5% should the notes not be fully redeemed by December 22nd, 2036. The margin will be increased by an additional 5% (i.e to 9% or 10%) in the event that Origin is bought out by another person or entity.

The Business

Origin is Australia’s largest energy retailer with over 4 million customers. It is active across the entire energy supply chain, from oil and gas exploration to electricity generation, wholesale and retail supply. They also own 43% of Australia Pacific LNG, which is seeking to develop one of Australia’s largest coal seam gas to liquefied natural gas projects in central Queensland.

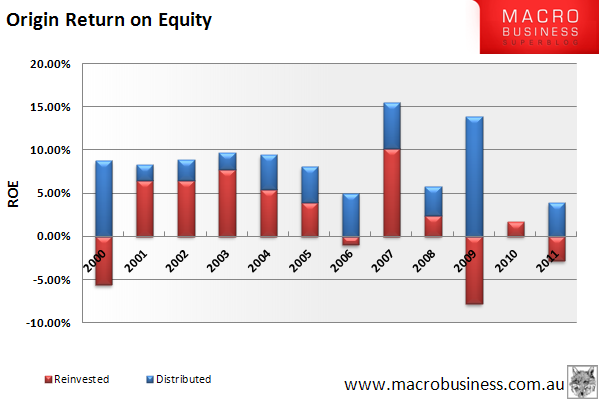

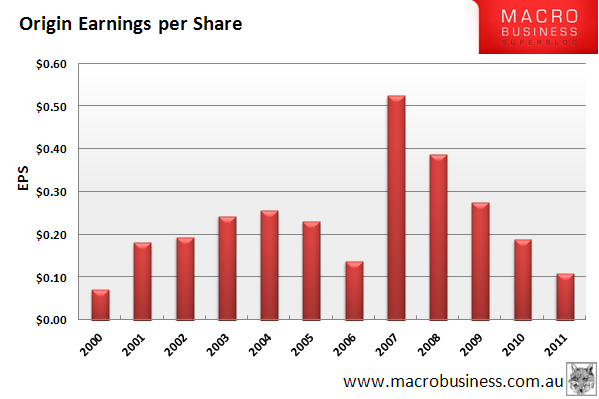

From an investors point of view Origin appears a stock-standard public utility company. Return on equity is relatively low (averaging around 6.5% over 10 years) and has been decreasing over the last few years – due to both decreasing earnings and increasing equity from capital raisings (see graphs below).

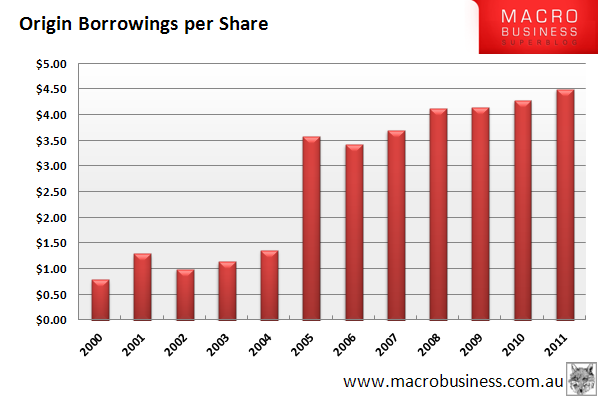

Debt is also increasing, especially after the $900 million dollar notes raising which isn’t shown in the graph below.

Origins size and position in the energy market are a positive given how inelastic demand is for electricity. We’ll also want (and need) more of it and Origin will be there to both generate and supply.

Are they good for it?

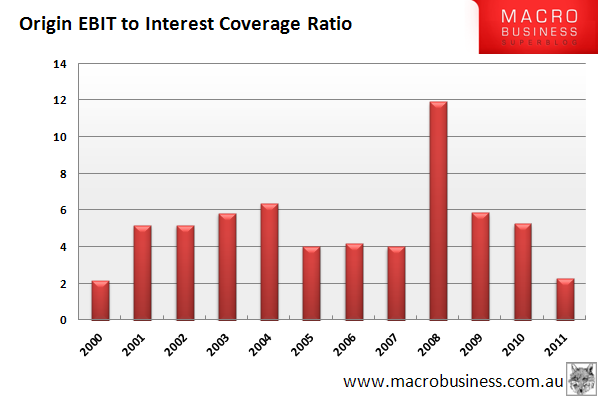

As a potential bond investor, we’re interested in whether the company can cover its interest obligations. The notes are new, so they’ll be an additional burden to the borrowings already reported in 2011.

