Those greasy pie and pizza sellers got me thinking – what other opportunities could arise from Qantas’ woes? More to the point, which ASX-listed company would most likely benefit from the very expensive Qantas-union arm wrestle?

Surely Virgin Blue.

But before you call me Shirley, let’s take a closer look.

The Business

Virgin Blue Holdings (VBA) started out in 2000 with 2 aircraft and one Australian route. Their aim was to create a low‑cost domestic carrier service to undercut the Qantas and Ansett duopoly that was very good at gouging Australian travellers. They were pretty successful in their efforts, seeing off Ansett, forcing Qantas to create the low-cost carrier Jetstar and almost halving the cost of domestic air travel in Australia.

VBA are now a leading airline group, having listed on the ASX in 2003 and currently incorporating the following ventures:

- Virgin Blue – Australian domestic

- Pacific Blue – a NZ based airline servicing the pacific islands, NZ and Australia

- Polynesian Blue – a joint venture with the Samoan government

- V Australia – an international service based out of Australia

Like its rival Qantas, Virgin also operates a frequent flyer points program called Virgin Velocity, which can be used to purchase flights or other assorted consumer items with points earned via flying with VBA or associated credit cards.

Financials

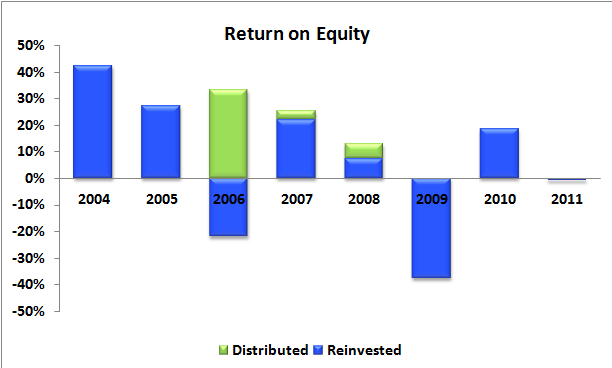

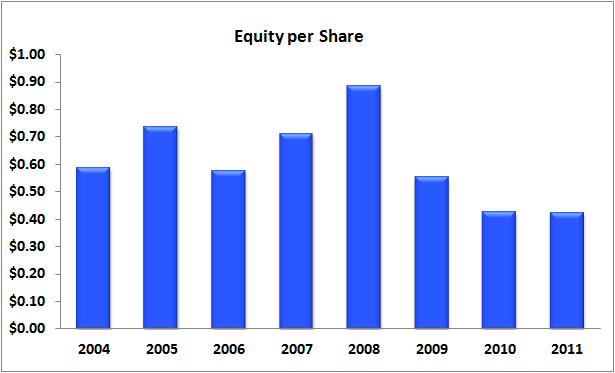

Virgin’s finances are not a pretty sight. Return on equity (ROE) is volatile at best, woeful at worst. The early years saw stellar ROE of +40%, but the last five years have seen a high of 25%, a loss of 37% and an average of 5.5%. Equity per share rose from 60c to 90c per share over the 2004/2008 period however has now dropped to 42c per share.

