There is widespread acknowledgement that Australian tax rules, particularly negative gearing and capital gains tax (CGT) discounts for assets owned for more than a year, lead to higher home prices (and reduced tax revenue for government – in the order of $2.5billion pa). Together, these tax rules tilt returns in favour of owning residential property for investment rather than occupation. Even the tax-free capital gains on the family home are insufficient to make owner occupying a more attractive financial position.

Even the financial illiterate will know these rules increase prices simply by looking at the vested interest group most vocal in support of them – the property industry.

So how big is the price impact?

The short answer is ‘it depends’. But it is always positive.

Below are a series of models demonstrating the scale of price impacts under various scenarios. What we learn from this investigation is that not only do these two tax rules work in tandem to increase prices, while the scale of price impacts is dependent on investor expectations of capital growth – the higher the expected capital growth, the greater the price impact. In this way, the asset price cycle is amplified by these rules.

We also come to realise that the rules are a political construct, and actually do serve the purpose of allowing markets to deliver private provision of rental accommodation by making the investment market the price setter, rather than the owner-occupied market.

The models

All models are discounted cashflows, calculating the purchase price based on investor expectations of after tax return on equity (ROE), along with the following assumptions and specifications:

- 7 year holding period

- 80% LVR

- 7% mortgage interest rate

- 45% marginal tax rate (the current to income tax rate)

- Weekly rent of $250

- Operating costs of 2% of value (each period)

- Other transaction costs ignored (stamp duty, commission, legal fees and searches)

In the baseline case, of no negative gearing or CGT discount, losses carry over to the sale period and subtracted from capital gains to calculate CGT liability.

All numbers are arbitrary and are simply used to demonstrate the relationships between price and other factors. However it is important to note that while there are huge price variations, housing will be equally affordable in all cases since the rent does not change. Take this as a warning when drawing conclusions form comparisons of prices to household income. Prices are very sensitive to tax rules, growth expectations, and interest rates, all of which need consideration. Also, in Australia, the investment market usually sets the price of housing.

