As H&H mentioned yesterday the mid-year economic and fiscal outlook was released by the Treasury yesterday. We have already covered quite a bit of this so I will not go into too much detail. If you are having trouble sleeping or feel the need waste a good part of a day then the monster is available at the bottom of this post.

Back in May when Wayne swan released the budget he led his speech as:

Mr Speaker, the purpose of this Labor Government, and this Labor Budget, is to put the opportunities that flow from a strong economy within reach of more Australians. To get more people into work, and to train them for more rewarding jobs. So that national prosperity reaches more lives, in more corners, of our patchwork economy.

To take full advantage of the seismic shift in global economic power, which positions us as a prime beneficiary of tremendous economic growth in our Asian region. And to succeed in the good times as we did in the bad – by choice, not by chance – by applying the best combination of hard work, responsible budgeting, and well-considered policies to the difficult challenges ahead.

Mr Speaker, this Budget is built on our firmest convictions: That just as our focus on jobs helped Australia beat the global recession, so too can a focus on jobs ensure we maximise our advantages in the Asian Century. And just as deficits are the right thing to fight a global recession, or to rebuild from natural disasters, so too are surpluses right for an economy set to grow strongly again.

We have imposed the strictest spending limits, delivering $22 billion in savings to make room for our key priorities, ensuring our country lives within its means.

And finished with:

Real GDP growth is forecast to be a strong 4 per cent in 2011-12 and 3-3/4 per cent in 2012-13.

Over 300,000 jobs have been created in the past year and the unemployment rate is forecast to fall further, to 4 1/2 per cent by mid 2013, creating another half a million jobs. Mining investment will rise to around 8 times the level preceding the boom to $76 billion in 2011-12, underpinned by the highest sustained terms of trade in 140 years.

But not every family or business is feeling the immediate benefits.The dollar is around post-float highs and this makes it difficult for some sectors, particularly those that compete in international markets. We see lingering effects from the global recession in consumer caution, a slow improvement in people’s wealth, and tighter credit, all of which has an impact on government revenue.

But with the investment pipeline ramping up and unemployment falling, the boom will test our economy and our workforce, and price pressures will re-emerge. That’s why we have strict spending limits – so that we don’t compound these pressures – and why this Budget will help get more Australians into better jobs, improving productivity and participation.

Those statements were backed up by the following figures:

- $40b deficit in 2010-11

- $13b deficit in 2011-12

- $1b surplus in 2012-13

Using GDP forecasts as follows:

- 2010-2011 2.25%

- 2011-12 4%

- 2012-13 3.75%

- 2013-2014 3%

- 2014-2015 3%

When I last reviewed the budget against its previously forecasts I noted the following:

The government seems to have done a fairly good job of predicting most of the macro economic influences on the budget. Exports, imports, inflation, Terms of Trade and employment are all in-line with predictions. However, they have stumbled significantly with private debt dynamics. They certainly did not predict the very large influence that a change in private sector credit issuance and associated spending patterns would have on the budget.

My overall feeling is that this trend has continued into the MYFEO, however the Treasury’s optimism does appear to be reaching new heights:

The downward revision to the economic outlook from Budget has reduced tax receipts by over $20 billion over the forward estimates. Lower employment growth since Budget is impacting on taxes on wages and salaries, and volatile financial markets are affecting equity prices and hence capital gains receipts.

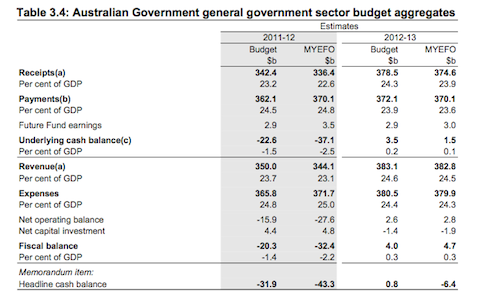

The underlying cash deficit is expected to be $37.1 billion (2.5 per cent of GDP) in 2011-12, returning to a small surplus of $1.5 billion (0.1 per cent of GDP) in 2012-13.

{kind=link}

Those figures are obviously moving away from the original estimates, but what makes them look even worse is if you actually check the forward estimates that are mentioned you realise just how unrealistic the 2012-13 numbers have become.