Looking to Origin’s history, we can see that their coverage ratio (EBIT divided by interest paid) has hovered between 3 and 4 for most years. The big drop in 2011 is due to hefty transition costs incurred with acquisitions of NSW electricity assets.

At the current 90 day BBSW, the note coupon of 8.45% will result in an extra $76m in interest expenses for Fy12. Using a little extrapolation, I would expect the coverage ratio to come in around 2.5 next year.

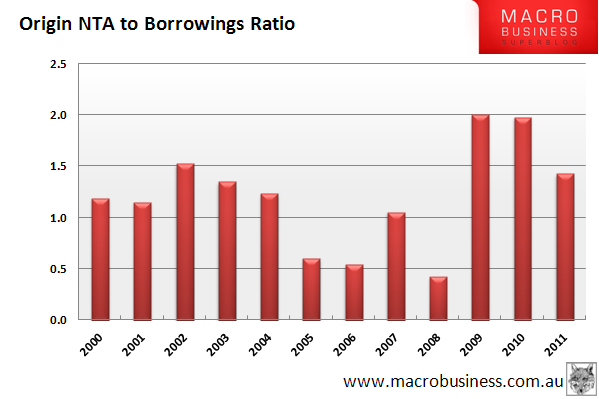

Another useful measure for public utility-like companies is the net assets to borrowing ratio – a measure of the value of their tangible assets to their total borrowings. The true value of Origins NTA bounces around a little due to equity fluctuations caused by hedging/commodity exposures, however its historical NTA to borrowings has average 1.2 – giving themselves a 20% buffer.

The Return

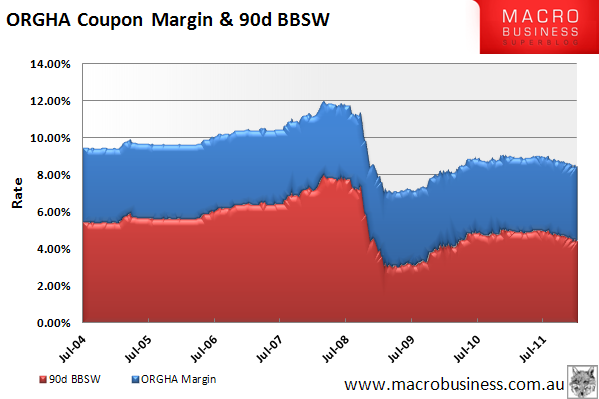

With the 90d BBSW currently sitting at 4.5%, meaning the coupon currently sits at 8.5%. However, this will fluctuate with the 90d BBSW, which is shown below.

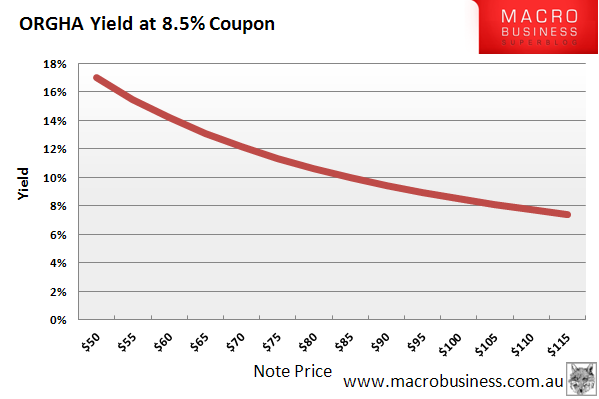

ORGHA is currently trading for about $103, which puts its running yield at 8.25%. The yield vs price at the current coupon shown below.

For a comparison, the yields of a few other investments are shown below:

| Australia government bond yield (5y) |

3.34% |

| At-call bank deposit (Ubank base rate) |

5.61% |

| Woolworths dividend yield |

4.7% |

Summary

In my opinion, the ORGHA notes are a little over priced based on their interest coverage ratios. The 90 day BBSW may also be heading south given the RBAs current easing stance, meaning the note coupon would also drop.

If the CSG to LNG project comes through and earnings increase, then Origin shouldn’t have too many troubles paying their bills. However, the past few year’s earnings have been a little variable (and low) for my liking. Origin can probably tap the capital market again for funds if things get hairy, but personally I will be waiting to see if the notes trade below their face value before I’d consider buying.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has currently has no interest in the business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.