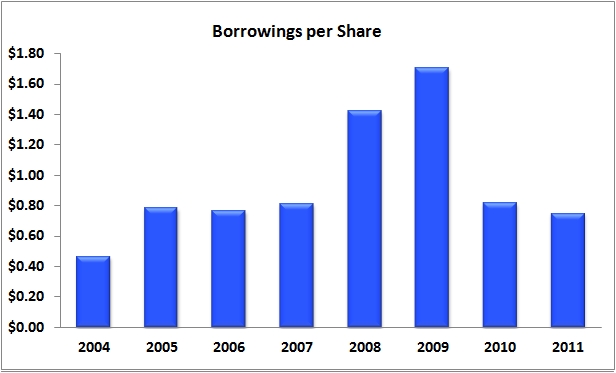

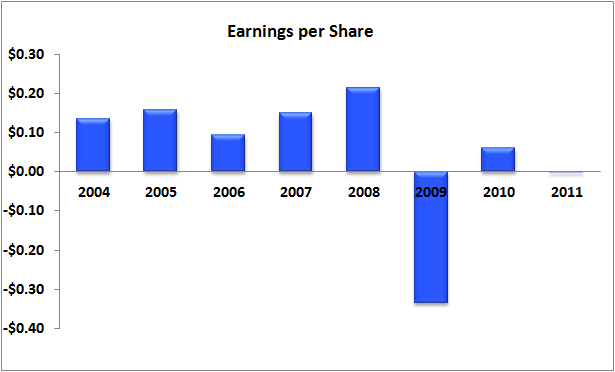

In addition to unsightly ROE, Virgin also has a debt problem. Current net debt levels of about $900 million are extremely high compared to average NPAT of $200m over the last five years. Note the use of the word average –2011 recorded a loss of $67m while, which was a good year compared to 2009 when VBA lost $160m. As such, earnings per share results are also volatile. There are numerous causes for the earnings volatility, from high oil costs during first mining boom to reduced demand and computer glitches post-GFC, as well as ever-increasing labour cost and airport charges.

Even the franking huggers would avoid embracing VBA – the last dividend was paid in 2008. In addition, equity per share also dropped during this period. As such, VBA has successfully destroyed about $225 million in shareholder capital during that time (which was replenished by a capital raising in 2010 of about the same amount). I this regard Virgin is very similar to its rival Qantas, as I covered here in an earlier MB post.

Management

The board and executive management team possess a wide range of skills covering airline, finance, legal and even political arenas (former Deputy Prime Minister Mark Vaile is a non-executive director). Average tenure appears to be about 5 years, with very few long-term associations. Despite the skills available, I don’t think there is anything the management team can do to sustain high ROE in this industry. There are just too many factors outside of their control – oil prices, labour, airport charges, forex movements, flight demand – coupled with the very high operating and capital costs of an airline. At best they can hope for a profit in the good years and convince shareholders to pony up more capital in the bad years, just like Qantas.

Remuneration is split about one third between fixed-base, short term incentive (STI) and long term incentive (LTI) pay. The LTI increases to 40% with more senior executive.

The long term incentive targets are based on total shareholder return – a measure of dividends plus share price change over a three year period. However, the measure is relative to the ASX200 and excludes financial services and resource companies, which are basically the biggest and strongest performers in the ASX200. So the LTI plan can still reward executives handsomely even if the TSR is woeful, so long as the weaker companies of the ASX200 perform even more woefully. At least the LTI is measured over a 3 year period into the future and for the past couple of years has paid nothing at all. At least there is some recourse for the lack of dividends.

VBA claims that having a higher proportion of salaries “at risk” (ie in STI or LTI plans) better aligns executive interests with shareholders. That’d be true if the incentives were absolute (not relative) and based on capital returns (not dividends and share price, which can be more easily manipulated). Unfortunately for VBA shareholders, this is not the case.

Risks

- Revenues are heavily impacted by oil prices

- Revenues are heavily impacted by foreign exchange movements (oil is traded in USD)

- Revenues are heavily impacted by labour costs and airport charges, neither or which will be decreasing in Australia any time soon

- VBA operates in a cut-throat industry full of subsidised national carriers

Opportunities

- The recent Qantas debacle should increase Australian-based business for VBA

Valuation

Assuming an average normalised ROE (inc franking credits, where dividends are paid) of 7.5% over 5 years, a dividend payout eventually increasing to 50% and a current equity per share level of $0.42, we value VBA at $0.19 per share.

Due to the poor ROE, volatile earnings and high debt load, Empire considers VBA to be non‑investment grade. As such, we would not calculate a buy price.

Summary

Despite flying high in the early years, Virgin Blue has demonstrated the wisdom of Richard Branson’s quip on how to become a millionaire:

Easy – just start out as a billionaire and buy an airline

ROE over the last 5 years has been volatile and depressed, averaging only 5.5%. Virgin has been buffeted by oil costs, labour costs, the GFC, computer glitches and a high debt load. In short, it’s just like every other airline out there, but not backed by supportive legislation or deep, subsidised government pockets.

Even if Qantas fell over tomorrow, I wouldn’t be putting my hard-earned into Virgin Blue.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no current interest in the business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.