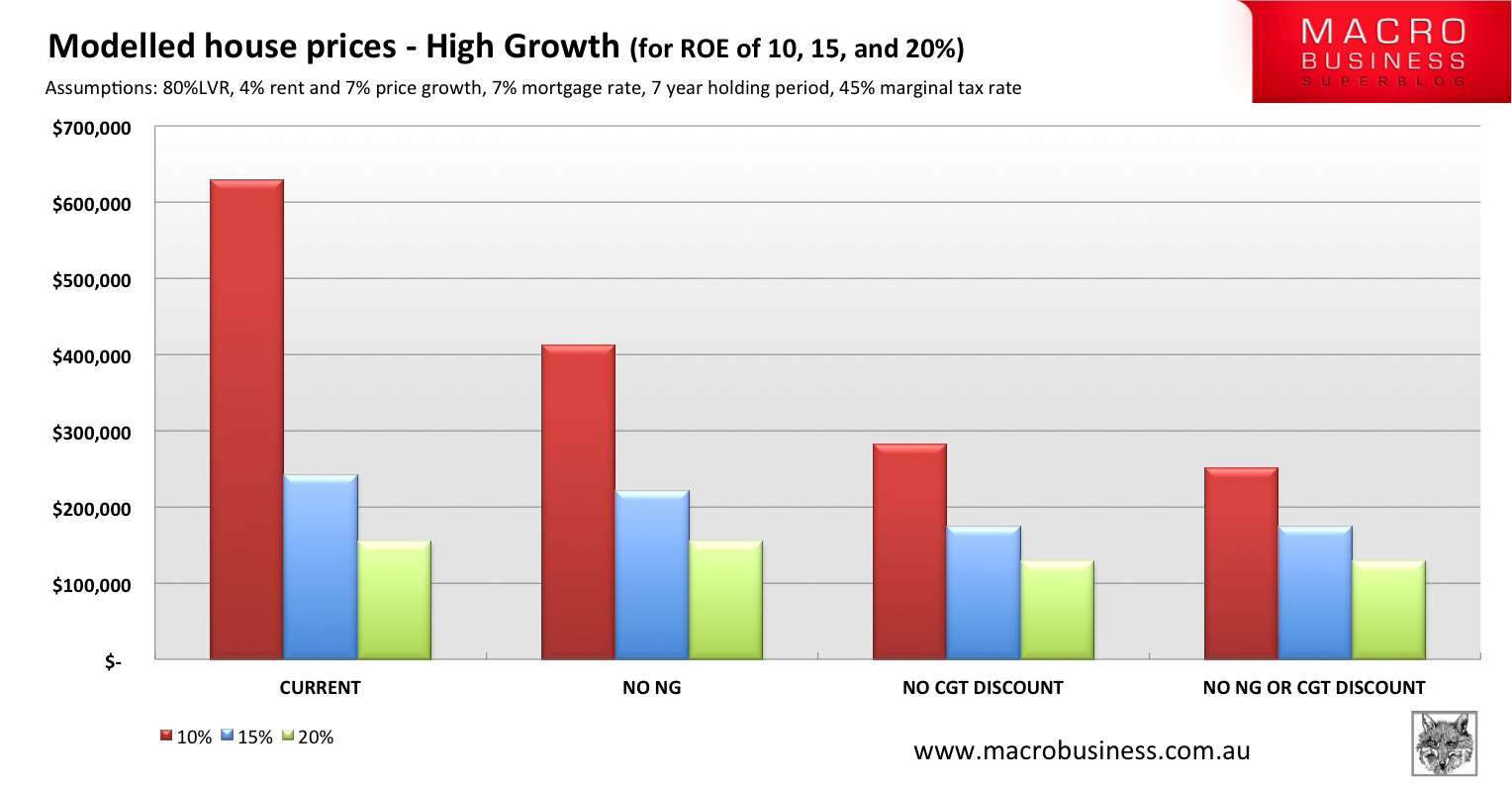

Scenario 1 – High growth high return

This high growth model is based on an assumption of 7%pa capital gains (which the property industry assures us is typical), and 4% rental price growth:

In this model, the price setting investor is seeking an after tax ROE of 10,15 or 20%. The removal of negative gearing alone (while keeping the CGT discount), would reduce the price by between zero and 35%, depending on whether expectations of ROE are 20% or 10%. I would imagine that the reality of the last decade in Australia is in this, albeit large, ballpark.

Removal of both tax rules (noting that removing these rules treat residential property inconsistently compared to other asset classes) reduces prices between 20 and 50%.

The CGT discount is also shown to have a larger price effect than negative gearing (since negative gearing brings forward tax benefits, while the CGT removes a tax obligation). This CGT price effect is sensitive to the holding period, where the longer the expected holding period, the lower the price impact.

