Another weekend…. and we are still waiting for an outcome on Greece. The chief negotiators from Institute of International Finance (IIF) have left the country yet we still haven’t heard anything that sounds remotely like a deal. FT reports that the brinkmanship hasn’t ended but there doesn’t appear to be too much wiggle room left:

Private owners of Greek debt have made their “maximum” offer for the losses they are willing to accept, the bondholders’ lead negotiator has said, implying that any further demands could kill off a “voluntary” deal and trigger a default.

Charles Dallara, managing director of the Institute of International Finance, said in an interview that he remained “hopeful and quite confident” the two sides could reach a deal that would prevent a full-scale Greek default when a €14.4bn bond comes due on March 20.

As I said last week, we will all just have to wait and see. There are many unknowns as to whether an initial deal can be struck and even if it can whether that will be enough. Is the rumoured 65-70% loss correct? Do the hedge funds have blocking position? Will Greece need to retrospectively apply a collective action clause to get a high participation rate? CDS triggers then? What about the ECB? Will the rest of the EU agree given they have a post-deal target of debt to GDP at 120%? Will there be any corresponding legal action?

Lots of questions, but no real answers at this stage. What we do know is that Greece has a €14.5bn bond payment on 20 March and to meet this obligation it almost certainly needs another bailout. If the PSI deal is not completed quickly (possibly by the next EU summit on the 30th of Jan) then Greece will not get the additional support it requires and will therefore default in 2 months.

It is true that 2 months is a very long time in European economics so anything could happen between now and then, but the outcome of Greece, either way, is adding pressure on to the other weak links of Europe, such as Portugal:

Greece’s talks with creditors are currently proceeding under the rubric of a “voluntary” restructuring. Yet ratings agencies have stated unequivocally that anything other than the original bondholder terms will be classified as a technical default. Greece, Zervos says, will be “the first example in a developed market for how you deal with sovereign default.”

All of which puts Portugal in a precarious spot. Most private investors have already fled the country’s bonds. But market observers say a Portuguese restructuring or default could still reverberate across Europe’s shaky banking sector, plunging the euro zone’s most vulnerable economies–and perhaps the entire global economy–into financial peril.

I am not sure that “peril” is the correct word, but there is no doubt the outcome of Greece, one way or another, will have an effect on other periphery nations. This year Portugal enters its third year under a bailout and this year is expected to be the toughest with more tax hikes and the elimination of two months of pay for civil servants. The government is already calling for a economic contraction of 3%, but a look at the latest stats from the central bank suggest much worse.

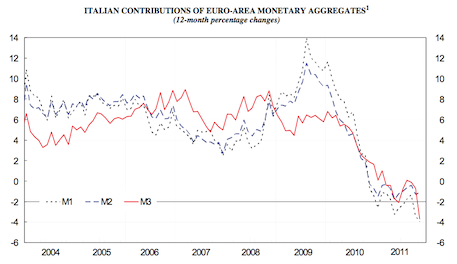

As we have seen in Italy, private sector deleveraging is accelerating led ,in part, by austerity government policy but also due to “zombification” of the banking system:

{kind=link}

I also note that many economic indicators are heading in the wrong direction:

The Portuguese government did meet its obligations under its bailout agreement in 2011, but only by using a one-off transfer of money out of the banks’ pension funds to the government. In 2012 there is no backstop and therefore targets are unlikely to be met.

Over the weekend the government, with the final support of unions, introduced new reforms in an attempt to boost competitiveness including making it easier for employer to hire and fire staff, cutting holidays and severance pay requirements. It is yet to be seen if these changes can have an effect on the shrinking industrial output, but given the deleveraging environment this seems unlikely. Either way, the last thing the country needs at this point is a break-down in the Greek PSI talks that leads a further deterioration of trust in Europe’s periphery economics.

In other news Croatia wants in, Dexia is suing JP Morgan over mortgage securities and finally, Monti wants a trillion, the Germans want none of it, Draghi suggests something in the middle.

Apologies for late post today, readers. Kids went bananas this morning!