The forward estimates were actually only predicting a shrinkage of the deficit by $12.4 billion in 12-13 and that was when GDP was predicted at 4%. With the GDP now predicted to be 3/4 lower, again overly optimistically in my opinion , the Treasury is somehow forecasting a $42 billion dollar turn around.

Revenue is down on the back of current economic conditions, however, as far as I can tell from the document, Treasury seems to believe that is a temporary phenomena:

Tax receipts have been revised down by $4.8 billion in 2011-12 in large part because of the weaker near-term outlook for the economy. In addition, payments have increased by $2.3 billion under the Natural Disaster Relief and Recovery Arrangements, including an additional advance payment to Queensland to ensure necessary reconstruction and repair work can happen as soon as possible. Decisions to provide significant assistance to households and business as part of the policy reform to reduce carbon pollution and to accelerate funding for key infrastructure projects have also contributed to the change in budget position in 2011-12.

Tax receipts are also expected to fall by $6.1 billion in 2012-13, the areas effecting these numbers are:

- Income tax withholding receipts have been revised down by $1.3 billion in 2011-12 and $3.2 billion in 2012-13, reflecting a softening in the outlook for employment and wages growth.

- Gross other individuals’ taxation receipts have been revised down by $450 million in 2011-12 and $940 million in 2012-13, reflecting the revised economic outlook, as well as weakness in capital gains.

- Refunds are around $800 million lower in both 2011-12 and 2012-13, consistent with recent outcomes and the downward revisions to individuals’ income taxes.

- Fringe benefits tax has been revised down by $250 million in 2011-12 and $270 million in 2012-13, due to a lower than expected 2010-11 outcome and the revised labour market outlook.

- Superannuation taxes are expected to be $380 million lower in 2011-12 and $480 million lower in 2012-13, as weaker employment and wages growth results in lower contributions, in addition to lower capital gains.

- Company tax receipts have been revised down by $1.8 billion in 2011-12 and $780 million in 2012-13, partly due to lower capital gains in both years and increased company refunds in 2011-12. The impact of the refunds is muted in 2012-13 due to a range of revenue protection measures.

- Resource rent taxes have been revised down by $150 million in 2011-12 and $70 million in 2012-13. The revisions reflect increased state royalties, weaker production expectations and lower commodity price assumptions, partly offset by the lower Australian dollar.

- GST has been revised down by $820 million in 2011-12 and $660 million in 2012-13, reflecting lower consumption and subdued dwelling investment.

- Since Budget, excise duty has been revised up by $590 million in 2011-12 and $570 million in 2012-13, while customs duty has been revised down by $770 million in 2011-12 and $830 million in 2012-13. The composition of receipts between excise and customs duties has been revised relating to the relocation of a large tobacco manufacturer. Abstracting from this, tax receipts from tobacco have been revised down since Budget.

- Both the luxury car tax and the wine equalisation tax have been revised down in 2011-12 and 2012-13, reflecting the consumption outlook.

Revenues are also effected by new initiatives:

- assistance for households to meet additional costs under the Clean Energy Future package. This measure is expected to increase cash payments by $1.5 billion in 2011-12 ($6.2 billion over four years);

- support, under the Clean Energy Future package, for emissions-intensive coal mines, coal-fired power stations, Australian steel and other manufacturing industries, and those activities in the economy that are the most emissions-intensive and highly exposed to international competition to transition to a low carbon future. These measures are expected to increase cash payments by $1.4 billion in 2011-12 ($6.1 billion over four years);

- accelerating funding for a range of Nation Building road and rail infrastructure projects, including the duplication of the Pacific Highway, works on the Bruce Highway, the Interchange at Mains and Kessels Road, the Hunter Expressway, Western Ring Road in Melbourne and the South Road Superway, the Gawler Line Modernisation project in Adelaide and the Blacksoil Interchange Project. These decisions are expected to increase cash payments by $1.4 billion in 2011-12 (a net increase of $45 million over four years);

- new listings on the Pharmaceutical Benefits Scheme which are expected to increase cash payments by $67 million in 2011-12 ($445 million over four years); and

- setting aside funding to meet the Commonwealth’s share of the costs to the Social and Community Services sector for the equal remuneration case currently before Fair Work Australia.