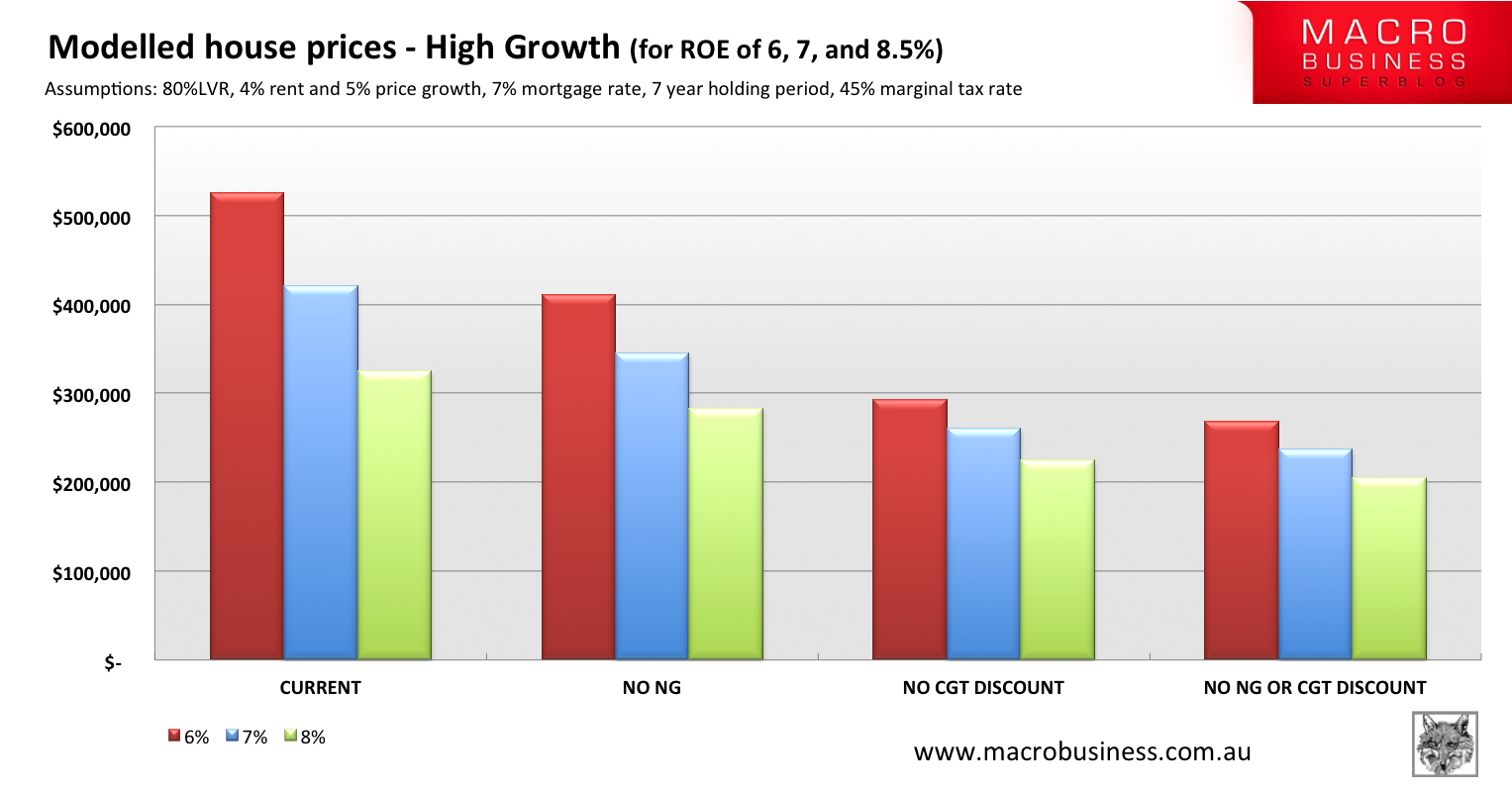

Scenario 2 – High growth, low returns

More moderate capital growth expectations of 5%, plus rental growth expectations of 4% are used. Also, much lower after tax ROEs are used in this demonstration:

We again see the consistent pattern of price reductions from removal of the two tax rules, and the more substantial price impacts from the CGT exemption. Negative gearing prices effects alone are between 20 and 25% in this model.

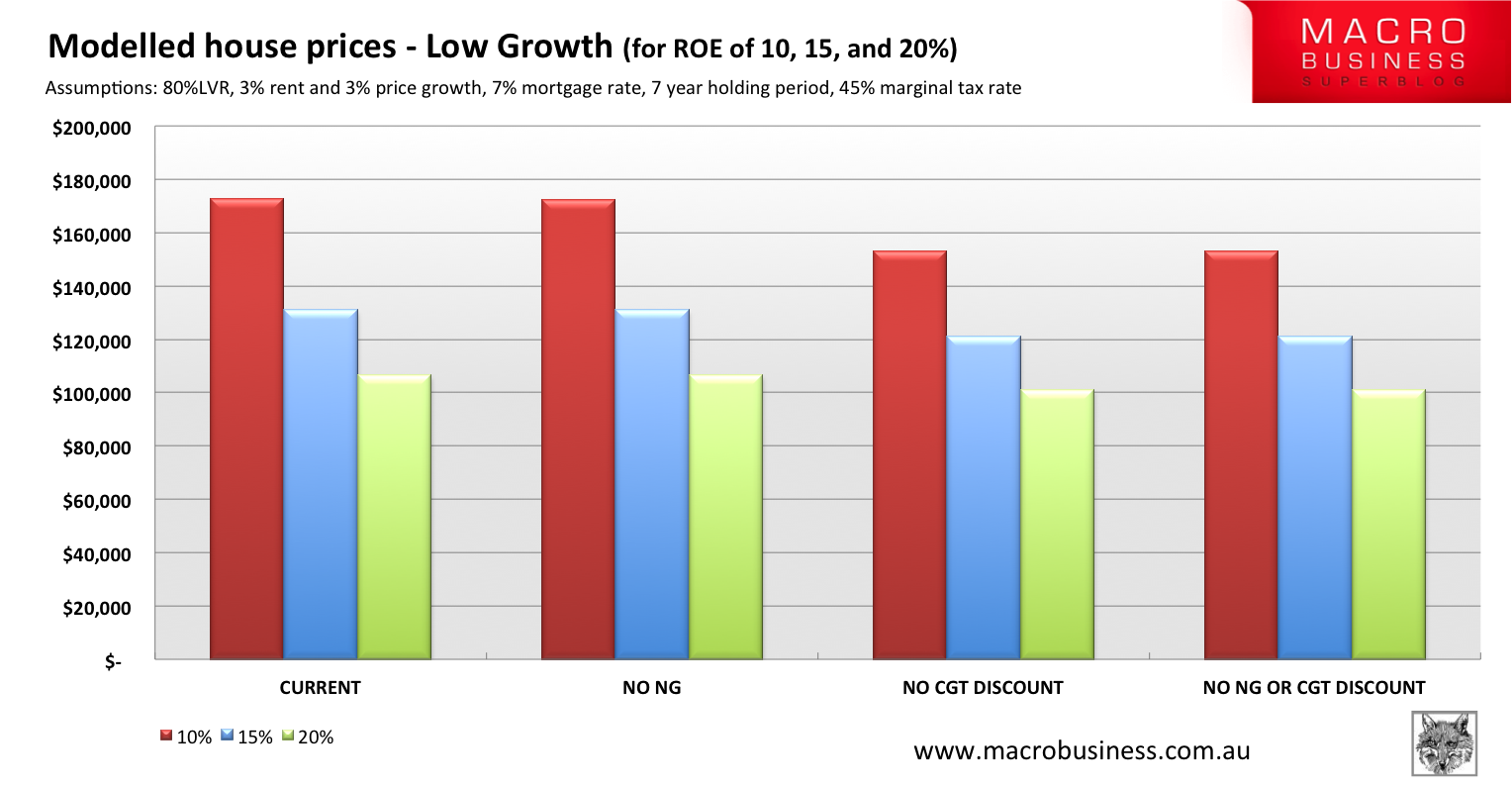

Scenario 3 – Low growth, high returns

Rental growth and capital growth expectations are both 3%:

We see a new pattern emerge in the low growth scenarios. Since capital growth is low, there is little justification for incurring costs each year in anticipation of cash flow from capital gains in a later period (especially with the high after tax ROE).

Negative gearing is this scenario has no price impact, while removing the CGT discount would decrease price by 11%.

The political implication of the investor price requiring positive cash flows is discussed later in the post.