Given the downgrades in budget revenues, the Government has found another $6.8 billion in net savings through a combination of expenditure cuts, deferrals in initiatives, and measures to improve the integrity and fairness of the taxation system. These include:

- placing an explicit price on greenhouse gas emissions through the carbon pricing mechanism. This measure is estimated to raise $17.8 billion on an underlying cash basis over the forward estimates period from the sale of carbon units, all of which will be used to help households, industry, community organisations, workers and regions adjust to the carbon price;

- deferring the commencement of the 2010-11 Budget measure that provided a standard deduction for work-related expenses and the cost of managing tax affairs by 12 months, to now commence on 1 July 2013. This measure is estimated to raise $1.2 billion on an underlying cash basis over the forward estimates period;

- applying an effective carbon price on aviation and non-transport gaseous fuels by increasing the excise and excise-equivalent customs duties on these fuels, proportional to the relevant emission rates. This measure is estimated to raise $920 million on an underlying cash basis over the forward estimates period and forms part of the revenue which will be redirected to households and industry to help them adjust;

- reforming the tax treatment of living-away-from-home allowance and benefits, for periods commencing 1 July 2012 for both new and existing arrangements. These changes will better target this concession to a more appropriate range of circumstances and require individuals to substantiate that the allowance is being used for its intended purpose. This measure is estimated to raise $682 million on an underlying cash basis over the forward estimates period; and

- pausing indexation of the superannuation concessional contributions cap for one year in 2013-14, improving the underlying cash balance by $485 million over the forward estimates period.

These have also been helped by reductions in payments:

- a one-off increase of 2.5 per cent to the efficiency dividend for most Commonwealth departments and agencies in the 2012-13 financial year. This measure has no impact in 2011-12 but is expected to reduce cash payments by $1.5 billion over the period 2012-13 to 2014-15;

- a 20 per cent reduction in funding provided under capital budgeting arrangements for relevant Commonwealth agencies and departments. This measure has no impact in 2011-12 but is expected to reduce cash payments by $710 million over the period 2012-13 to 2014-15;

- implementing an effective carbon charge on the use of liquid and gaseous fuels through the fuel tax system by reducing the business fuel tax credit entitlement for the use of these fuels. This measure is expected to cost $2 million in 2011-12 but deliver a net reduction in cash payments of $962 million over four years;

- reducing the maximum co-contribution payable and rate at which the government matches eligible personal superannuation contributions for low to middle income earners from 1 July 2012. This measure is expected to reduce cash payments by $660 million over two years from 2013-14;

- resetting the baby bonus to $5,000 per child from 1 September 2012 and pausing indexation from 1 July 2012. This measure is expected to cost $1 million in 2011-12 but delivers a net reduction in cash payments of $320 million over four years;

- ceasing the student experience and quality learning components of Higher Education Reward Funding, reducing expected cash payments by $3 million in 2011-12 ($241 million over four years). Funding will continue to be provided for the achievement of participation and social inclusion outcomes; and

- making the payment of Family Tax Benefit Part A supplement conditional on a child being fully immunised from 1 July 2012. From 1 July 2013, children will be required to receive vaccines for meningococcal C, pneumococcal and varicella to be assessed as fully immunised. From this date, Priorix-Tetra®, a combination vaccine, will be added to the National Immunisation Program. This measure is expected to cost $13 million in 2011-12, but deliver savings of $197 million over four years.

Once again it would appear that Treasury has under-estimated the effects of the disleveraging public while overestimating the offsetting strength of the capital investment boom. However, unlike my previous assessment, this now seems to have been made worse by some highly optimistic predictions for the future.

I don’t think it is too much of a stretch to suggest that a European recession is baked in, with the potential for much worse, and the expectations around resource revenues are, as H&H suggested yesterday, disconnected from the reality of the current global economy. On top of this I can’t see anything to suggest that rates of credit issuance are about to return to the levels that would provide taxation revenues required to meet surplus targets. It must also be noted that at a time when the private sector is showing signs of an attempt to deleverage an attempt by the public sector to do the same in the absence of a current account surplus is likely to be counter-productive.