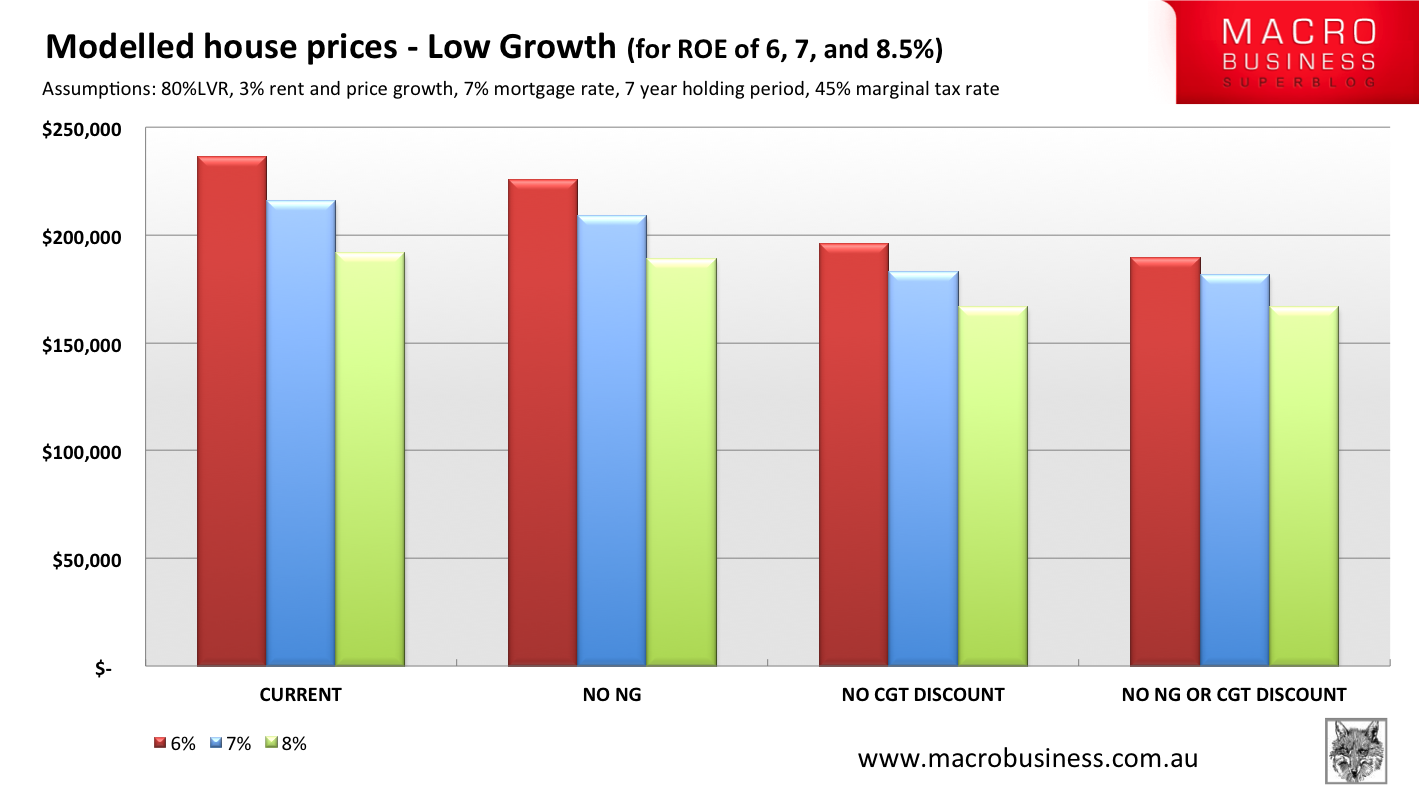

Scenario 4 – Low growth, low return

In this scenario rent and capital gain expectations are 3%, and investor after tax ROE expectations are all below 10%:

In these models negative cash flows are justified in all but the baseline case of no negative gearing or CGT discount (although the first two years cash flows are negative). Negative gearing has a very minor impact – just 1-5% on price.

In this scenario, removing the two tax rules would decrease prices between 15 and 20%.

What does it mean?

From these simple models we can observe a number of relationships:

- The lower the after tax ROE expectation, the greater the price impact from negative gearing and CGT discount

- The CGT discount has a higher price effect than negative gearing at a holding period of 7 years

- The higher the growth expectation, the greater the price impact of negative gearing and the CGT discount

- When capital growth is expected to be low, but ROE is expected to be high, the investor’s rational price will be below the cost of renting.

We also know from the model construction that the longer the holding period, the lower the price impact from the CGT discount.

These relationships interact dynamically, leading to an exacerbated price cycle.

Political economy of housing

These two rules do not impact housing affordability – they impact home OWNERSHIP affordability by nudging the benefits in favour of home investment, rather than home ownership. After all, it still costs $250/wk to rent this home under all scenarios.

Is this a desirable social outcome? In a way, yes.

Governments, present and past, have taken the view that private markets should supply rental housing. If housing investment is not made more attractive to investors rather than owner-occupiers, there is a possibility that no private market for rental housing will emerge. Yet we know that some people will be incapable of saving or borrowing sufficiently to own their own homes, even if it is cheaper than renting, so that some form of rental market will be required.

Such a breakdown of the private rental market would occur because home buyers, given they typically value ownership more highly than renting, could bid up prices to, or above, that which reflects the cost of renting.

If that occurs, no investor will enter the housing market because returns would be so poor. Home ownership would simply become a consumption good that not everyone could afford.

To ensure a private rental market, tax rules appear to have evolved to ensure that owner occupying is more costly, and that investor demand sets the market price, allowing for a functioning private rental market. This is why over the past thirty years, owning has never been more financially attractive than renting (except for rapid capital gains).

How likely is a situation of private rental market breakdown if these tax rules where changed? I am not sure. But it is possible under a specific set of circumstances, and a genuine political concern. These circumstances are not that unrealistic – investors requiring a ROE around 10% with rent and capital growth at around 3%.

In any case, the creation of a functioning private market is one reason you will hear that negative gearing improves housing supply – it actually allows a private market to supply rental housing if it makes investing more financially attractive than owner occupying. Once the private market is functioning, no further tax incentives will increase housing supply. Negative gearing may simply be a case of political ‘insurance’, guaranteeing the investor housing market exists.

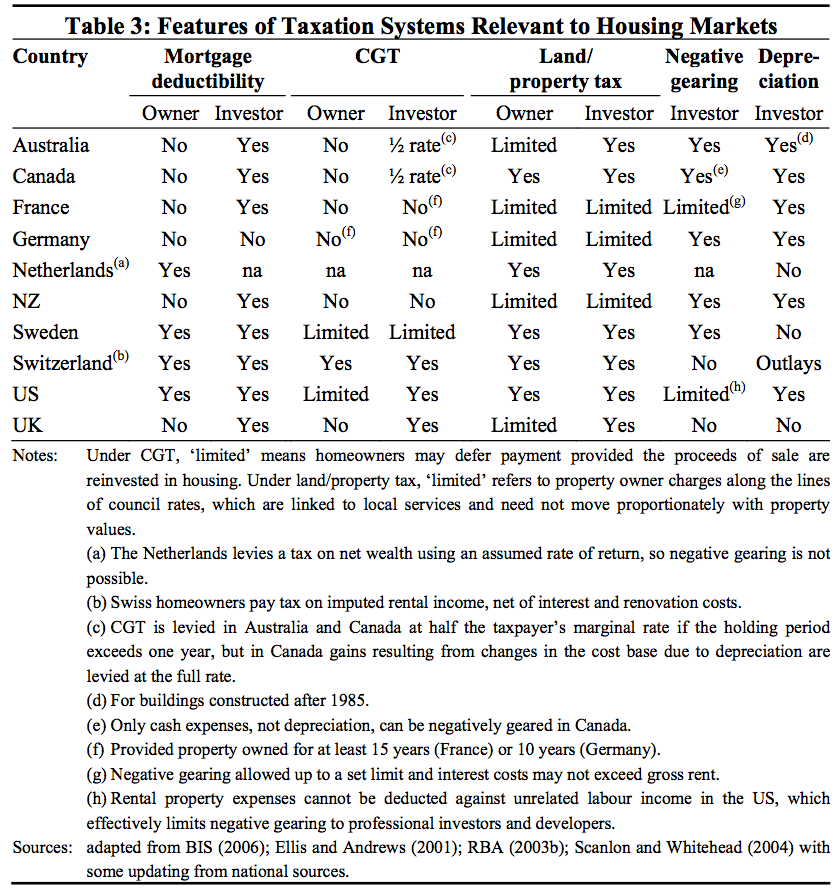

Global housing markets

The RBA’s Luci Ellis compared international housing market rules in her 2006 paper. The countries listed below, from Switzerland, to Netherlands, to Sweden, Canada and Australia, all have very different tax rules that reflect the quite different historical and institutional development of housing markets:

We need to be careful about simply plucking a set of rules from another country that seem to work well, say Germany, and applying them here. German home ownership rate is just 42%. In Netherlands it’s 49%. In Bulgaria, 97%. A history of war and housing shortage, and greatly differing rental rules also make comparisons difficult. For example, Germany and France have CGT discounts for residential property investment; but only after 10 and 15 years ownership, respectively.

Market rules need to be structured in a way to create the incentives to provide the desired social outcomes. At the broadest level, Australian housing policy appears to be a juggling act between encouraging homeownership on the one hand, and creating rules that allow a functioning private rental market on the other. We know there are also strong social benefits from home ownership, especially given our relatively landlord focused tenancy laws.

Indeed, if rental controls were to be implemented, current home owners and investors would lose out to the advantage of both renters and future home owners – but the system of private supply of rental housing would stay intact, even if the political risk makes it a less attractive investment. This would have the same effect as if all renters could coordinate a group decision to pay lower rents.

Australia has chosen to establish a set of rules that allows markets to provide private rental housing. The models show, however, that removing either of these two tax rules would be sufficient to reduce the ownership premium while maintaining the social aims of the ‘investor price maker’

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin